Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1492.9 | -4.2 | -0.28% |

| Eurostoxx Index | 2736.0 | -8.5 | -0.31% |

| Oil (WTI) | 96.55 | 0.1 | 0.11% |

| LIBOR | 0.301 | -0.001 | -0.33% |

| US Dollar Index (DXY) | 79.8 | 0.023 | 0.03% |

| 10 Year Govt Bond Yield | 1.96% | -0.01% | |

| RPX Composite Real Estate Index | 193.4 | 0.8 |

Stock index futures are weaker as the Fed kicks off its January FOMC meeting. The markets will be parsing the press release looking for clues regarding the end of QE, specifically the timing and the economic variables that influence the decision. Today is a very heavy earnings day, with Danaher, Ford, EMC, International Paper, and Pfizer reporting. Bonds and MBS are up a tick or two.

The S&P Case-Schiller index of home values rose 5.5% YOY and .6% MOM in the month of November. The hardest hit areas (Phoenix, Detroit, Las Vegas) showed the biggest YOY increases (Phoenix was up 23%!), while the New York declined 1.2%

DR Horton reported a 39% increase in revenues and a 26% jump in homes closed from a year ago. Orders were up 39% and backlog was up 62%. Like the other homebuilders, DHI is reporting general strength in their housing markets. There was a shift towards larger houses as well, as the dollar increase in the value of homes built increased 60%, while the number of units increased 39%. They are looking forward to the spring selling season with optimism. The stock is up about 4% pre-open.

Is the “risk on” trade we have been waiting for since 2007 finally on? Trim Tabs is reporting that last month was a record month for inflows for stock mutual funds and ETFs – the last time we had inflows of this magnitude was the winter of 2000, right as the tech bubble was bursting. Time to be cautious or time to break out the champagne? Reason for optimism: There are no, repeat no, signs of overheating in the economy. If anything there is a tremendous amount of pent-up demand. That is not recessionary, and should therefore be bullish for stocks. Reason for pessimism: Interest rates are going up. The great secular bull market in bonds that began with Paul Volcker’s tightening in 1981 is ending. The end of QE will mean long-term rates will rise, and short-term rates will soon follow. Also, we are in a secular bear market for stocks, and those rare animals typically last a lot longer than 12 years.

This secular bear market in stocks resembles the bear market of the 1970s. with stocks trading in a large range that oscillates over a period of years, while going nowhere. To put the 1970s in perspective, the Dow Jones Industrial Average was at roughly the same place when I graduated from high school as it was when I was born.

Chart: Dow Jones Industrial Average 1965 – 1983:

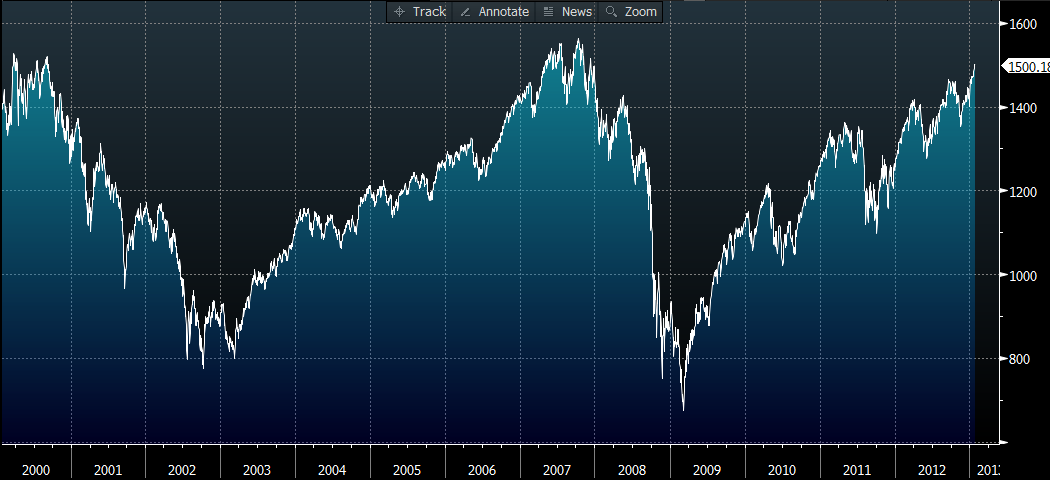

Compare to the S&P 500 since 2000:

Similar oscillating pattern, with higher highs, and lower lows. If you believe in charts, they suggest a further run to eclipse the previous high and then a swoon lower. So, you might have another 8% – 10% left before the market heads back down again.

Of course we have one other secular bear market to look at: the granddaddy of them all:

23 years of a secular bear – it took until 1953 to recover the losses from the 1929 crash. Some stock market darlings – Radio Corporation of America (aka RCA) never regained its peak from the 1920s. The economic backdrop of deleveraging has a lot more in common with the Depression bear than the 1970s bear which was driven by commodity price shocks and inflation.

Of course as Wall Street loves to say, past performance is not indicative of future performance, and charts are just that – representations of history that may or may not be relevant. The market may not follow either pattern. But, remember the great secular bull market in stocks from 1983 – 2000 was accompanied by a secular bull market in bonds that began at roughly the same time. That will not be the case this time around.

Filed under: Morning Report | 72 Comments »