Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1788.0 | -3.4 | -0.19% |

| Eurostoxx Index | 2988.7 | -25.2 | -0.84% |

| Oil (WTI) | 97.06 | 1.0 | 1.06% |

| LIBOR | 0.242 | 0.001 | 0.23% |

| US Dollar Index (DXY) | 80.77 | 0.180 | 0.22% |

| 10 Year Govt Bond Yield | 2.84% | 0.06% | |

| Current Coupon Ginnie Mae TBA | 104.7 | -0.1 | |

| Current Coupon Fannie Mae TBA | 103.4 | -0.4 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.43 |

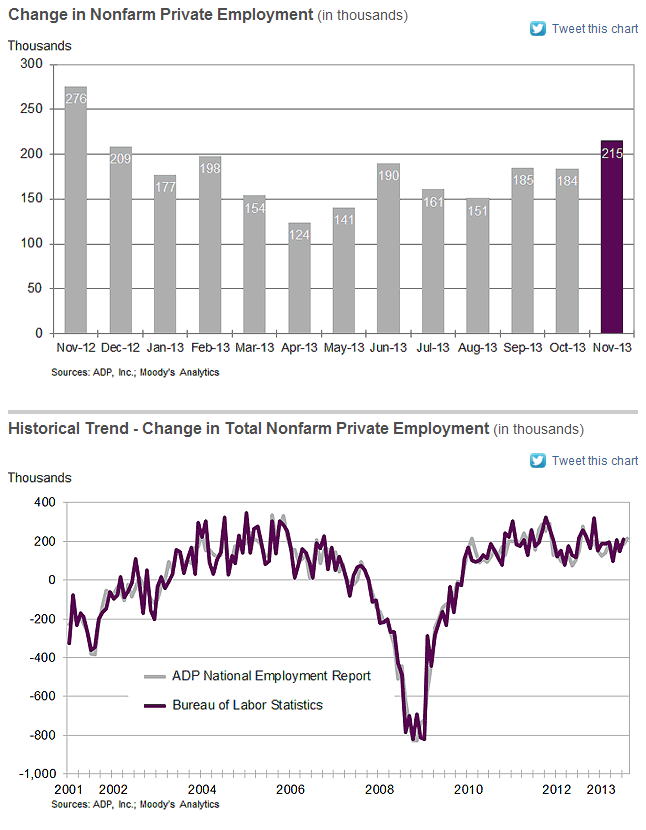

Markets are lower this morning after a strong ADP employment report. Bonds and MBS are down. Later on today, we will get the ISM services index and new home sales.

The ADP employment report showed 215k jobs added in November, above the 170k estimate. October was revised upward from 130k to 184k. The forecast for Friday’s payroll number is 175k. Lately, ADP has not been a great predictor of the upcoming jobs report, so bear that in mind. According to JP Morgan, the street is leaning heavily short going into the number, so the reaction to a strong report could be muted. Conversely a weak report could send bonds flying. A classic case of “buy the rumor, sell the fact.”

Mortgage applications fell 12.8% last week, which isn’t surprising given the holiday. Purchases dropped 4.1% while refis dipped 17.5%. Mel Watt is supposedly going to be confirmed next week and the rumor is that he wants a HARP extension for loans through 2010. So we could see some sort of refi wave, although it won’t be anything like 2012 was.

Smaller mortgage lenders have been picking up market share, according to Inside Mortgage Finance. As of Q3, they had a 60% market share vs 39% share in 2009. One reason – the big banks have tightened credit standards and are taking longer to process loans than smaller lenders. LOs, this is a good selling point to bring up with your realtor contacts – what realtor wants to get paid later rather than sooner?

Detroit has filed for bankruptcy, and it looks like pensions and creditors will likely take a hit. Detroit owes more than $18 billion and cannot perform even basic services. Half of that debt is retiree benefits. If Detroit was a company, they would be filing Chapter 7, not Chapter 11. Given the crime rate in the city, I don’t know what brings business back into Detroit. Almost on cue, Fitch, which recently cut Chicago’s rating, is predicting there will be more muni downgrades than upgrades in 2014.

