Vital Statistics:

| Last | Change | |

| S&P Futures | 2258.6 | 8.0 |

| Eurostoxx Index | 356.3 | 2.6 |

| Oil (WTI) | 53.1 | 0.3 |

| US dollar index | 91.3 | 0.0 |

| 10 Year Govt Bond Yield | 2.44% | |

| Current Coupon Fannie Mae TBA | 103 | |

| Current Coupon Ginnie Mae TBA | 104 | |

| 30 Year Fixed Rate Mortgage | 4.13 |

Markets are higher this morning as Italian bank Unicredito launches a restructuring plan. Bonds and MBS are up.

The FOMC meeting begins today, with the announcement scheduled for 2:00 pm tomorrow.

Despite the expectation that the Fed will hike rates tomorrow, inflation remains pretty much nowhere to be found. Import prices fell 0.3% last month and are down 0.1% on an annualized basis. Export prices were down 0.1% MOM and down 0.3% YOY.

Holiday shopping is starting out subdued, according to Redbook. Same Store Sales were up 1% for the week ending Dec 10.

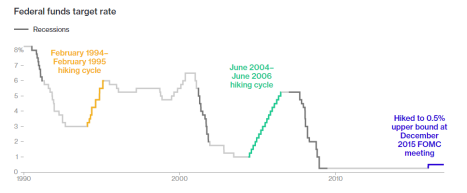

Here is a comparison of the past 3 tightening cycles: 1994-1995, 2004-2006 and the current one. The biggest differences: This tightening is happening much later in the cycle (this second hike is almost 7.5 years since the expansion began), unemployment is much lower (4.9% versus 5.5% and 6.5%) and growth is much lower. Of course the biggest difference is that the prior cycles were implemented in the context of a traditional business cycle, where a buildup in inventory caused a recession. This time around, it is the context of an asset bubble, where a buildup in bad debt caused the recession. These are fundamentally different animals, and explains why the Fed is taking baby steps this time around.

One thing to watch after the FOMC announcement: Donald Trump’s twitter feed. Any sort of jawboning of the Fed by Trump will almost certainly affect bonds. In the past, Trump has been hawkish, however now that he is a politician, he might adopt a more dovish tilt, as most politicians do (at least the ones in office).

Fed watcher Tim Duy believes the markets are probably too sanguine about rate hikes in 2017. The markets are looking for two 25 basis point hikes, and he believes the risk is to the upside (i.e. a more aggressive Fed).

Small business optimism picked up in November, according to the NFIB. Expectations for an improvement in the economy and top line growth drove the improvement. We also saw a big uptick in hiring plans, although capital expenditures are still depressed. Business is looking for a cut in corporate taxes and a relaxation of regulations. Remember however, these are expectations, not a description of how business is at the moment.

Zillow has its 6 big predictions for 2017 in the real estate markets. Here are the big themes:

- Cities will focus on denser development of smaller homes close to public transit and urban centers.

- The drop in the homeownership rate will reverse as more Millennials become homeowners.

- Rental affordability will improve as incomes rise and growth in rents slows.

- New home price inflation will continue, and could be exacerbated by any sort of slowdown in immigration.

- The suburban population will increase as city-dwellers seek more affordable housing outside of the cities.

- Home values will grow 3.6 percent in 2017 versus 4.8% in 2016.

There were 30,000 completed foreclosures in October, according to CoreLogic. Foreclosure inventory is down 32% from a year ago. 1 million mortgages were down 90 days + which is a decrease of 25% YOY and is the lowest level since August 2007. Normalcy for foreclosures is around 22,000 a month, so we still have some wood to chop.

Donald Trump has nominated Exxon-Mobil CEO Rex Tillerson to be Secretary of State. Getting this nominee past the Senate will not be a slam-dunk, given his ties with Vladimir Putin and Russia in general. This is even more sensitive given that the CIA thinks Russia might have had something to do with the Wikileaks emails surrounding the DNC.

Separately, Donald Trump cancelled a press conference scheduled for today regarding how he will handle his business interests once he takes office.

Filed under: Economy, Federal Reserve, Morning Report | 49 Comments »