Stocks are up this morning, following Euro markets as they speculate on added stimulus measures out of the ECB. Bonds and MBS are down.

Mel Watt addressed reps and warranties concerns at the MBA conference. He acknowledged uncertainty over putback risk is encouraging lenders to put overlays on Fan and Fred loans, which is excluding many borrowers who should be eligible for a conforming loan. In order to encourage lenders to lend through the entire spectrum of Fannie’s tolerances, rules regarding putback risk will be tightened up. Life of loan exclusions (in other words putback risk for the life of the loan) will be clarified. Watt didn’t go as far as to announce a new 97 LTV Fannie loan, but he did say FHFA was working withe GSEs to develop them.

AbbVie and Shire have abandoned their corporate inversion deal based on possible tax law changes.

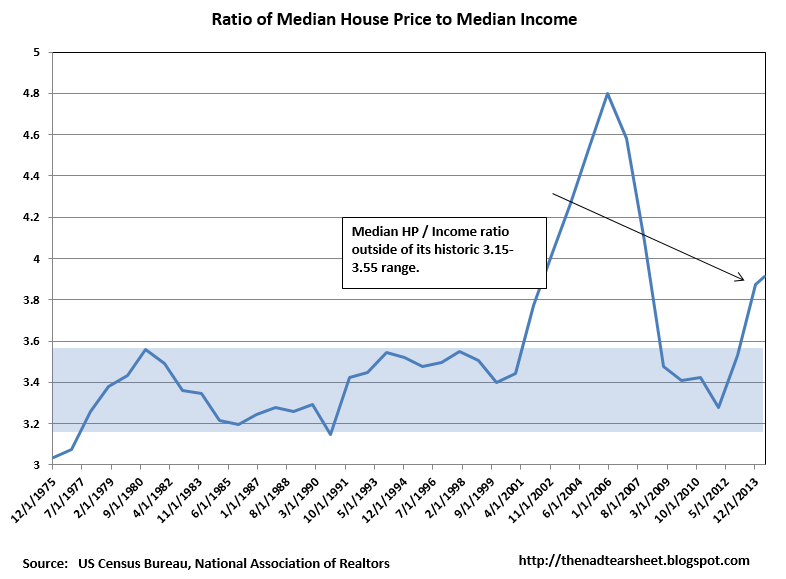

Existing Home Sales bounced back in September to 5.17 million, the highest pace this year. Sales increased everywhere but the Midwest. The median house price was $209,700, up 5.6% for the year. Total housing inventory fell 1.3% to 2.3 million homes, which represents a 5.3 month supply. 6 months supply is considered a balanced market. All cash sales fell to 24% in September, down from 33% a year ago. 20% cash buyers is more or less the historical norm.

The median home price to median income ratio is now 209,700 / 53,589 = 3.9x. Historically, that number has been in a range of 3.2 – 3.6. So house prices could be vulnerable or stagnate until we start seeing wage inflation.

Mortgage REIT CYS Investments reported earnings last night. In spite of a small bond market rally, they still experienced mark-to-market hits on their portfolio of MBS as these securities cheapened on fears of a Fed rate hike. Since TBAs correlate with existing RMBS, this means TBAs underperformed as well. This is further evidence that mortgage rates simply did not correlate with Treasuries very strongly on the bond market rally this summer. So, if a borrower says “I saw on CNBC that interest rates were going down in a big way, how come your rates aren’t falling as well?” you can explain that mortgage rates have been lagging the bond market rally all summer, and the securities that set mortgage rates simply haven’t been performing as well as Treasuries. CYS did not attribute this to the end of QE however – in spite of the drop in Fed buying, the lack of volume as refis dried up has been the dominant effect, and there is strong demand for whatever RMBS issuance remains.

Filed under: Morning Report |

Frist. Heh

LikeLike

Brent:

Are you aware of this? Seems crazy to me.

