Markets are lower this morning on European profit-taking. Bonds and MBS are up small.

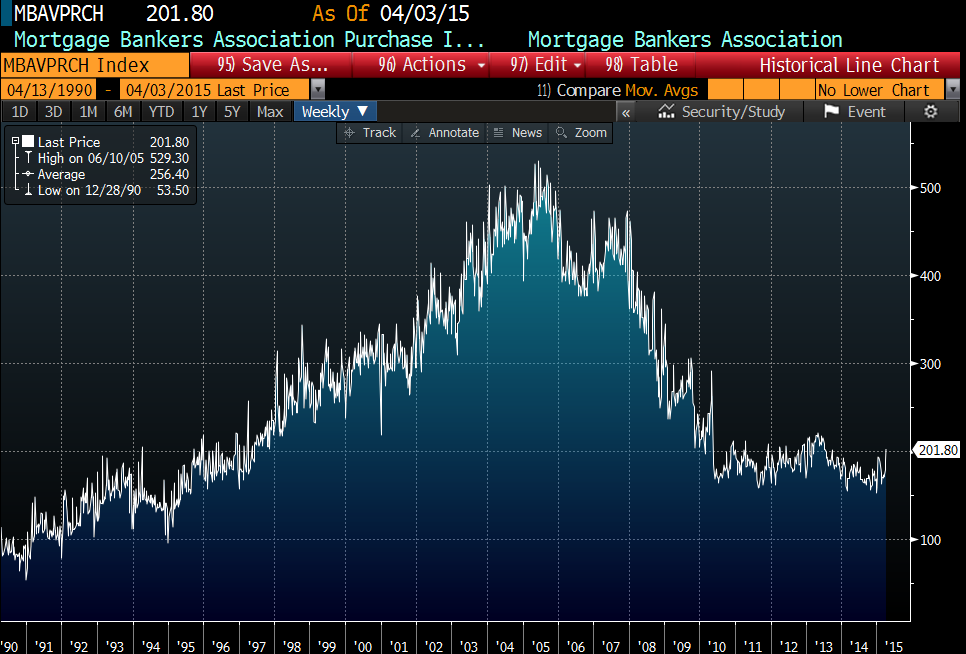

Very disappointing housing starts numbers this morning – 926k versus expectations of 1.04M. Building permits fell to 1.04M as well. The weakness was both in single fam and mult-fam. It is hard to reconcile these numbers with the NAHB Homebuilder sentiment survey from yesterday, or the trading in the XHB ETF but here we are. You might be able to blame starts on the weather (and even that is a stretch) but you can’t blame permits on that. Punch line: supply will remain tight, and prices will probably be a touch higher than people are forecasting.

The Philly Fed Index improved to 7.5 versus 5 last month.

The Bloomberg Consumer Comfort Index fell to 46.6 last week The perception of the buying climate is improving the most, while people’s perception of the economy and their personal financial situation is improving more slowly.

Initial Jobless Claims increased to 294k last week. At least the labor market seems to be holding up, although wage growth is still lackluster.

The left continues to agitate for “living wage” legislation and is hoping they have the beginnings of a movement. Set aside the fact that these protests are largely rent-a-mobs of union people, professional protesters, bums, and college students, there is something bigger happening here. This is at its core a war between “shareholder capitalism” and “stakeholder capitalism” as the left moves to seize ideological ground it lost 30 years ago. Expect to hear a lot of “If Company XYZ just suspended its stock buyback program, they could pay everyone a living wage” claims.

We will undoubtedly see a lot of demagoguery about wages from politicians, but there really isn’t much anyone can do about it. The Democrats will agitate for minimum wage hikes and living wage legislation while Republicans will blame regulation and an anti-business environment. The only thing that will change it is economic growth, and as long as we have slack in the labor market, wages aren’t going up. Growth will happen, but we are still in the aftermath of a burst asset bubble, and recoveries from burst bubbles can be maddeningly slow. Of course this gives the Fed an excuse to stand pat, although they are creating bigger and bigger imbalances as ZIRP continues.

The German Bund yield is now a single-digit midget. If you lend money to the German government for 10 years, you will get 9 bps. Guess we are headed to negative rates there as well. How are insurance companies like Allianz and Munich Re at 52 week highs? There is no way they can cover their actuarial liabilities in sovereign debt these days. I know the stock has a fat dividend yield of 4.1%, but I wouldn’t bet on that dividend getting maintained. As I have said before, the actuarial tables don’t care that money is free. Insurers are stuck between having to take a lot of risk for a little return or to simply use unrealistic future growth assumptions to remain solvent.

Mel Watt is going to lower fees on Fan and Fred loans in order to increase lending to lower credit scores. The “free market’ versus “housing policy as a means of social engineering” battle has been fought and is over. The social engineers won.

Filed under: Morning Report | 4 Comments »