Stocks are lower this morning, reversing the post FOMC rally. Bonds and MBS are up.

As expected, the Fed rose the Fed Funds target rate by 25 basis points. The statement generally focused on how the economy has improved. The biggest surprise in the statement and the projection materials was the forecast for rates going forward. The Fed lowered their expected Fed Funds range going forward. You can see the September versus December dot graphs below:

In response to the rate hike, banks hiked their prime rate to 3.5% from 3.25%. A lot of consumer debt, especially credit cards, are tied to the prime rate, which means consumers will feel the pinch.

The Philthy Fed Manufacturing Index fell to-5.9 from 1.9. while initial jobless claims fell from 282,000 to 271,000.

The Bloomberg Consumer Comfort Index rose to 40.9 from 40.1.

The Index of Leading Economic indicators fell from 0.6% to 0.4%.

Stocks are up this morning ahead of the FOMC meeting. The decision should be released around 2:00 EST. Given that this was the most telegraphed rate hike in history, I don’t necessarily expect a lot of volatility around the decision, however the language in the statement could always spook the markets. The consensus seems to be a hike of 25 basis points and very dovish language.

Housing starts increased to 1,173 million last month and building permits increased to 1,29 million. The increase in housing starts was in both single-fam and multi-fam, while the increase in permits was mainly in multi-fam. We still continue to under-build which is just creating more pent-up demand. We are in the seasonally slow period for housing, so I wouldn’t read too much into these numbers.

Mortgage Applications fell 1.1% last week as purchases fell 2,8% and refis rose 1.4%.

The strong dollar is still wreaking havoc on the manufacturing sector. Industrial Production fell 0.6% last month and capacity utilization fell to 77% from 77.5%. Manufacturing Production was flat.

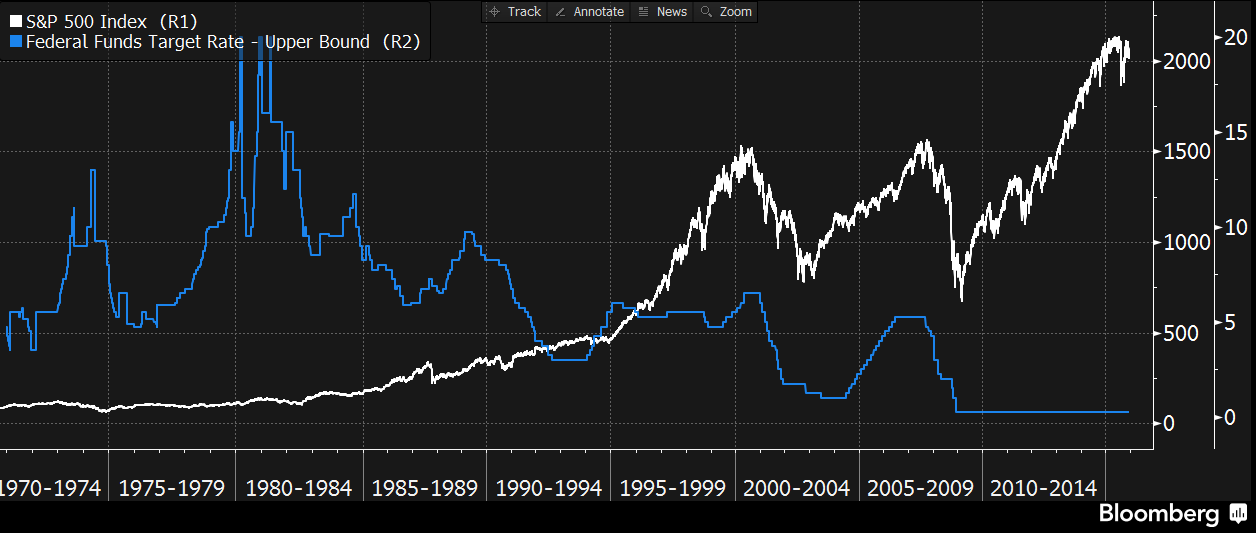

As the Fed begins to remove support from the market, stock market strategists are wondering what will happen to the stock market. Are current market levels a function of the Fed’s stimulus programs or are they supported by earnings and economic fundamentals? I can’t see a gradual tightening cycle collapsing the market, but it will mean that further increases in the market will have to be driven by earnings and economics and you can’t expect to see further multiple expansion. Dividends will become much more important. Here is a chart of the S&P 500 versus the Fed Funds rate over the past 45 years:

Interest rate cycles are long. The bull market in Treasuries started in 1982 or so is probably over, unless the economy rolls over again. The previous bear market in Treasuries ran from the mid-50s through the early 80s.

Note that the other central banks (especially Japan and Sweden) have tried to get off the zero bound, only to see rates fall back to 0% again. If that happens, then what? The Fed would have to raise its inflation target.

The story of Marty Whitman’s Third Avenue downfall. A value investor who simply didn’t fit with the current momentum-investor world. The current liquidity crunch in junk bonds is being attributed to Third Avenue’s Focused Credit Fund, which just put up gates preventing investor withdrawals. Daily liquidity, they promised.

Markets are higher this morning as oil and credit markets have an up day. Bonds and MBS are getting whacked.

There is no news in particular driving the rally in oil and other financial assets. Markets don’t go up in a straight line and they don’t go down in one either. Another possibility is that market participants are positioning themselves ahead of the Fed rate hike.

The problems in the credit markets are centered in distressed credits. The carnage is concentrated in the energy sector. For those keeping score at home, if you want to track how things are going, check out the Ishares high yield ETF HYG. The chart is below. You can see how it has been rolling over. I included the financial crisis years for perspective.

In economic data this morning, the consumer price index was flat on a month-over-month basis. Ex-food and energy, it increased 0.2%. On a year-over-year basis, it increased 2% ex- food and energy, which is right in line with the Fed’s target. The Bloomberg Real Average Hourly Earnings index increased to 1.6% annualized, up from an upward-revised 2.4% last week. Maybe, just maybe, wage inflation is upon us.

The Empire Manufacturing Index improved to -4.6, indicating that things are still tough in the manufacturing sector. Blame the dollar.

Homebuilder sentiment fell in December to 61 from 62. The index hit a 10 year high in October, so the sentiment is still pretty positive. The builders all reported pretty strong increases in orders and backlog, so it looks like 2016 could be a better year for the builders. The Spring Selling Season is about 2 months away. Note we will get numbers out of Lennar on Friday.

A survey of economists says that mortgage rates are going up. Probably a no-brainer, given the Fed is hiking rates. Does that mean a bad year for the housing sector? Not necessarily. Certainly an increase in rates is going to make lives tough for the refi shops. However if rates are rising because of a strengthening economy, that is probably great news for the purchase business as Millennials leave expensive rentals and buy property.

Mortgage fraud is making a comeback, according to CoreLogic. As credit loosens and purchase activity increases, you are going to see more risk of it.

Markets are lower this morning as oil continues to fall and problems at a high yield mutual fund begin to spill over.

No economic data today. The markets will be focused on the Fed and the evolving situation in distressed debt markets.

Marty Whitman’s Third Avenue Focused Credit Fund has suffered losses as the rout in high yield has reduced liquidity. Dodd-Frank has severely curtailed market-making operations at investment banks, and right now there are very few buyers of distressed credit as hedge funds face redemptions and investment banks cannot step in because of capital requirement. In fact, the regulators are considering additional steps to ensure a bank failure doesn’t bring down the entire financial system, which means that investment banks will probably de-risk further, making them even less likely to act as market-makers. This will be an interesting first test of a financial crisis in the new Dodd-Frank world.

