Markets are flattish this morning on no major news. Bonds and MBS are down small.

Merger Monday is back with a couple of big deals in the tech space. NXP is buying Freescale Semi for 11.8 billion, and HP is buying Aruba Networks for $2.7 billion.

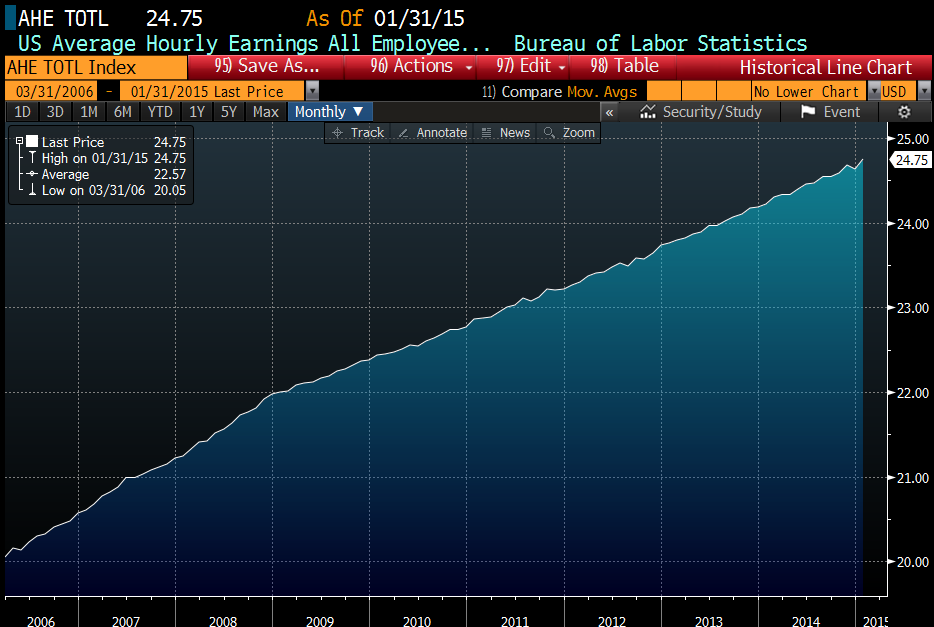

Lots of important economic data this week, but the jobs report on Friday will be the highlight of the week. Bond Markets will be focused on average hourly earnings. Below is a chart of average hourly earnings. Note the change in the slope of the line starting in 2009. That is a change from roughly 3.2% annual growth to 2% annual growth, which is more or less in line with inflation. Later on this week, we will get non-farm productivity, which is expected to fall, and unit labor costs which are expected to increase 3.3%.

Personal Income rose .3% in January, which was below expectations, but flat with December. Wages and salaries were up .6%, which was a big increase from the .1% reading in December. This tends to be a volatile component however, so don’t read too much into one data point. Disposable income rose .9%. The savings rate increased to 5.5% from 5% last month as well. Personal spending fell .5%, however that was partially driven by lower energy prices. Stripping out food and energy, spending increased .1%, which is pretty much in line with what we have been seeing. The punch line: The Great American Deleveraging continues. As incomes increase, that money is used to pay down debt or is getting put in the bank. Investors hoping for another late 90s or mid aughts debt-driven consumption boom are probably going to be disappointed.

Construction Spending fell 1.1% in January, a disappointment. December was revised upward from .4% to .8%. Month to month numbers tend to be volatile. Where is the money going? Lodging, office and commercial space as well as manufacturing. Also public infrastructure spending with increases in transportation, and sewage. Where is it not going? Residential (still). Given the price increases and the current tight inventory, you should expect to see more homebuilding. If the personal income numbers continue to improve that will hopefully change.

Note that optimism about 2015 construction is the highest in 20 years, according to Wells Fargo. Nonresidential construction is the driver, not resi however. Still, that means we are finally seeing some capital expenditures which is encouraging.

The ISM Manufacturing PMI dropped in February to 52.9 from 53.5. The West Coast port slowdown is impacting exporters. The current level of 52.9 corresponds to a GDP growth rate of 3.1%.

Stanley Fischer is telling the markets not to get used to being spoon-fed by the FOMC. Once rates start increasing, the guidance will become more and more murky.

Warren Buffet’s annual letter to shareholders is out. There is nothing earth-shattering in the letter, except for the usual schedule of events for Buffetapalooza, where you can try to throw a newspaper more accurately than Warren. No mention if he is going to bust out the ukulele and jam with the Fruit of the Loom guys however.

Filed under: Morning Report | 32 Comments »