Here is what the CFPB is going to be up to over the next few months.

Bill Gross’s Investment Outlook is pretty good: If you look at asset prices, there is an implied growth rate built in. But that implied growth rate is based in part on risk-free asset prices that are being manipulated by the Fed. That implied growth hasn’t happened yet, and it may never materialize. Then what?

Filed under: Morning Report |

First!

Heh!

Now, read this article and tell me that the preening and sheer stupidity of the author doesn’t make you ill.

http://m.newyorker.com/online/blogs/comment/2013/12/my-cancelled-policy-and-my-values.html

That this article was deemed publishable says a lot about who The New Yorker thinks it’s readership is.

Finally, WTF is the umlat over the second e in “preexisting” for?

Really, this article is beyond belief. Seriously.

LikeLike

I think she makes a couple of good points, the one about “pre-existing” and the one she did not see – that high deductibles are the best way to reduce non-essential health care visits by hypochondriacs.

IT seems to me a lot of folks are complaining about the “high deductibles” who haven’t done the arithmetic for themselves. This writer was about to pay $1300/mo for a low deductible and now she could pay $800/mo for a high deductible that allowed free checkups. $5K a year cheaper to handle the out of pocket on her own. I’ll bet the arithmetic works out for her and she still has catastrophic coverage, so it’s no biggie.

I think you just object to someone wanting to be part of an

AbominationExperiment.NoVA?

LikeLike

McWing:

A few observations on the New Yorker article.

I’ve had high blood pressure since I was in my thirties. I take ten milligrams of a generic beta blocker every morning, which has successfully kept my hypertension controlled. By doing so, I hope to prevent or postpone some of the possible consequences of hypertension—strokes, heart attacks—which are both debilitating and costly. That’s good preventive thinking for me, and good social policy…

In what way is it “good social policy”? I presume that she thinks that by lowering the risk of a stroke or heart attack, she is somehow saving “society” or taxpayers some expense. I would like to see the evidence of this, because it is not at all intuitively obvious to me that it is true. It could in fact be that, from a societal cost/benefit point of view, it is more costly to pay for her high blood pressure medicine than to let her take her chances on having a heart attack and dying on, say, her 65th birthday just before she starts collecting Social Security and entering the stage of life during which health care costs really start to climb. If “good social policy” is really to factor into her decision, then these kinds of sober analyses really need to be done.

Like many such common (pre-existing) conditions that people seek help for, it could have resulted, before Obamacare, in my being denied coverage if we were to lose our current policy.

She says she is 52, and has been treating her high blood pressure since she was in her thirties. So is it the case that she has maintained the same health care policy since prior to her diagnosis with high blood pressure? If not, how did she manage to get her current policy with this pre-existing condition?

Essentially, at some point, anyone would have a medical condition resulting in an increased rate or denial—sometimes because of behavioral issues (e.g. smoking) but most of the time just because of genetics (a very harsh standard).

That is indeed a harsh standard, and not one I want governing my life, or those of other people.

This is just a denial of reality. If a person has some genetic condition that produces large health care costs, that burden will, as a result of the nature of reality, have to be borne by somebody. Either the person himself will have to suffer without getting care, or he will have to pay for the care himself, or someone else will have to pay for the care. This is not a political judgement. It is a recognition of the nature of reality. Her desire to live in a fantasy world where no one bears the burden of genetic conditions doesn’t alter the world as it exists. Someone’s life will be “governed” by the need to pay for those costs or suffer the results of not paying them.

To be clear: I’m not happy to be paying more in the short term, and it may be a struggle at times. I wish other self-employed people didn’t have to shoulder so much of the burden. I wish we had a single-payer system, but that seems wildly unrealistic.

More fantasy land. A single payer system doesn’t change the fact that someone will be shouldering the burden. It just changes the method by which the person(s) who shoulders the burden gets determined.

