Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1856.0 | 3.2 | 0.17% |

| Eurostoxx Index | 3149.1 | 9.9 | 0.31% |

| Oil (WTI) | 103.9 | 0.2 | 0.16% |

| LIBOR | 0.226 | -0.002 | -0.88% |

| US Dollar Index (DXY) | 79.7 | -0.104 | -0.13% |

| 10 Year Govt Bond Yield | 2.66% | 0.03% | |

| Current Coupon Ginnie Mae TBA | 105.7 | -0.2 | |

| Current Coupon Fannie Mae TBA | 104.3 | -0.1 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.41 |

The Fed released the Beige Book yesterday. Overall, it shows activity increasing since last month, which isn’t surprising – the big question is whether it is a rebound from weather-related weakness or something sustainable. Certainly some of the manufacturing data we saw recently (industrial production, capacity utilization) seems to imply the latter. I think people don’t appreciate the industrial production reports that came out yesterday – the headline numbers for March were great on their own, but the upward revisions to February numbers were huge.

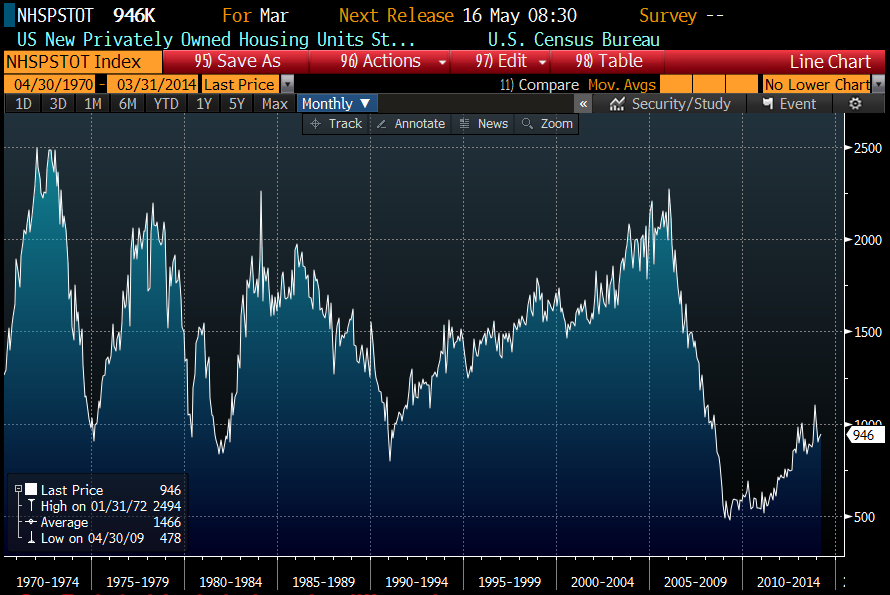

On the labor front, wage pressures remained contained, except for the Dallas district. Most districts are reporting labor shortages in skilled labor. On the negative side, food prices are rising, and rising food prices plus stagnant wages can be an economic damper. The main takeaway is that the economy seems to be accelerating and it is looking like it is more than just a rebound from weather-related weakness. That said, the weakness in housing starts continues to be a head-scratcher. We are still at levels that represent the bottoms of previous recessions. Any excesses of the bubble were corrected long ago.

Filed under: Morning Report | 56 Comments »