Markets are lower this morning after a lousy retail sales number. Bonds and MBS are up big on the retail sales number and strength in Eurobonds following a court ruling on QE.

Eurobonds are flying as one more hurdle for QE was cleared. The German Bund now yields 42.8 basis points.

Lousy. No other way to put it. Retail Sales fell .9% in December. Ex autos and gas, they were down .3%. The Street was expecting +.5%. To put that number in perspective, the setup for holiday sales was good: falling gas prices gave consumers an unexpected gift, the weather cooperated, and we had an extra shopping day in the season. And in spite of all of that, we put up a lousy number. I am wondering if analysts will start pushing back their estimates of the first rate hike.

Import prices fell 2.5% month-over-month as commodity prices continue to fall.

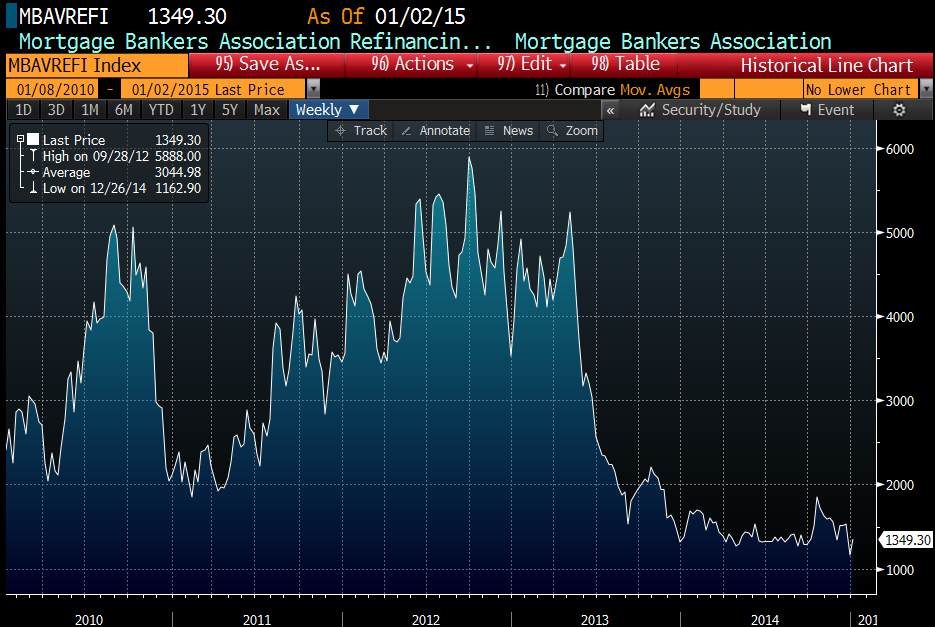

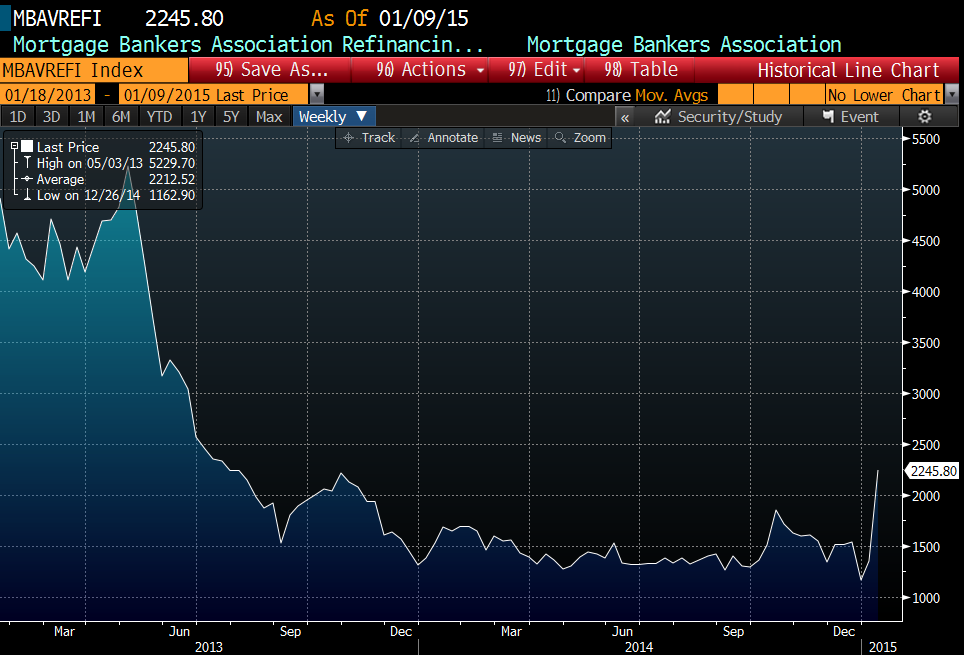

Mortgage Applications rose 49% last week, the biggest gain since 2008. Rates are the lowest since May 2006, and refis soared. Of course we are coming off of a holiday shortened week, but the moral of the story is that we might be setting up for another refi wave, this time driven by home price appreciation as well as rates. That said, we have a way’s to go to get back to the salad days of early 2013, but this is an encouraging number nonetheless.

KB Home gave the markets a head-fake yesterday, with the stock rallying on the earnings release, only to get slammed on the conference call. After rising a few percent pre-open, KB warned that margins would be under pressure and Q1 would be break-even versus Street expectations of 17 cents. Traffic in Texas remains unaffected by the drop in oil prices, at least so far. The entire sector got taken to the woodshed however. It appears that the builders have chewed through a lot of their inventory of cheap land they bought in the aftermath of the crisis, and are now building on lots bought more recently at higher prices. In spite of all of that, ASPs rose 17% to 351k.

Filed under: Morning Report | 1 Comment »