Vaccination provides more effective protection—so-called herd immunity—when more of us are vaccinated. Universal health insurance works in something like the same way

No it doesn’t. The benefit of such “herd immunity” accrues equally to all members of the herd, who are all less likely to catch the disease when someone else gets vaccinated. It is in that sense a typical public good in the economic sense. The benefits of “universal health insurance” accrue to individuals who get the insurance without paying the true cost for it, not to everyone equally. Other individuals not only accrue no benefits, but actually accrue a loss because they are subsidizing the benefit that accrues to others.

we are better off as a society—more compassionate, but also healthier—when we can all get the care we need.

Simple-minded treacle. She totally ignores the fundamental problem, which is that getting the “care we need” has costs.

LikeLike

Scott, this WSJ story is behind the paywall.

Opinion

Wallison: Get Ready for the Next Housing Bubble

Mel Watt is a long-time champion of mortgage quotas for affordable housing. Here we go again.

By

Peter J. Wallison

Dec. 4, 2013 6:48 p.m. ET

Could you reprint it here? Thanx.

LikeLike

Yeah, I read that this morning. Here it is:

By Peter J. Wallison

Dec. 4, 2013 6:48 p.m. ET

By banning filibusters of most executive-branch and judicial nominations, the Democrats have done historic damage to the Senate. This will have long-term consequences for the nation, but the most significant initial fallout will likely be the confirmation of Rep. Mel Watt (D., N.C.) to head the Federal Housing Finance Agency, which regulates mortgage giants Fannie Mae FNMA +0.73% and Freddie Mac. FMCC -0.79%

Since these two government-sponsored enterprises became insolvent in September 2008, FHFA has also been their conservator, with the power to control their operations and policies. Mr. Watt is a good man, but he is a man of the left, and he will use his control of Fannie and Freddie to return to the policies that brought on the mortgage meltdown in 2007 and the financial crisis in 2008.

Just before the crisis, 58% of all U.S. mortgages—32 million loans—were subprime or otherwise weak. Of these, 24 million, or 76%, were on the books of government agencies, primarily Fannie Mae and Freddie Mac. This shows incontrovertibly that the government itself was the source of the demand for these low-quality loans.

The U.S. had once been known for the high quality of its mortgage loans, but this began to change once Congress enacted affordable-housing goals in 1992. Under that legislation, Fannie and Freddie—which were then, as now, the standard-setters for the mortgage market—were required by the Department of Housing and Urban Development to purchase an increasing quota of loans to borrowers at or below the median income where they lived.

As HUD increased this quota between 1992 and 2008, Fannie and Freddie were forced to reduce their underwriting standards—accepting loans with 3% down payments in 1995 and 0% down in 2000—in order to find eligible borrowers. Mortgage financing is a competitive business, and as Fannie and Freddie’s underwriting standards deteriorated, they spread to the wider market.

Borrowers who could afford down payments of 10% or more were happy to take loans with 3% or nothing down and buy larger homes. The increased borrower leverage and the sheer number of new borrowers fed an enormous housing price bubble between 1997 and 2007. When the bubble collapsed in 2007 and 2008, an unprecedented number of mortgage defaults drove down housing values 30% to 40%—and drove Fannie and Freddie into insolvency.

A government bailout of more than $180 billion enabled Fannie and Freddie to continue operating after September 2008 under FHFA’s acting director, Edward DeMarco. A nonpolitical civil servant, Mr. DeMarco has seen it as his duty to protect taxpayers from another bailout. To this end, he has increased the underwriting standards that Fannie and Freddie employ before they acquire a loan, raised the fees they get for guaranteeing mortgage-backed securities, and limited the scope of the affordable-housing goals. The two enterprises are now profitable and able gradually to repay the government.

Mr. DeMarco’s actions have aroused the opposition of the left. Critics complain that his underwriting standards are too high, meaning that many low-income borrowers will not be able to buy homes. This is the same argument community activists made when they pressed Congress to adopt the affordable-housing goals. Today, the idea underlying the goals goes by a new term—”opening the credit box.” But the objective is the same: reduce underwriting standards so borrowers who have poor credit records and don’t have down payments will be able to buy homes.

