Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1471.6 | 6.0 | 0.41% |

| Eurostoxx Index | 2710.7 | 8.2 | 0.30% |

| Oil (WTI) | 94.8 | 0.6 | 0.59% |

| LIBOR | 0.302 | -0.001 | -0.33% |

| US Dollar Index (DXY) | 79.61 | -0.198 | -0.25% |

| 10 Year Govt Bond Yield | 1.87% | 0.05% | |

| RPX Composite Real Estate Index | 191.7 | 0.3 |

Markets are higher after a good housing starts number and lower than expected unemployment claims. Bank of America and Citi both reported lower than expected 4Q earnings. Bonds and MBS are down.

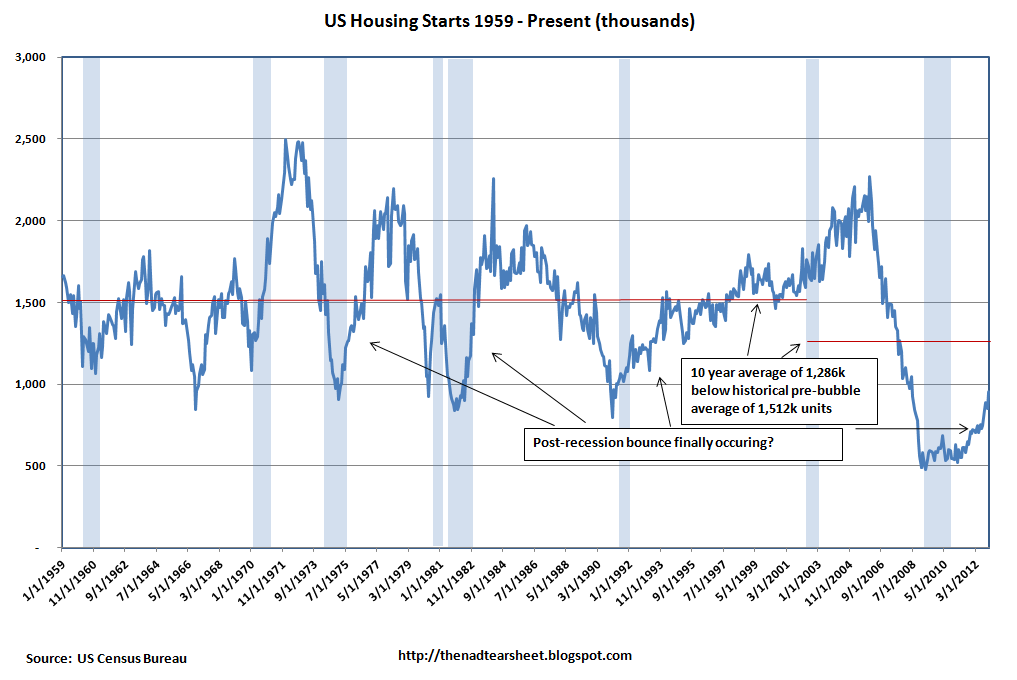

Housing starts took a big jump upward in December, to an annualized pace of 954k, an annualized increase of over 100k. This is the highest level since June 2008. Multi-family starts accounted for about a third of the increase. Building Permits increased at a 1.8% MOM and 29% YOY. Remember, we have historically started 1.5 million units per year, and our 954k annual number basically represents the low points of all recessions since 1957 up to the post-bubble recession.

Chart: Housing Starts

The CFPB is releasing new rules for servicers today. It essentially eliminates the practice of “dual tracking” where a servicer works to mod a loan and simultaneously initiates foreclosure proceedings in case the mod doesn’t work out or the borrower fails to pay. That might have the unintended consequence of less mods and more foreclosures. Foreclosures cannot be initiated until the account is more than 120 days delinquent. This rule pre-empts state law, so timelines will get extended in non-judicial states. Servicers with less than 5,000 loans will be exempt.

Speaking of unintended consequences, the Fed is now worried about bubbles in farmland and junk bonds, the direct result of QE. Unwinding QE (it needs a name – Fed Exit – Fexit?) will be a touchy deal. The buzzword for Fexit will be “convexity risk” Think Orange County in 1994 on steroids. Not only will MBS bids fade because of interest rate volatility, they will also have to contend with the Fed dumping paper in an effort to shrink its balance sheet. A 2014 recession is a distinct possibility.

What it took to get a mortgage in 2012, according to Ellie Mae: 748 FICO, 23/34 DTI, 21% down. Average interest rate 3.9%, average time to close, 48 days, 62% were refis.

Filed under: Morning Report |

An interesting piece about manufacturing and unions:

LikeLike

Technology is kiling unions as much as globalization and right-to-work states. Maybe more.

LikeLike

It seems that most of the union workers now are in the public sector, which is probably more resistant to technological advances (teaching, etc.).

LikeLike

last week, when they county picked up the trash a 3 man crew was on the truck.

this week, it was a driver who controlled a robotic arm that lifted the can and emptied into the truck.

LikeLike

Speaking of Orange County, the guy who blew it up (Robert Citron) just died.

LikeLike

Good piece by Nate Silver today:

“January 16, 2013, 1:06 pm

What Is Driving Growth in Government Spending?

By NATE SILVER”

…

Nevertheless, the declining level of trust in government since the 1970s is a fairly close mirror for the growth in spending on social insurance as a share of the gross domestic product and of overall government expenditures. We may have gone from conceiving of government as an entity that builds roads, dams and airports, provides shared services like schooling, policing and national parks, and wages wars, into the world’s largest insurance broker.

Most of us don’t much care for our insurance broker.”

http://fivethirtyeight.blogs.nytimes.com/2013/01/16/what-is-driving-growth-in-government-spending/

LikeLike

Thanks for that link, jnc. It’s a pretty stark look at how entitlement spending is taking up more and more of the budget. Beyond increasing health care costs, I worry about when interest rates are going to go up and the negative effect that will have on the levels of discretionary spending.

LikeLike

The real question is whether the benefits of Bernanke’s decisions will outweigh the costs. Not only will interest rates continue to stay low, but assets with values in fixed dollar terms, such as a bond or a bank account, will be worth less and less as the coming inflation starts to become more apparent. Investments with values that increase over time, such as stocks, commodities or real estate, will be the way to maintain and grow one’s wealth. In effect, the Fed will make your stuff worth more and your dollars worth less.

LikeLike