Markets are higher on earnings and a low initial jobless claims number. Bonds and MBS are down small.

Today is the first Thursday of the month, which means same store sales from the retailers. So far it looks like they are coming in a bit better than expected.

Initial Jobless Claims came in at 289k, the lowest level in 8 years. Bloomberg’s weekly consumer comfort index fell to 36.2.

Mortgage delinquencies fell to 6.04% in the second quarter, according to the MBA. Foreclosures fell to 2.49%.

Fannie Mae earned $3.7 billion in Q2, of which all went to Treasury. They modded 32,000 loans in the quarter as well. Delinquencies dropped to 2.05%.

The next global economic headache is the bursting of China’s real estate bubble and the potential for a protracted slowdown. There is a “buyer’s strike” going on and so far developers are not lowering prices yet. So inventory builds. Inventory is 23 months worth of sales in the top 20 cities. To put that number into perspective, 6 months is considered normal, at least in the US. This is generally how busts begin. If it becomes “the one” then trophy properties in the US, particularly the West Coast will become vulnerable.

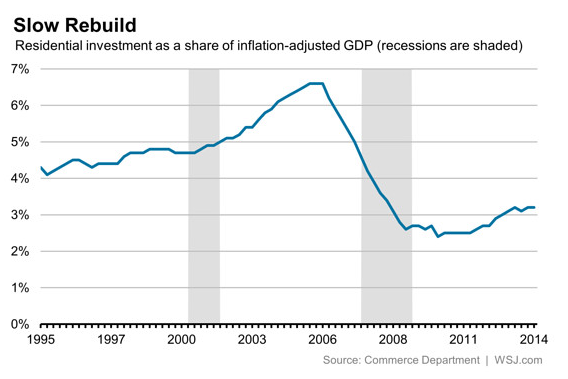

The WSJ has a good piece on the weakness of housing, particularly housing construction. As we know, housing starts have been mired below 1 million units for what seems like forever. Normalcy is around 1.5 million units historically. When you look at residential construction’s contribution to GDP, it is been about 2.5% – 3%, much lower than its pre-bubble level of 4% to 5%. Not only that, but residential construction usually leads an economy out of recession. I had hoped this would be the year starts got back to normalcy, but the homebuilders have seemed content to increase the top line through price hikes, not volume increases.

Filed under: Morning Report | 33 Comments »