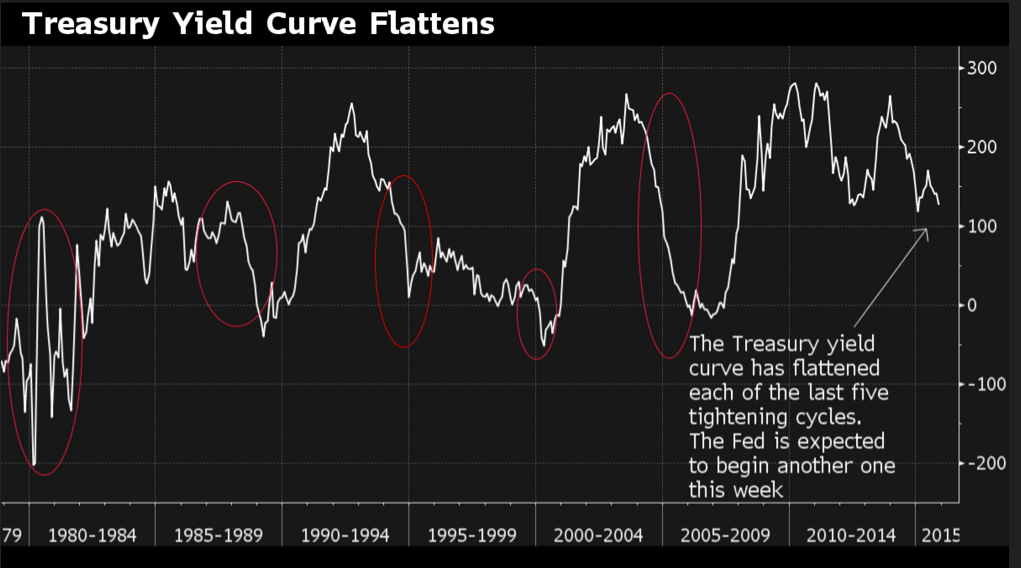

As a general rule, in credit crunches, the long bond rallies. You saw that on Friday, where the 10 year yield fell 10 basis points in spite of strong retail sales data. This week will be interesting between the evolving Third Avenue situation and the FOMC decision on Wednesday. LOs, expect bond market volatility this week. As a general rule, tightenings have not had a dramatic effect on mortgage rates. In fact, the yield curve has flattened during all the tightening cycles since 1979. Granted, these tightenings have taken place in context of a secular bull market in bonds, so take this analysis with a grain of salt. That said, unless the economy really starts taking off (and you start seeing wage inflation), chances are that the 10 year yield increases less than the amount of the rate hike. Note that CoreLogic is forecasting a 4.5% 30 year fixed rate mortgage by the end of 2016.

Mortgage loan performance has been improving, according to the OCC. Performing loans increased to 93.9% from 93% a year earlier. New foreclosures are down 22% YOY.

Ex GMAC Ally Financial is getting back in the mortgage business. Ally CEO said this about the move: “Don’t think of this as Ally going down the road of the old GMAC,” Brown said, referring to the home lending unit that brought Ally to the brink of collapse. The ironic thing is that the “new subprime” is auto loans, and that is Ally’s bread and butter these days. They are offering 8 year loans for new cars at rates at rates substantially below the 30-year fixed rate mortgage (think 3.5% range). Given that new cars depreciate like sushi, this is a very, very mispriced loan. If you are wondering why the Fed wants to get off the zero bound even in the face of zero inflation, there you go. Those sort of rates are a function of ZIRP and the impossibility of earning a decent rate of return. It would be ironic if the ne-er do well of mortgages had simply morphed into the ne-er to well of auto lending and we see a collapse in asset backed security liquidity.

Today, on the day Paul Krugman tells us that a bunch of politicians getting together and posing for photographs and brunching excessively has saved the planet, I feel motivated to ask this question:

What do people mean when they tell us, repeatedly, that climate is not weather? Or if you wonder how we’re predicting the climate and its effects 100 years from now, when we can’t reliably predict the weather 12 hours from now, and sometimes cannot accurately predict the weather as it’s happening, why does someone shake their head sadly about what a moron you are and explains: weather and climate are not the same thing, you sad, mentally-limited man-child.

I mean, why is the answer to the observation that we are not good at predicting the future for complex systems even in the near term essentially: “Well, the stock market is not the same thing as a large river with many tributaries”. I am aware that a watermelon is not a football, but if I want to say something about the shape of the football, the watermelon might still have some relevance. Just saying: “a watermelon is not a football” does not suddenly make a watermelon a trapezoid.

