Vital Statistics:

| Last | Change | |

| S&P Futures | 2475.5 | 7.5 |

| Eurostoxx Index | 380.1 | 2.2 |

| Oil (WTI) | 49.9 | -0.3 |

| US dollar index | 85.9 | 0.1 |

| 10 Year Govt Bond Yield | 2.32% | |

| Current Coupon Fannie Mae TBA | 102.93 | |

| Current Coupon Ginnie Mae TBA | 103.81 | |

| 30 Year Fixed Rate Mortgage | 3.95 |

Stocks are higher this morning on overseas strength. Bonds and MBS are down a touch.

Personal income was flat in June, as a drop in interest / dividend income offset an increase in compensation. Inflation remains nowhere to be found as the PCE price index (the Fed’s preferred measure of inflation) was flat MOM and up 1.4% YOY. Ex-food and energy, the numbers ticked up 0.1%.

Home prices rose 1.1% in June and are up 6.7% YOY, according to the CoreLogic Home Price Index. Want to know how tight inventory is? Unsold inventory as a percentage of households stands at 1.9%, which is the lowest in 30 years.

Manufacturing strengthened slightly in June, according to the ISM and PMI manufacturing indices. Construction spending fell 1.3% in June as public construction spending fell. Residential construction was down 0.3% MOM, but is up 9% YOY.

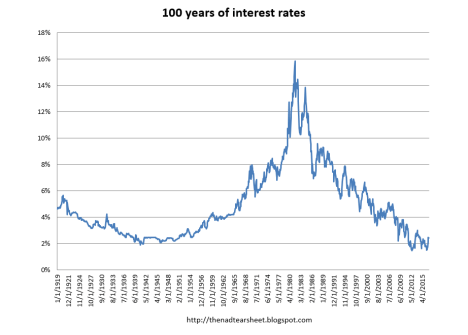

Remember “irrational exhuberance?” That was Alan Greenspan’s warning to investors that there was a stock market bubble. Unfortunately for him, he issued the warning on 12/5/96, about 39 months before the stock market actually peaked. Well, he is back, warning of a bond market bubble. He is warning of an abrupt pop in the bond market, and a return to 1970s stagflation. Color me somewhat skeptical of the abrupt pop in the bond market argument. Below is a chart of interest rates going back to World War 1. As you can see, interest rate cycles are long. Aside from the disastrous Fed hike after the crash of 1929, rates stayed below 4% from 1924 to 1959.

FWIW, the 1970s stagflation was largely due to the oil shocks combined with the guns and butter policies of the Johnson administration coming home to roost. The 1970s came after decades of economic strength, while today we are coming out of a decade of economic weakness. Housing starts averaged 1.75 million units per year for the entire 1970s. Since 2010, we have averaged about half that. During the 1970s, capacity utilization was running close to 83%. Since 2010, it has been 76%. Wage growth is stuck stubbornly at 2.5% growth, and there is still slack in the labor market. I just don’t see the conditions in place for a return to 1970s stagflation.

Financial regulators are working on a rewrite of the Volcker rule, which prohibits FDIC insured banks from proprietary trading. No one is sure what is actually being proposed – it may turn out that the re-write will merely provide some bright lines to separate prop trading from market-making. Between a drop in commissions and cloudy guidance over prop trading, market making has dried up, and liquidity is suffering in many markets as a result. Any changes will have to pass muster with a panoply of regulatory agencies, so this is going to take some time.

Filed under: Economy, Morning Report | 20 Comments »