Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1807.0 | 2.0 | 0.11% |

| Eurostoxx Index | 2981.6 | 1.6 | 0.05% |

| Oil (WTI) | 97.71 | 0.1 | 0.06% |

| LIBOR | 0.243 | 0.002 | 0.73% |

| US Dollar Index (DXY) | 80.22 | -0.098 | -0.12% |

| 10 Year Govt Bond Yield | 2.85% | -0.01% | |

| Current Coupon Ginnie Mae TBA | 104.6 | 0.3 | |

| Current Coupon Fannie Mae TBA | 103.8 | 0.4 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.48 |

World markets are higher this morning after Friday’s stronger-than-expected jobs report. Bonds and MBS are up small as well.

The upcoming week is relatively data-light, so the markets will be left to fret about the FOMC meeting next week. The Street seems to be handicapping a December tapering at 50/50. Don’t forget, even if the Fed does begin to reduce asset purchases, it doesn’t necessarily follow that MBS purchases will drop. In fact, most observers think that the Fed will only reduce Treasury purchases and maintain their current rate of MBS purchases. The only reason why the Fed may want to reduce MBS purchases would be to reflect that the Fed’s current purchase rate of $40 billion a month is much higher as a percentage of total MBS issuance than it was a year ago. This is because overall issuance has fallen since the refi boom ended.

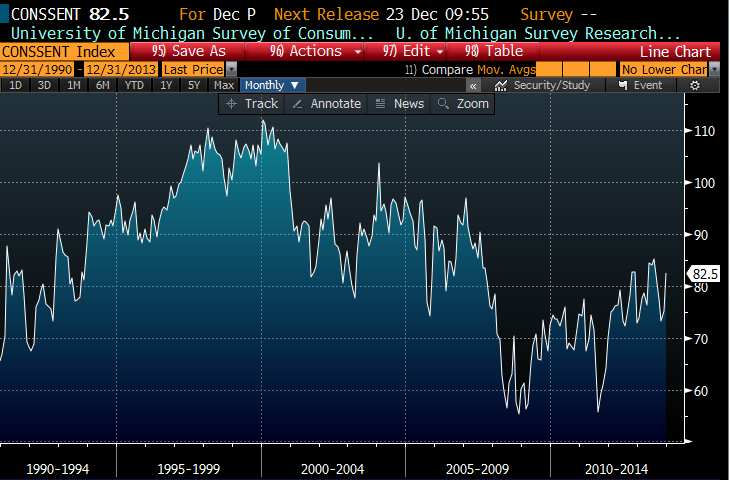

Consumer sentiment is on the rebound, but is still below what one would call “normalcy.” The chart below is of the University of Michigan Consumer Sentiment Index. You can see that we are close to post-bubble highs, but are still mired in that early 90s malaise. Consumer sentiment is a big driver of real estate activity – in fact the CEO of KB Home said that consumer sentiment matters more than interest rates, at least to the homebuilders. Things are improving, albeit slowly.

It looks like we have some sort of budget deal in Washington, which should at least take the possibility of another government shutdown off the table. It looks like some of the sharper edges of the sequester will be sanded down, and it will be paid for by increased pension contributions from Federal workers and increased airport security fees. It is a “kick the can down the road” agreement that will at least prevent some fireworks beginning next year.

The FHA reduced the upper limit on FHA mortgages in high cost areas from $729,750 to $625,500. The jumbo market has been back for quite some time, and FHA is happy to let upper income borrowers access private capital.

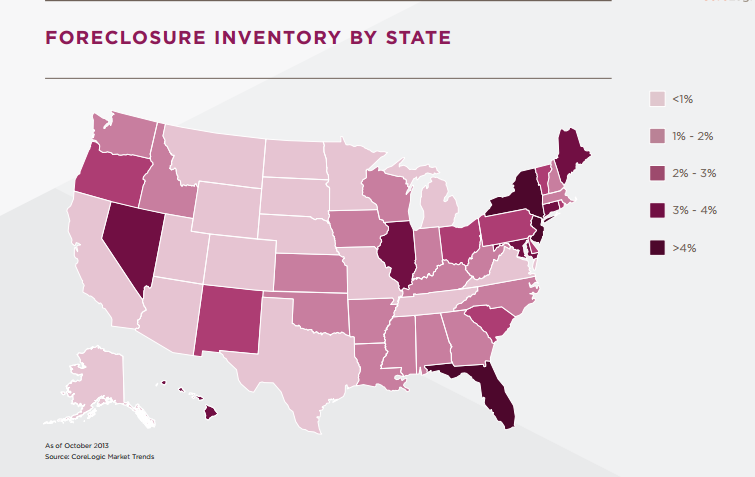

Completed foreclosures dropped 30% from a year ago, and 26% from last month, according to CoreLogic. The foreclosure pipeline is 900k homes, which is a big drop, however we are still far from “normalcy,” which would be about a quarter of that number. The judicial states still have the highest level of foreclosure inventory, as you can see from this foreclosure heat map.

