Markets are higher this morning after the ECB cut rates to 5 basis points and committed to start buying securitized debt and covered bonds in October. Bonds are flat as this decision had been priced in already.

Just something to think about – the “buy the rumor, sell the fact” effect. In other words, the big move for ECB QE was over the past six months, and it wouldn’t be surprising to see a sell-off in sovereigns as the announcement is out of the way and speculative players unwind their positions. Euro sovereigns are driving the US bond market at the moment.

Fun fact, 45% of global sovereign bonds yield under 1% according to Bank of America.

Denmark just cut its deposit rate to negative 5 basis points. They are in the throes of a burst real estate bubble.

The ISM Non-Manufacturing index rose to 59.6, the highest since August 2005. The manufacturing index rose to 59, and would correspond to a GDP growth rate of 5.2%. Of course manufacturing doesn’t have the impact on the US economy it used to, but still….

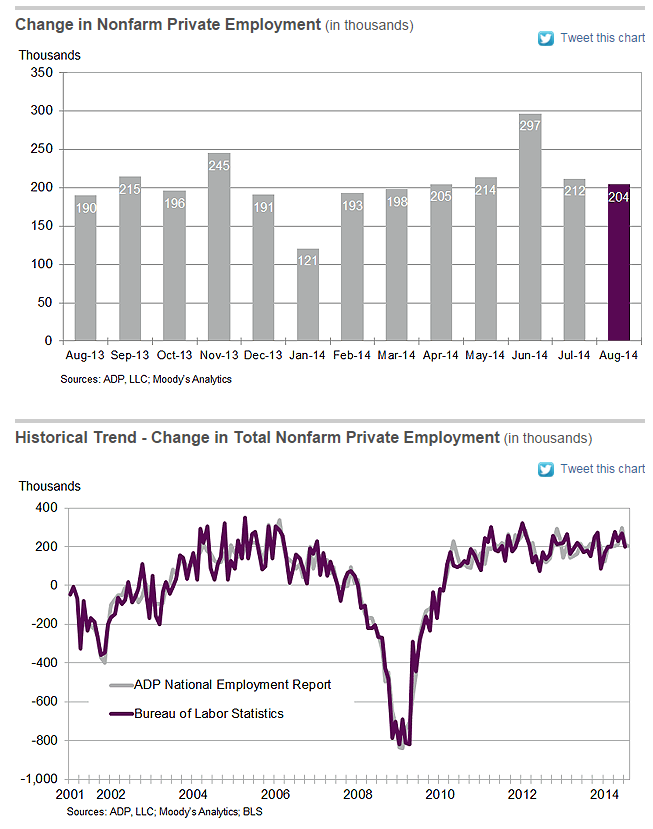

ADP is forecasting the economy will add 204,000 jobs in August. ADP has been spot-on the last couple months. The Street is forecasting 215k tomorrow.

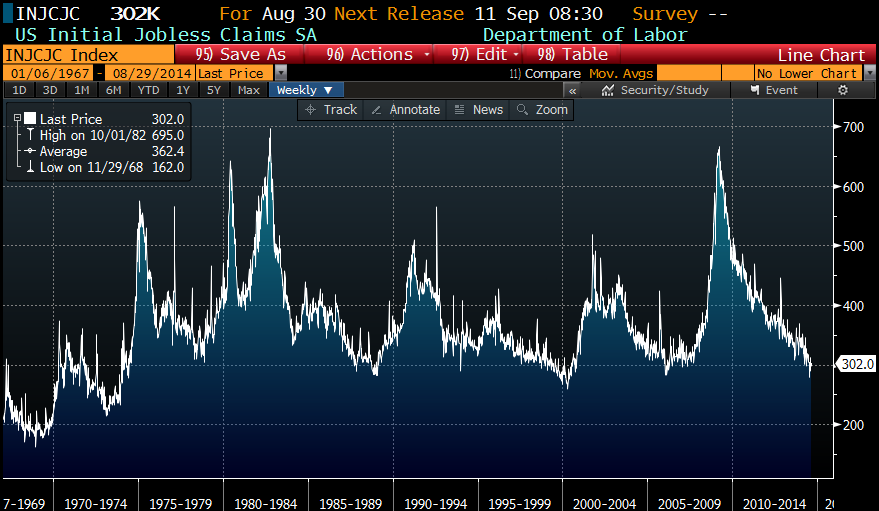

In other labor market data, announced job cuts fell 21% according to outplacement firm Challenger, Gray and Christmas. Unit Labor Costs fell .1% in the second quarter as productivity rose 2.3%. Finally, initial jobless claims ticked up slightly to 302,000. Initial Jobless Claims levels are back to boom-time levels, and as a percent of the population are back to levels not seen since the late 1960s.

What is holding back wage inflation? Pent-up deflation. As Keynes pointed out, during recessions wages should fall as the demand for labor falls. However, employers are loath to cut pay (a phenomenon called sticky wages) which means that by not cutting wages, employers are overpaying during a recession. As the recovery builds steam, therefore they are not feeling pressure to raise them either. Interesting theory, and one thing the researchers say is that once this runs its course, wages could rise more quickly than economic models suggest as businesses that kept wages low for too long are forced to play catch up. This may in fact be what was behind the language in the FOMC minutes about there being less slack in the labor market than people think. We will see tomorrow with the jobs report. Separately, the average weekly hours worked by a full time employee inched up to 46.7 hours.

Filed under: Morning Report | 21 Comments »