This is exceptionally bad policy. Even Barney Frank, the principal backer of the affordable-housing goals for much of his career in Congress, admitted in 2010 that “it was a great mistake to push lower-income people into housing they couldn’t afford and couldn’t really handle once they had it.”

The only way to maintain a stable housing market is by requiring reasonable underwriting standards. This means a down payment of at least 10%, a FICO credit score above 660, and a debt-to-income ratio, after the mortgage is closed, of no more than 38%. When those standards were generally in force between 1970 and 1992, mortgage defaults in the U.S. were under 1% and the national homeownership rate was 64%—about where it is today after all the foreclosures in recent years.

Unfortunately, Mr. DeMarco’s underwriting standards will almost certainly change, and for the worse, once Mr. Watt is in charge of the Federal Housing Finance Agency. The stage has already been set. The Consumer Financial Protection Bureau (CFBP), an agency created by the Dodd-Frank Act, has outlined a minimum quality mortgage that will permit a borrower to get a loan with a 3% down payment and a FICO credit score well below 660. Under Dodd-Frank, a lender could be subject to severe penalties if it turns out that the borrower cannot repay the loan—but the CFPB’s rule protects the lender against liability if Fannie and Freddie’s automated underwriting systems approve the loan.

Enter Mr. Watt. The North Carolina congressman is a consistent, long-time supporter of affordable-housing quotas. He joined Barney Frank in 2003 to block the Bush administration’s attempt that year to increase government oversight of Fannie and Freddie. And in 2007 he cosponsored legislation that would have pushed the two GSEs even deeper into the subprime mess. One can be sure that there will be many low-quality mortgages approved by Fannie and Freddie on his watch.

In August, the six financial regulatory agencies that Dodd-Frank directed to define a high-quality mortgage (the Federal Reserve, Comptroller of the Currency, Federal Deposit Insurance Corporation, Securities and Exchange Commission, FHFA and HUD) reported that they’re quite happy with the CFPB’s minimum-quality loan. Despite the mandate in Dodd-Frank, they decided not to propose a high-quality mortgage.

The six agencies reported that mortgages that met the CFPB’s low standards between 2005 and 2008 had a default rate of 23%. Incredibly, they were still OK with that. Why? We are “concerned,” they said, “about the prospect of imposing further constraints on mortgage credit availability at this time, especially as such constraints might disproportionately affect groups that have historically been disadvantaged in the mortgage market, such as lower-income, minority, or first-time home buyers.”

As we gaze into the open credit box the financial regulators have set before us, is there any doubt where the housing market is headed?

Mr. Wallison is a senior fellow at the American Enterprise Institute.

LikeLike

Thanx. I believe that I wrote in favor of deMarco here but I did not know enough about Watt to criticize his nomination. Brent was worried about him, so I was too, based on Brent’s concern, but I had no hard knowledge.

This article makes clear the danger.

“Despite the mandate in Dodd-Frank, they decided not to propose a high-quality mortgage.

The six agencies reported that mortgages that met the CFPB’s low standards between 2005 and 2008 had a default rate of 23%. Incredibly, they were still OK with that.”

I will keep this in mind.

LikeLike

Shorter Mark Pryor ad: Sorry about the Obamacare vote you drooling Jesus Freaks!

http://www.katv.com/story/24129155/pryors-new-ad-highlights-his-faith-in-the-bible

LikeLike

Mark,

First I want her to choke on the law she is forcing on the rest of us. Second, her preexisting complaint might actually have some resonance if she’d actually been denied coverage. Third, this is no “experiment” as the n=everybody. It’s more akin to a prison rape. What’s nauseating is the suthor’s moral preening as justification for a immoral law and her unarguable stupidity.

LikeLike

WTF is the umlat over the second e in “preexisting” for?

It’s New Yorker house style to use the umlaut to designate a new syllable when two vowels are adjacent. It’s unique to them and ignored by everybody else. I use the hyphen like Mark did but what do I know?

LikeLike

I haven’t seen the movie Twelve Years a Slave , but this is funny.

http://freebeacon.com/blog/12-years-a-slave-is-driving-people-batty/

And racist. I denounce myself!

