Global stock markets are down again on no real news. Whatever comfort markets took in Janet Yellen’s remarks yesterday are over. Bonds and MBS are up, with the 10 year bond yield pushing a 1.5% handle.

Speaking of Janet Yellen’s plan to continue to increase the Fed Funds rate, the markets are not buying. The Fed Funds Futures contracts are forecasting no rate hikes until 2018.

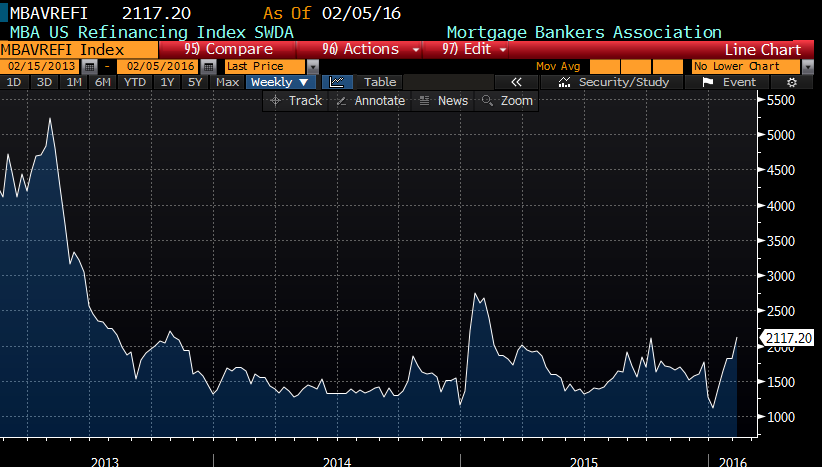

Loan officers, you have been given an unexpected gift with the 10 year. Rates are now at the pre “taper tantrum” level when the Fed started bracing the markets for the end of QE. So I guess the Fed didn’t need to purchase $4 trillion worth of assets to get rates down?

Initial Jobless Claims fell to 269k from 285k last week. It bears repeating that these numbers are exceptionally good and are associated with boom times. The tape doesn’t care, but still…

The Bloomberg Consumer Comfort Index rose slightly to 44.5 from 44.2 last week. Lower gasoline prices are helping improve the mood.

Most commodities have been getting crushed lately, however one has been on a tear: Gold. Gold is a strange animal, in that it is one of the few financial assets that isn’t some else’s liability. The price of gold can be considered to be the (inverse) confidence indicator in the world’s central banks. Gold up, confidence down.

Continuing on the central bank thread, one of the bright spots in the US markets has been auto sales. This has been driven by a couple things: The biggest was that people deferred replacing cars until they absolutely had to due to the lousy economy. However another reason is cheap credit, and some hedge funds think they have found the new “big short” in subprime auto. When you can get an 8 year loan for a new car at a rate below the 30 year fixed rate mortgage, something is awry.

So, yet another pillar holding up the economy was based on cheap credit. Janet Yellen must feel like Michael Corleone: “Just when I thought I was out, they pull me back in.”

The House Financial Services Committee is having a hearing today on FHA MIP. Expect Democrats to push for another cut and Republicans to be against it. The Democrats are in a strange position with the base continuing to push for even tougher regulations for the industry and the affordable housing types getting sick and tired of the tight credit that results.

Filed under: Economy, Morning Report | 76 Comments »