Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1764.5 | 8.0 | 0.46% |

| Eurostoxx Index | 3056.8 | 20.9 | 0.69% |

| Oil (WTI) | 93.94 | 0.6 | 0.61% |

| LIBOR | 0.239 | 0.001 | 0.40% |

| US Dollar Index (DXY) | 80.54 | -0.169 | -0.21% |

| 10 Year Govt Bond Yield | 2.65% | -0.02% | |

| Current Coupon Ginnie Mae TBA | 106 | 0.1 | |

| Current Coupon Fannie Mae TBA | 105 | 0.2 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.23 |

Markets are higher this morning on strength in overseas markets. Market darling Tesla Motors (TSLA) fell in premarket trading after missing its quarter. Abercrumble (ANF) was down 9% after missing as well. Bonds and MBS are up small. At 10:00 we will get the Index of Leading Economic Indicators, which shouldn’t be a market mover

Tomorrow starts the big data, with GDP and then the jobs report on Friday. The bond market has clearly been spooked by the strong ISM numbers and the language out of the FOMC statement.

In politics last night, Chris Christie cruised to a win in New Jersey, while McAuliffe won in Virginia. Dinkins got another term in New York City.

Mortgage applications fell by 7% last week as mortgage rates rose 5 basis points. The purchase index fell by 5.2% while the refi index fell by 7.9%.

Homeprices are 17% overvalued according to Fitch’s models, with much of coastal California > 20% overvalued. Their model is based on unemployment, income, rental prices, population levels, housing units, and mortgage rates. Note that the median house price to median income ratio is back above its historical range again. This is based on NAR’s median house price, which is probably over-emphasizing the red-hot California markets due to its repeat sale methodology. All real estate is local, and I doubt we are overvalued all that much outside of a few markets like Washington DC, Manhattan, and the hot West Coast markets. In the judicial states (primarily in the Northeast) we have yet to see any sort of meaningful rebound in prices.

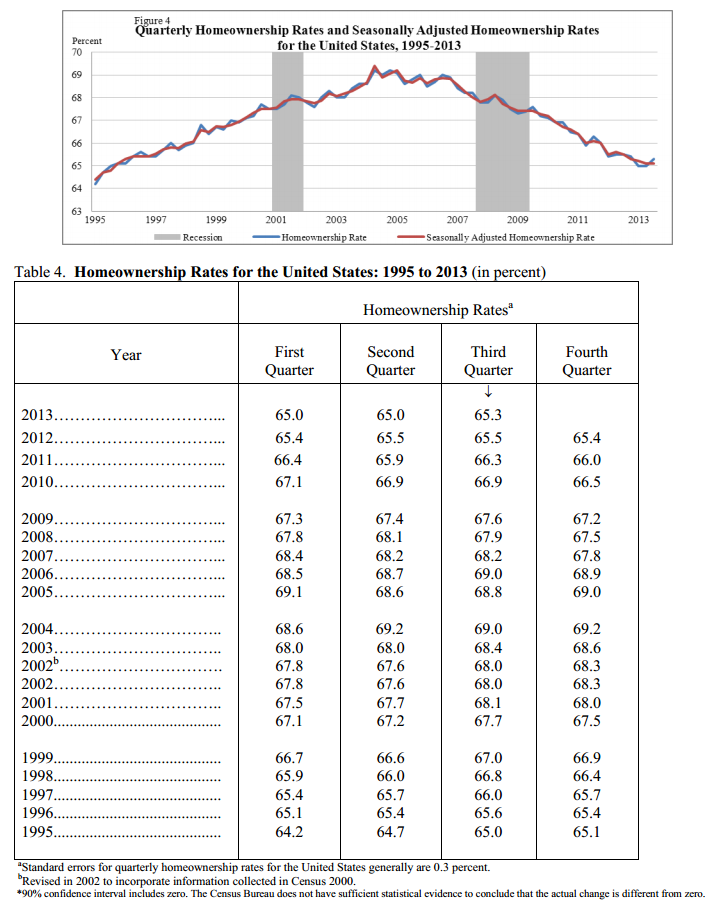

The homeownership rate edged up last quarter to 65.3% from 65% in Q2 and is now back to levels we haven’t seen since the mid-90s, when HUD began to aggressively push to increase homeownership in this country.

Interesting article on the fiscal drag (aka “austerity”) by the AEI. Without the Fed’s stimulus, nominal GDP would have fallen by 2%. Note that most of the drag is coming from the tax increases, not the spending cuts, as the tax hikes have a much higher multiplier than spending cuts. They cite a San Francisco Fed study which found that 90% of the fiscal drag came from increased taxes. This is not surprising as taxes were increased much more than spending was cut, but I found the difference in multiplier interesting. The spending cuts have a .60 multiplier while tax hikes have a 1.8 multiplier. This means that a $1 reduction in government spending reduces GDP by 60 cents, while a $1 increase in taxes reduces GDP by $1.80.

Filed under: Morning Report | 55 Comments »