LikeLike

In my defense of above, this.

http://www.newrepublic.com/blog/jonathan-chait/my-rodney-king-moment

LikeLike

When obama says “government is us” I think he really means “all your base are belong to us.”

http://www.realclearpolitics.com/video/2013/12/04/obama_government_is_us.html

LikeLike

The problem with the high deductibles in the ACA plans is that they are packaged with the preventive benefits/no-cost sharing*. so they’re not true catastrophic care. not when you get no-cost sharing services with them. also, if you buy a catastrophic plan, you don’t qualify for the tax subsidies. it’s also limited. I couldn’t buy one b/c I’m 35 and don’t qualify for one of the “hardship exemptions.” have to 30 or younger.

*not the same as the essential health benefits.

LikeLike

The problem with the high deductibles in the ACA plans is that they are packaged with the preventive benefits/no-cost sharing*.

I thought that was a feature, NoVA, not a glitch. Please explain why the net result is not cost effective. I really am interested and don’t understand this part.

LikeLike

I guess they ran out of other people’s money.

http://www.gallup.com/poll/165935/nearly-half-younger-southern-europeans-underemployed.aspx

LikeLike

Scott — it’s been done. See the “heart disease and stroke” section of http://content.healthaffairs.org/content/28/1/42.full

“An early CEA, now a classic, shows that the accumulated costs of treating hypertension are nonetheless greater than the savings, because many people, not all of whom would ever suffer heart disease or stroke, must take medication for many years.”

LikeLike

nova:

Scott — it’s been done. See the “heart disease and stroke” section of…

Thanks for that. It doesn’t surprise me in the least. And those studies are only looking strictly at medical costs. They don’t even consider the effects of prevention on things like tax revenue and SS benefit expenditures. I would imagine that there is a high probability that preventative measures end up increasing government costs even outside of medical expenditures.

Which brings us back to the woman’s claim about “good social policy”. She, I suspect, is both so gullible and so blinded by her own moral self-righteousness that she actually does believe that prevention is not only good for her (an obvious truism) but is also a net “social” benefit rather than cost. But surely many of those politicians (eg Obama) who used this claim to justify the costs of O-care know it is complete bunk. If the fact wasn’t plain already, it becomes clearer and clearer that the passage of O-care was built on a mountain of lies. It also shows that, contrary to their claims about themselves, people like Obama are in fact highly driven by ideology and not just “what works”, since study after study shows that what they want does NOT “work” to accomplish what they claim.

LikeLike

Also, don’t forget the Oregon Medicaid study. The implications of which are completely being ignored.

http://www.nationalreview.com/corner/348287/game-changing-oregon-medicaid-study

Fuck it, it’s only money.

LikeLike

McWing:

Also, don’t forget the Oregon Medicaid study. The implications of which are completely being ignored.

Yup. Yet another sign that the left is driven by ideology, not results.

LikeLike

The libertarians are coming!

http://www.politico.com/blogs/media/2013/12/radley-balko-joins-washington-post-178831.html

LikeLike

Mel Watt is a CRA guy to the bone.. All he cares about is low-income lending..

LikeLike

Scott, don’t discount this woman’s idea of “good social policy” is her continued living so she can keep “contributing” to whatever moronic coercive policies she want’s the Federal government to undertake. Remember, for nanny’s preeners like her it’s less important how she lives her life, what’s important is her ability to control how I live my life.

LikeLike

McWing:

Scott, don’t discount this woman’s idea of “good social policy” is her continued living so she can keep “contributing” to whatever moronic coercive policies she want’s the Federal government to undertake. Remember, for nanny’s preeners like her it’s less important how she lives her life, what’s important is her ability to control how I live my life.

I think that is an apt description of politicians of the left, especially hyper-arrogant ones like Obama, and it is possibly true of the author too. But I suspect that your more average, non-professional leftist like the author just unquestioningly believes the bunk that is fed to them by the likes of Obama, because it helps them to justify in reason their otherwise emotion-driven (ie non-rational) politics.

