Vital Statistics:

| Last | Change | |

| S&P Futures | 2547.5 | -2.5 |

| Eurostoxx Index | 390.1 | -0.9 |

| Oil (WTI) | 49.7 | -1.1 |

| US dollar index | 87.2 | 0.2 |

| 10 Year Govt Bond Yield | 2.38% | |

| Current Coupon Fannie Mae TBA | 102.875 | |

| Current Coupon Ginnie Mae TBA | 103.938 | |

| 30 Year Fixed Rate Mortgage | 3.9 |

Stocks are lower after the jobs report. Bonds and MBS are down as well.

Jobs report data dump:

- Nonfarm payrolls -33,000 (100k-150k expected)

- Unemployment rate 4.2% (4.4% expected)

- Labor force participation rate 63.1% (62.8% expected)

- Average hourly earnings up .5% MOM / 2.9% YOY (expectation .3% / 2.6%)

Hurricanes Harvey and Irma are responsible for the weak payroll number, which is the only depressed number in an otherwise strong report. Much of the drop in payrolls was due to a drop in restaurant / bar jobs. If a restaurant was closed due to power outages or evacuation the employees are generally not paid, and therefore won’t show up on the list of jobs.

The critical numbers from the jobs report (which is causing rates to rise) is due to higher-than-expected wage growth and the increase in the labor force participation rate. These point to a tightening in the labor market and an increased likelihood of a rate hike in December. The Fed Funds futures are now predicting a 92% chance of a December hike, up from 80% yesterday.

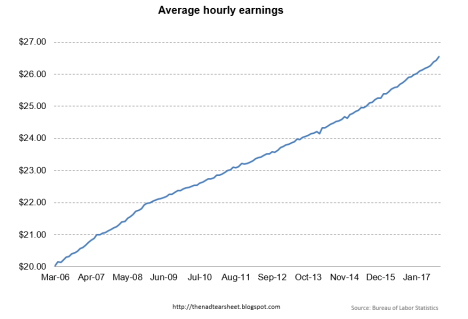

Take a look at the chart of average hourly earnings below. You can see the change in inflection (sharp slowdown in growth) starting in early 2009, however you can also see the change in inflection (that appears to be accelerating) that started in early 2015. We could finally be seeing some wage inflation at long last. Note that there is a possibility that the jump in wages could be driven by the drop in restaurant jobs, which are generally low-paying. That would bump up the average a tad.

The NAHB and NAR are parting ways on the issue of the mortgage interest deduction. The MID is slated to become less important as tax reform takes shape. The standard deduction will be doubled, but many popular deductions will go away. For most people, taking the increased standard deduction will make more sense than itemizing. The NAHB is willing to allow the mortgage interest deduction to go away, as long as the low-income housing tax credit remains. The LIHTC is the big driver that makes building affordable housing make sense. NAR, on the other hand is suggesting that losing the MID would cause a 10% drop in house prices. Since Democrats will be uniformly opposed to any changes to the tax code, it will only take a few Republicans in blue states to put the kibosh on this. The MID has survived many attempts to kill it, and it is simply so popular that it may live to fight another day. Note that there are two things to make the MID less and less important: First, with interest rates so low, the actual interest paid is much less than it was, say, 30 years ago. Second, the MID cap is not indexed to inflation, so as house prices rise, the cap will kick in at progressively lower relative levels.

The Fed weighed in on tax reform, saying that it could cause a short term bump in the economy, but will raise the deficit and inflation. Of course how much it increases the deficit will depend on the economic forecast used. Republicans want to argue that cutting taxes will increase growth, which will increase the taxes received by Treasury (called dynamic scoring). Democrats want to exclude that growth, arguing that it is invariably too rosy. All sorts of think tanks will weigh in on it and you will have to know their political predilections before reading their take. Many think tanks sell themselves as “non-partisan” when they really are not.

Filed under: Economy, Morning Report | 17 Comments »