Markets are lower this morning on some disappointing economic data out of China. Bonds and MBS are up small.

Not a lot of big data this week, but we do have some stuff related to real estate. Tomorrow, we will get housing starts and building permits. On Thursday, we will get existing home sales and the FHFA House Price Index. We will also hear from homebuilder Pulte on Thursday.

The NAHB Housing Market Index rose to 64 in October from a downward-revised 61 in September. This is the highest reading since October 2005. Tight supply means that builders can increase average selling prices pretty easily. Unfortunately, since wage inflation remains muted, the median house price to median income ratio has become stretched again.

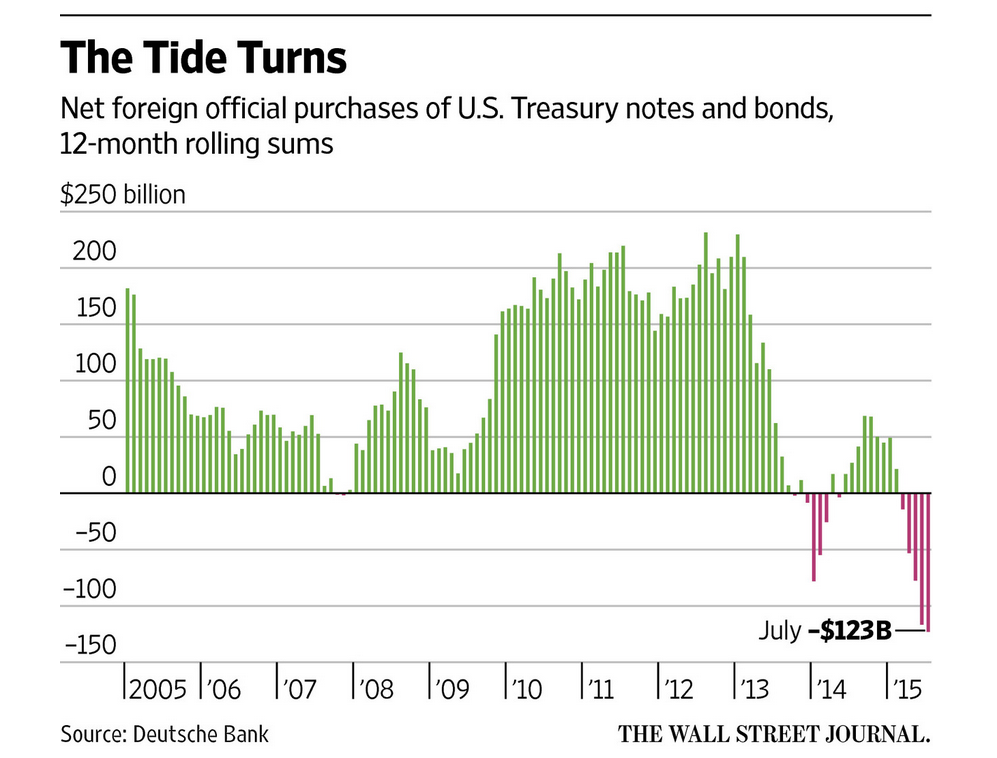

Everyone knows China has been dumping Treasuries, yet rates aren’t increasing. The reason why is that US firms are buying them. This means that (a) US investors are more making bearish bets on the US economy (b) the Fed will probably be watching this closely as a “tell” whether they need to raise rates, and (c) even if rates go up, you might not see any effect out on the curve, which means that mortgage rates might simply brush off any tightening for a while.

Deutsche Bank is beginning to discuss scenarios where the next move could be something like a re-introduction of Operation Twist, which is where the Fed sells short term T-bills to fund purchases of long term Treasuries.

Speaking of the Fed, Republican presidential candidate Donald Trump accused the Fed of keeping rates low for political reasons – to help Barack Obama and Hillary Clinton. Cleveland Fed President Loretta Mester fired back saying that politics is never a factor in their decisions. The political independence of the Fed is extremely important – no politician would ever argue that the Fed should hike rates. One thing to keep in mind however is that as we approach the election in 2016, the Fed will probably hold off on making any rate hikes late in the year to prevent the appearance of being political.

Filed under: Morning Report | 2 Comments »