LikeLike

From Ace, on my particular hobby horse. This guy is absolutely right.

There is two trends going on which should be of equal concern to all members of Congress. One is that we have had the radical expansion of presidential powers under both President Bush and President Obama. We have what many once called an imperial presidency model of largely unchecked authority. And with that trend we also have the continued rise of this fourth branch. We have agencies that are quite large that issue regulations. The Supreme Court said recently that agencies could actually define their own or interpret their own jurisdiction.

LikeLike

I thought Democrats hated health insurance companies? How are Democrats defending this ?

http://washingtonexaminer.com/how-obama-wants-to-sweeten-the-bailout-for-insurers-under-obamacare/article/2540182

LikeLike

The piece about Mel Watt should disabuse anyone with a remotely rational mind that there is nothing, absolutely nothing, “free market” about the U.S. residential real estate market and that the housing bubble was not simply the result of CDO squareds and Wall Street Sharpies.

I don’t know why I continue to bang my head against that wall on PL, but I guess I am just a glutton for punishment…

LikeLike

Because a 25% default rate is ok with them. WE CAN ALWAYS PRINT MORE MONEY!

It’s that simple for them.

LikeLike

I suspect the vast majority of that 25% were strategic defaults from professional investors.

LikeLike

Brent:

I suspect the vast majority of that 25% were strategic defaults from professional investors.

That would be a really interesting stat to know. Does it exist?

LikeLike

Michael Cannon* at Cato testified about the presidential powers thing.

http://townhall.com/video/catos-michael-cannon-if-govt-doesnt-have-to-follow-laws-why-should-we-n1757347

*disclosure — I know him.

LikeLike

Cannon’s the left’s new Cruz who was the new Palin who was the new Norquist who was the new…

LikeLike

I don’t think we have any supporters here anymore, but if there are any increase-the-minimum-wage lurkers out there, I am curious as to what justification there could possibly be for a federal minimum wage, as opposed to a state minimum wage. Given that local economies differ drastically throughout the country, with different housing costs, different price scales for the same goods, and different costs of living in general, how could it possibly make any sense to standardize the actual minimum wage across the whole nation, even we did accept the “social” justification for a minimum wage in theory?

LikeLike

That would be a really interesting stat to know. Does it exist?

You would have to look at the NOO (non owner-occupied) loans from those years and look at default rates. I am sure the Mortgage Bankers Association has those numbers, but the data won’t be free.

I don’t know for a fact if they were strategic, but we saw a deluge of defaults as the real estate market rolled over, but before the economy rolled over. That would signal strategic defaults, not borrowers getting into trouble.

LikeLike

Brent:

That would signal strategic defaults, not borrowers getting into trouble.

Yes, indeed. That is very interesting.

LikeLike

Scott, tons of unions peg their wages to the Federal Minimum wage.

LikeLike

I am curious as to what justification there could possibly be for a federal minimum wage, as opposed to a state minimum wage.

To prevent a “race to the bottom” with companies moving from highly regulated (and high cost) states to lower ones..

LikeLike

Brent:

To prevent a “race to the bottom” with companies moving from highly regulated (and high cost) states to lower ones.

I realize I am probably preaching to the converted, but…

I don’t think this justifies it, because in fact a federal min wage prevents a lot more than just a “race to the bottom”. Recall that for the sake of argument I accepted the theoretical rationale for a minimum wage in general. I just questioned the rationale for a single, national minimum wage.

For the sake of simplicity, let’s assume a min wage of $10 an hour. If you are a min wage worker in New York City, working for 30 hours a week, that means you are taking in $15,600 a year. According to this cost of living calculator, the economically equivalent pay in Atlanta, Georgia is $6,360, which, at the same 30 hours/week work rate equates to an hourly rate of $4.07. So a minimum wage of $10 in NYC is the economic equivalent of a minimum wage of $4.07 in Atlanta. This means that if a company that employs 100 people in New York at $10 an hour decides to move to Atlanta and employs 100 people at $4.07 an hour, they are not “racing to the bottom”. They are providing exactly the same benefit in real economic terms, but just to different people. Indeed, if the company offered, say, $6 an hour to its Atlanta employees, it would be providing a greater economic benefit to its employees in Atlanta than to its employees in NYC. Again, far from a “race to the bottom”, such a situation is actually a “race higher”, yet the existence of a federal minimum wage actually eliminates the incentive for a company to do just that. And by artificially discouraging employer movement from high cost of living environments to low cost of living environments, the min wage actually favors those who live in higher cost of living environments at the expense of those who live in low cost of living environments.