The official explanation is that climate is simple while weather is complex. Which, summarized thusly, seems an absurd statement. What they actually say, in their own words:

Weather is chaotic, making prediction difficult. However, climate takes a long term view, averaging weather out over time. This removes the chaotic element, enabling climate models to successfully predict future climate change.

… isn’t much better. There is very little evidence that climate models are able to successfully predict future climate change. And I find it interesting that a site that calls itself “skeptical science” blithely asserts that the climate models are predicting the future without the most basic evidence—the actual prediction of the future.

Also, you cannot reduce the complexity of a million or a billion inputs by averaging. Again, where are the skeptics (not to mention the mathematicians) at Skeptical Science? The assertion that climate can be accurately predicted (because averaging!) while the weather 12 hours from now, much less 3 days from now, cannot reminds me of that cartoon. You know the one.

I would also observe that every time there is a severe or unusual weather event, climate suddenly becomes the cause for the weather. Which, to me, begs the question why we cannot use our infinitely accurate climate models to start predicting the weather. Wait, I know! Because we’ve tried it, and it turns out those predictions were wrong, too.

I have come to the not unreasonable conclusion that climate ≠ weather in the context of anthropogenic climate change because we have ample, daily evidence that the behaviors of a complex system cannot be predicted with any degree of accuracy. The predictions of climate change are always far in the future, and evidence of inaccuracy of such predictions so far in the past they can be dismissed, or the data massaged. Harder the argue that, yes, it was sunny yesterday, even though the leaves are still wet from all the rain.

…

Tangentially related, even mainstream, largely liberal news organs like Time and Newsweek had to observe that the Paris talks were far less about climate or “saving the planet” than they were about making money, creating markets, and allocating capital.

Finally, How Climate Change Deniers Sound to Normal People:

Because anybody who doesn’t agree with me ideologically is abnormal. And sounds like an idiot to all the normal people. Conform, you abberants! Conform!

Stocks are lower this morning on emerging market weakness and oil. Bonds and MBS are up.

Retail Sales rose 0.2% in November, lower than expectations. Ex food, energy and building materials, they rose 0.6%, better than expectations.

Inflation at the wholesale level remains under control as the producer price index rose 0.3% in November. Ex food and energy and trade services it was up 0.1%.

Morgan Stanley is warning investors that the world’s central banks could succeed in creating inflation. Markets are definitely priced right now as if inflation is never ever coming back. We could see another bond sell-off like the “taper tantrum” of 2013. IMO, until we start seeing wage inflation we don’t have anything to worry about on that front.

Even those who didn’t see the questions beforehand considered the evaluations a breeze. “I’ll be honest with you—I studied harder for fast-food jobs and waiter jobs when I was in college than I did for their program,” says Kenneth Colvin, who was a US Army air-traffic controller before joining Scarbrough and Watkins’s training class. “Their testing program is a joke.”

Things got even stranger when the new hires started on-the-job training and found a workplace that, according to five recent ROCC trainees, was inhospitable to newcomers. The ROCC’s employees were mostly WMATA lifers who almost never left the Landover facility. (Even when the Silver Line opened, controllers watched a DVD about the extension instead of touring it.) Many veterans hardly spoke to the new hires, who felt as if they were being iced out. “They wanted us to fail,” Colvin says.

It’s hard to even recommend it for tourists anymore. I use it sparingly, but honestly, Uber is just so much more convenient. So i’m saying that i’d get in an loosely-regulated jitney driven by a stranger (UberX) before getting on a heaving regulated transit system is all you need to know. Of course, on Tuesday, my UberX driver had a Mercedes C-class Sedan.

Also: What an incredible smell you’ve discovered.

This wasn’t the only troubling thing the feds found in Metro’s plumbing. The FTA discovered that train drivers regularly relieved themselves on the tracks because supervisors, due to inadequate training, weren’t comfortable taking the wheel to give them bathroom breaks.