Filed under: Morning Report |

See this, on Fed policy:

Last week we discussed 3% down mortgages and lower qualifying scores. I think they pose a known risk. I also think continuing QE poses a known risk. And I worry that it is the confluence of these risks that is destabilizing.

LikeLike

Worth a read:

http://www.theguardian.com/world/2013/dec/08/david-simon-capitalism-marx-two-americas-wire

LikeLike

The ACLU is going after FHFA over its position on eminent domain (saying that loans made in municipalities that pursue eminent domain are uninsurable).

https://www.aclu.org/racial-justice/aclu-and-center-popular-democracy-file-foia-lawsuit-over-efforts-limit-municipalities

It isn’t enough that borrowers in higher income neighborhoods subsidize borrowers in low income neighborhoods, the ultimate lenders need to get screwed as well…

LikeLike

So, their saying that a mortgage in a municipality with a history of trying to seize that property for “mortgage adjustment” have to be insured? Really, that’s a reasonable position? That’s equal protection?

We are well and truly fucked, no?

LikeLike

“If the owners of the securities refuse to sell at fair market prices, the city proposes to use eminent domain to buy them.”

If they refuse to sell then the price probably isn’t fair or set by the market.

LikeLike

They do have a point here:

“If eminent domain can be used in blighted neighborhoods to seize property that will be turned over to private developers, then eminent domain should also be available to help homeowners stay in their homes and to stabilize neighborhoods”

Kelo was easily one of the worst, if not the worst, Supreme Court decision in my lifetime and this whole scheme flows directly from that.

LikeLike

Plus , through zoning, a municipality can be the cause for the loss of value.

Any homeowners here with the belief that your home value can only go up? Who believes that?

LikeLike

For Obamacare supporters, is Kaus right? If so, what do you think about it?

http://dailycaller.com/2013/12/08/big-obamacare-payoff-for-tax-cheats/

LikeLike

Really interesting Kaus piece on Income inequality.

http://dailycaller.com/2013/12/09/the-great-macguffin/

I disagree with his solutions, but the why ‘s of it are thought provoking.

Really.

LikeLike

It’s working!

LikeLike

Mark, you may find this interesting on internal union politics and the effect on labor negotiations at Boeing.

http://www.washingtonpost.com/blogs/wonkblog/wp/2013/12/09/what-happens-when-a-union-starts-acting-like-a-corporation/

LikeLike

Thanx, JNC.

LikeLike

Obviously, the solution is more centralized control.

http://m.theatlantic.com/health/archive/2013/12/you-re-getting-too-much-healthcare/281896/

LikeLike

Absolutely hilarious.

http://dailycaller.com/2013/12/09/fight-erupts-between-lefty-scribe-and-other-reporters-awesome-breakdown-ensues/#ixzz2mzfwprZH

Seriously, this is very funny.

LikeLike

Absolutely hilarious follow up to earlier link I posted about flame war betwixt (see what I did there?) Eli Lake and Mike Elk.

http://dailycaller.com/2013/12/09/reporter-unravels-after-story-publishes/

LikeLike

Certain chickens come home to roost:

“Whose sarin?

Seymour M. Hersh

Barack Obama did not tell the whole story this autumn when he tried to make the case that Bashar al-Assad was responsible for the chemical weapons attack near Damascus on 21 August. In some instances, he omitted important intelligence, and in others he presented assumptions as facts.”

http://www.lrb.co.uk/2013/12/08/seymour-m-hersh/whose-sarin

LikeLike

Welcome back, BTW, jnc! Hope your time off has left you tanned, rested and ready.

LikeLike

Worth a read.

Apparently it’s not just separate locations for the same businesses that are counted together for the PPACA compliance rules (i.e, the over 50 worker threshold), but if multiple legal businesses have the same owner as well.

http://www.washingtonpost.com/business/on-small-business/health-care-laws-aggregation-rules-pose-a-compliance-nightmare-for-small-businesses/2013/12/09/87b2dcc6-611d-11e3-bf45-61f69f54fc5f_story.html?hpid=z2

LikeLike

JNC, I think this is because IRS rather than DOL definitions control. Under labor law we use the “enterprise” concept [all locations of the same business] but under tax law same owner faces consolidated returns for all his/her/its businesses.

ACA got tied into tax law for enforcement so it is another hybrid like ERISA that labor lawyers HATE because they [until very recently “we”] cannot get it quite right.

QB probably has some knowledge as to how this all fits together. Actually, NoVA probably does. Better to see your lobbyist at a time like this.

LikeLike

It’s all for the greater good WingNut! It’s not falsifiable! Like AGW!

Jesus, will no one rid us of these tiresome trolls?

LikeLike

Yes, but as the article notes, that’s going to cause a plethora of problems for things like the mandate, depending on how much of an equity stake makes the owner liable.

Politically, I think it will make opposition to the PPACA from certain segments go from mere complaining and grousing to actively working to repeal it.

The ironic thing is that I believe that the employer mandate is one of the items that has been viewed as secondary that could be repealed without radically undermining the law.

http://www.washingtonpost.com/blogs/wonkblog/wp/2013/07/02/obamacares-employer-mandate-shouldnt-be-delayed-it-should-be-repealed/

LikeLike