Again, I cannot imagine any sensible justification for such a policy.

LikeLike

If the federal minimum wage law is pegged to the lowest cost of living state then it doesn’t change the nature of state minimum wage laws being the controlling factor.

On the other hand if it is pegged to the CPI of San Francisco it would be pretty onerous in Laredo.

LikeLike

Mark:

If the federal minimum wage law is pegged to the lowest cost of living state then it doesn’t change the nature of state minimum wage laws being the controlling factor.

Such a system would still put the low cost state at a disadvantage relative to the high cost state, as it would still force the low cost state to provide higher real wages to its workers than the high cost state would be forced to provide to its workers.

Having a single, national, minimum wage that ignores relative local economics can’t be justified.

LikeLike

If you were correct about which state is disadvantaged, jobs would be flowing to CA from TX, right now.

Perhaps you meant to write something else.

LikeLike

Mark:

If you were correct about which state is disadvantaged, jobs would be flowing to CA from TX, right now.

Incorrect, for a couple of reasons. The first is that California actually has a minimum wage that is higher than the federal minimum wage, while Texas does not. Which means that California is willingly giving up the advantage that the fed min wage gives to it. In fact, I believe California just recently raised its min wage to $10/hr, so while the TX min wage is just 72% of CA mins wage, according to the COL calculator I linked earlier, the COL in, say, Austin is 81% of what it is in Sacramento. So the prevailing min wage in Texas vs that in California gives Austin a clear advantage over Sacramento.

A second reason your conclusion is incorrect is that min wage laws are not the only factor that determines the relative attractiveness of a given labor market. There are lots of reasons outside of min wage laws, including other regulations relating to a given business, that might drive a company to prefer Texas to California. So even if Texas had a higher min wage relative to cost of living than California (which, again, it does not), it still could be the case that a business might prefer Texas because of other factors unrelated to min wage laws. Any single factor, like the min wage, will just effect things at the margin.

I understand the ideological attraction of imposing a flat min wage on the whole nation. But really I can see no sensible economic justification for it at all. Because of widely varying economic realities across various parts of the nation, a single federal min wage will, by its nature, create artificial advantages and disadvantages for different parts of the nation.

LikeLike

The first is that California actually has a minimum wage that is higher than the federal minimum wage,

EXACTLY MY POINT, DAMMIT.

LikeLike

Mark:

EXACTLY MY POINT, DAMMIT.

Your original point, I thought, was that if the national min wage was pegged to the lowest cost of living state, then state min wage laws would still be the controlling factor. But that is true only for high cost states that choose to have a min wage higher than the national one, a la CA. If two states both choose to mirror the national min wage, then the higher cost state has a clear advantage over the lower cost state. And that advantage is entirely in control of the higher cost state, because the only option the lower cost state has to offset it is lower its min wage to the real wage equivalent of the high cost state min wage, and the very presence of the federal min wage disallows it from doing so. The high cost state could, like CA, choose to give up that advantage, but that choice rests with them, not the low cost state. Hence my point…the national min wage advantages high cost states over low cost states.

LikeLike

Mark:

To take a slightly different angle on the same point, if one’s desire is to set a wage at which a minimum standard of living is achievable, then one must peg that wage to the cost of living in the area in which it is to be paid. If you peg it to just the lowest cost of living area out of all the areas under question, then you are not achieving your desire. You force one area, the lowest COL area, to provide a certain minimum standard of living, while allowing all the rest to provide something less than that. That clearly is a disadvantage to the lowest cost area.

Again, from a political/ideological point of view I can see the attraction of a single national min wage, but from an economic, results point of view, it makes no sense to me at all.

