Stocks are higher this morning on no real news. Bonds and MBS are giving back some of Friday’s big gain.

Construction Spending rose 1.1% in October, and September’s number was revised upward from – .4% to – .1%. Private residential construction rose 1.3%. Federal construction spending rose 19.3% and overall public construction increased 2.3%. Construction spending is still 20% off its peak level in 2006. 3Q GDP was boosted by a 9.9% increase in government spending, and we see that the Federal Government increased construction spending by 19%. Perhaps someone was trying to influence the midterms by throwing a little money around…

Chart: Construction Spending 2000 – Present

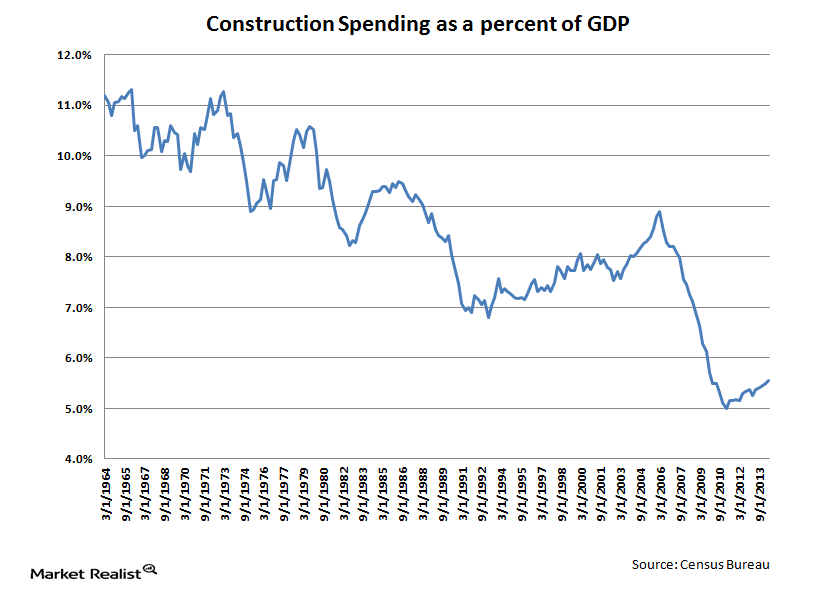

Construction Spending as a percent of GDP:

As you can see from the two charts above, we construction spending has been heavily depressed since the bubble burst 8 years ago. This represents pent-up demand which will drive the economy going forward. If oil prices remain low, 2015 could be a good year and the economy might be able to weather higher interest rates, although I don’t think the Fed raises rates by more than a symbolic amount until wage inflation starts. Given the bid that is underneath worldwide bonds, the Fed could raise short term interest rates and longer-term rates might not even move all that much.

Home Prices increased 6.1% year-over-year in October, according to CoreLogic. They remain 12.4% below their April 2006 peak.

Zillow is predicting Millennials will be the biggest home buying group in 2015 and rent inflation will outstrip home price appreciation. We are already seeing the home price indices reflect higher growth at the lower price points than the higher price points.

While Black Friday sales were tepid for the most part, Cyber Monday sales were brisk, up 8.5%. Consumer confidence indices are pushing through post-bubble highs, and lower gas prices should help improve consumer spending.

Filed under: Morning Report | 6 Comments »