Stocks are higher this morning on no real news. Bonds and MBS are up.

Inflation came in weaker than expected at the wholesale level, with the producer price index falling 0.1% MOM and increasing 2.6% YOY. The core index (which strips out food, energy, and trade services) rose 0.1% and is up 2.3% YOY.

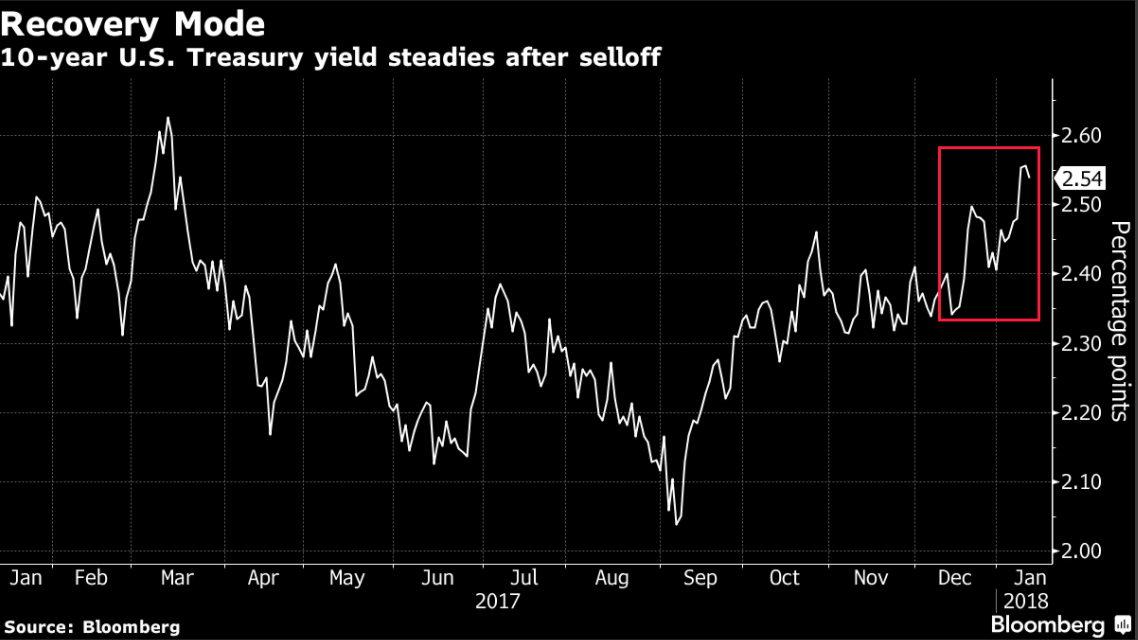

Bonds were trying to break through support yesterday, however a decent 10-year auction pushed rates lower. The 10 year yield dropped 2 basis points on the result and is holding those levels this morning after the weaker than expected PPI. The Chinese government said that yesterday’s Bloomberg story of a potential slowdown or suspension of Treasury purchases could be fake news.

Initial Jobless Claims rose to 261k in a holiday-shortened week. I would bet most of this is being driven by post-holiday retail layoffs.

Wal-Mart is raising its starting wage to $11 an hour and handing out bonuses to employees. They are just the latest in a string of companies that announced raises and bonuses recently. We’ll see if this moves the needle in the official wage inflation numbers out of BLS. It is interesting that most of the wage inflation seems to be occurring at the bottom end of the scale.

Mortgage Credit Availability decreased in December, according to the MBA. Government programs (FHA/VA) especially at lower FICO and higher LTVs were the biggest decliners. Note that GNMA servicing values did get hit in 2017 as prepay speeds were generally higher than the benchmark TBAs were forecasting. That said, we saw a tightening of credit in all products, including jumbo. Despite the monthly drop, credit availability is still up substantially from a year ago.

The Kansas City Fed is out with their housing outlook for 2018, and it predicts continued price increases as pent-up demand remains unsatisfied. Household formation remains below the benchmark forecast done in 2000 based on demographics. Part of this is a continuation of the decades-long trend of Americans marrying and having kids later than previous generations. Student loan debt is also a factor. That said, the shortfall is astounding – about 3.5 million households. That is almost 3 years’ worth of housing starts at current levels! Housing starts would need to double to satisfy that demand. If we get 2 million plus housing starts, we are looking at the strongest growth since the 90s. Lack of workers, available land, and land use regulations remain the bottlenecks.

Last year, the Fed paid $80 billion in profits to Treasury. Long-term rates fell slightly during the year and that number was lower than 2016. For those keeping score at home, that works out to be a 1.8% ROA, which is pretty punchy for a bank. The big question is what happens if rates move up faster than the Fed anticipates?

The Trump Administration is reviewing the Community Reinvestment Act, to make compliance easier and more transparent.

Filed under: Economy, Morning Report | 69 Comments »