LikeLike

Scott, are they proposing “a single national minimum wage” or “raising the federal minimum wage”? You are positing a non-event, I think. What I describe is what we have now and what we will have so long as the federal minwage is based on the low cost area, not the median, not the high. As in the past, a small minwage increase has no effect measurable or measured. A big minwage increase would have multiple effects, most of which would be insufferably bad. I don’t know the break point but I suspect it to be any significant increment above prevailing entry wages or above the cost of automating the function. Minwages are still below prevailing entry wages most places.

Because I am opposed to artificially raising the minwage above the prevailing entry wage in the lowest cost area [I spent a lifetime representing small biz, so call me a dinosaur] I don’t care about this issue until it hurts the client pool with which I identify.

LikeLike

Let me add that we pay babysitters $10/hr or much more in Austin, the $10 is for HS kids. So $10 works here as a rough number for minwage. It would be less in Laredo.

LikeLike

Mark:

Let me add that we pay babysitters $10/hr or much more in Austin, the $10 is for HS kids. So $10 works here as a rough number for minwage.

I don’t know why a babysitter’s wages should be considered a reasonable gauge for what a min wage should be. There are all kinds of reasons why I can imagine being willing to pay a babysitter more than what I’d be willing to pay for a typical min wage job, supply and demand being just one.

LikeLike

Mark:

Scott, are they proposing “a single national minimum wage” or “raising the federal minimum wage”?

We already have a single national minimum wage. That is how the federal minimum wage works, as far as I understand. It is a single wage (currently $7.25/hr) that applies to the whole nation. And Obama is proposing that it be raised. I propose that it makes no sense to have one at all, even if one believes that a min wage is otherwise justified in theory. I think that, since economic conditions and cost of living vary greatly across the country, so too must any min wage, if it is to allow each labor market to compete on an equal footing with regard to wages.

What I describe is what we have now and what we will have so long as the federal minwage is based on the low cost area, not the median, not the high.

Is the federal min wage pegged to the lowest cost area in the country? I don’t know either way, but regardless, my criticism still stands. It makes no sense to have a single federal min wage, or a single national min wage (which is the same thing), even if it is pegged to the lowest cost area. For precisely the reasons I have already laid out.

As in the past, a small minwage increase has no effect measurable or measured.

I would imagine that the effect of any min wage increase, and even whether that increase could be considered small or large, would be largely dependent on local economic conditions, which, again, vary greatly across the nation. Relative to the cost of living, a $3 increase in the min wage in, say, Athens, GA is a much bigger increase than a $3 increase in NYC.

Minwages are still below prevailing entry wages most places.

Then it seems to me there isn’t much point to them in the first place.

I don’t care about this issue until it hurts the client pool with which I identify.

As with lots of issues, I care about this even though I don’t have a direct, vested interest in it.

LikeLike

re: MW, based on what I paid to have my dishwasher repaired yesterday, I’m in the wrong line of work.

LikeLike

Blue states have high labor costs, red states don’t. The left is simply trying to protect its turf…

LikeLike

Funny minimum wage article.

“I have always argued that we should pay them,” Elk said when contacted by the Free Beacon‘s Alana Goodman, to whom Elk previously said, “I hope you fucking burn in hell. … Go fuck yourself.” ”It wasn’t fair when I had to work as an Unpaid [sic] intern at campaign for Americas future [sic, sic] and it’s not fair that interns working on my stuff aren’t getting paid either.”

http://freebeacon.com/blog/mike-elk-company-man/

That’s different you inbred wingnut!

LikeLike

http://www.washingtonpost.com/blogs/capital-weather-gang/wp/2013/12/05/legitimate-chances-for-snow-and-ice-in-d-c-region-sunday-and-sunday-night/?wpisrc=nl_buzz

If you are unfamiliar with snow in the DC area, it’s time to being hoarding. for eventual profiteering.

LikeLike

If you are unfamiliar with snow in the DC area

I can hardly wait! Of course, I don’t have to get out and get to work. . .

LikeLike