Vital Statistics:

|

Last |

Change |

Percent |

| S&P Futures |

1837.7 |

1.5 |

0.08% |

| Eurostoxx Index |

3147.5 |

-2.7 |

-0.08% |

| Oil (WTI) |

94.69 |

0.7 |

0.78% |

| LIBOR |

0.237 |

0.000 |

0.11% |

| US Dollar Index (DXY) |

81.05 |

0.135 |

0.17% |

| 10 Year Govt Bond Yield |

2.83% |

-0.01% |

|

| Current Coupon Ginnie Mae TBA |

105.2 |

0.2 |

|

| Current Coupon Fannie Mae TBA |

104 |

0.1 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.42 |

|

|

Markets are flattish this morning after UPS missed and housing starts came in a bit better than expected. Bonds and MBS are up.

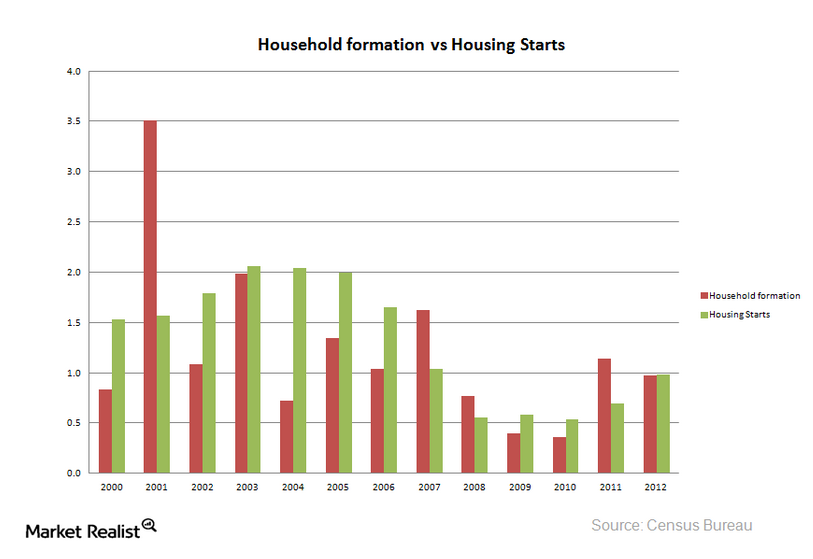

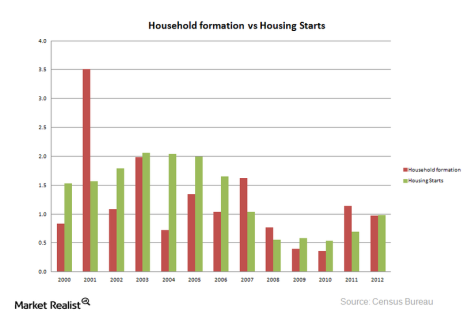

Housing starts came in at 999,000 and building permits came in at 986,000. Single Fam and Multi-fam both fell, although single fam is up year-over-year and multi fam is down. Starts are up small from a year ago, and down from the huge 1.1 million print we saw in November. While a million starts is a champagne-popping number in the context of the Great Recession, it is still a lousy number historically. Pre-bubble, starts averaged about 1.5 million a year, and routinely topped 2 million a year early in recoveries. We have spent years below the nadir or prior recessions which usually exhibited sharp V-type crashes and recoveries. Once household formation numbers recover (and we have tremendous pent-up demand here), we will find ourselves with a shortage of homes.

Industrial Production came in as expected at .3%, and capacity utilization ticked up to 79.2%. The average since the 1960s has been 80.6%, so we are approaching normalcy here after bottoming at 66.9% in 2009. The prior low was 70.9% during the nasty 81-82 recession. Yet another data point showing just how rough the past 5 years have been.

Freddie Mac has an interesting chart showing how depressed the mortgage business has been, but also why forecasts might be a little too gloomy. They look at home sales relative to housing stock (basically housing turnover) and then compare it to purchase applications. Two things jump out at me: first, turnover (the blue line) is very low at the moment, which probably reflects the underwater borrower phenomenon. People can’t move if they can’t sell. But second, note that as housing turnover increased recently, purchase applications (the green line) remained more or less flat – that is evidence of the cash / professional buyer who has been dominating the marketplace. Both are temporary headwinds for mortgage bankers that will abate as home prices continue to rise. Underwater homeowners will eventually get right-side up and will be able to sell. Professional investors will begin to balk at the higher prices and may even begin to sell. The purchase business will benefit from a number of major big trends going forward: (a) a “payback” of the low household formation numbers over the last few years, (b) increasing turnover as underwater home owners finally get right side up, and (c) the professional investor’s exit from the distressed home market (the green line will catch up to the blue line)

Zillow has a

study showing that targeted lending areas had the biggest drops in real estate prices. This is unsurprising given that the chance of a home becoming worthless is higher in places like Detroit or Harrisburg than it is in, say Stamford CT or San Diego CA. Unwittingly the study also proves a point that I have been making for quite some time – that the underlying logic to the Community Reinvestment Act is flawed. Essentially, the CRA says that borrowers with the same characteristics (FICO / LTV) should get the same rate. And if they don’t get the same rate, then that is prima facie evidence of discrimination. That logic is perfectly valid for some forms of credit – particularly credit cards, installment debt, etc. However, mortgages are different. They are secured loans, and when a lender looks at a secured loan, they take into account not only the probability of getting paid (via credit scores), but also the characteristics of the underlying collateral. The CRA proponents assume a house is a house is a house and FICO is all that matters. But the study shows that isn’t the case – the lender has to take into account what happens if they are not paid. And because the underlying homes in targeted lending areas are more likely to have huge price swings (particularly to the downside), when lenders charge more for loans in these areas, they are not guilty of discrimination – they are simply properly pricing risk. Therefore, the CRA isn’t correcting some purported wrong, it is simply an excuse for wealth redistribution.

Filed under: Morning Report | 19 Comments »