Like lenders, homeowners associations can foreclose on homes to recoup delinquent payments, an option that many have taken after waiting years for lenders themselves to foreclose, a scenario that has left homes without dues-paying owners and some HOAs strapped for cash. Nevada and about 20 other states have laws that allow HOA liens to get priority over first mortgages.

The result, according to a recent state court decision, is that homes can be put up for auction by HOAs — without the blessing of the mortgage lender — and sold, extinguishing the first mortgage and allowing the investor to get title to the home. Such sales often are for an amount equal to or slightly above the HOA dues in arrears.

LikeLike

I have never heard of that before. That is amazing..

LikeLike

Must be an older neighborhood. I’ve never run into one without a subordination clause. Most banks wouldn’t loan on a house in an HOA w/out one.

LikeLike

That is crazy.

Also John Cassidy on China.

http://www.newyorker.com/news/john-cassidy/chinese-economy-fall-off-cliff

LikeLike

Vox summs up:

“Obama’s latest plan to boost the economy? Bring back subprime mortgages

Updated by Matthew Yglesias on October 21, 2014, 3:00 p.m. ET”

http://www.vox.com/2014/10/21/7027949/mel-watt-subprime-mortgage-fannie-mae-freddie-mac

LikeLike

jnc:

Vox summs up:

…poorly. His basic point is correct, but the framing is total BS.

This hide-the-ball approach to goosing the economy has some political appeal. But it also creates lots of opportunities for bankers and other industry players to ride high on the hog during the good times, and pass the buck for their own misbehavior during the bad.

That is completely wrong. If the government is pursuing an explicit policy of encouraging the writing of riskier loans, and is explicitly underwriting those risks, it is neither the “misbehavior” of banks nor any buck-passing that results in the government taking the hit when things blow up, as Yglesias himself acknowledges is inevitable.

LikeLike

And if the banks don’t go along with more lending, the blame story is already written:

“The Mortgage Industry Is Strangling the Housing Market and Blaming the Government

By David Dayen

October 21, 2014”

http://www.newrepublic.com/article/119918/mel-watts-2014-mba-speech-and-assault-housing-regulations

The absurdity of the mortgage industry strangling itself is apparently lost on Dayen.

LikeLike

I love the idea of a bunch of people in the most competitive industry on the planet supposedly colluding to restrict credit in order to get the regulators to back off.

No one ever accused the left of having any business acumen or even common sense for that matter.

LikeLike

Brent, I won’t be around here much for a week or so as I am flying up to help clean out my Mother-in-law’s home in Westchester County. I don’t think I will have spare time but just in case do you have a gig this weekend?

On a sad but nevertheless amusing note, Coburn’s list is out:

http://www.washingtonpost.com/blogs/federal-eye/wp/2014/10/22/nine-ways-the-government-squandered-your-money-from-sen-coburns-2014-wastebook/?wpisrc=nl_fed&wpmm=1

Also this: http://www.washingtonpost.com/blogs/post-politics/wp/2014/10/21/mr-president-dont-touch-my-girlfriend/?tid=pm_politics_pop

LikeLike

Hi Mark: Two gigs this weekend.

Saturday 4:00 pm at the Nyack Halloween Parade. Should be a short 1 hour set

Saturday 10:00 pm at PieMan in Valley Cottage.

Both gigs are across the river.

LikeLike

http://online.wsj.com/articles/companies-try-to-escape-health-laws-penalties-1413938115

well how about that.

LikeLike

Federal Reserve President William Dudley, criticizing violations of banking regulations at a recent meeting with bank executives:

“The inevitable conclusion will be reached that your firms are too big and complex to manage effectively. In that case, financial stability concerns would dictate that your firms need to be dramatically downsized and simplified so they can be managed effectively.”

Sound to me like a criticism and a conclusion that would be at least as aptly applied to the government itself. In fact even more apt. The regulatory state itself is far too big and complex to be either managed effectively by elected officials or effectively navigated by those subject to its whims.

LikeLike