Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1351.2 | 0.5 | 0.04% |

| Eurostoxx Index | 2220.9 | 13.5 | 0.61% |

| Oil (WTI) | 80.75 | -0.7 | -0.86% |

| LIBOR | 0.468 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 81.6 | 0.012 | 0.01% |

| 10 Year Govt Bond Yield | 1.65% | -0.01% | |

| RPX Composite Real Estate Index | 180.7 | 0.2 |

Markets are flattish after a mixed Spanish bond auction and disappointing jobless claims numbers. Spain auctioned off 2.2 billion euros of 5 year debt, with a bid / cover ratio of 3:1, however it paid 6.07%. Sovereign yields across Europe are lower, as are Treasuries with the 10 year down a basis point. MBS are up slightly.

Yesterday, the Fed maintained low interest rates and committed to extend Operation Twist through the end of the year. Notably, the Fed took down its projections for GDP growth and bumped up its estimates for unemployment. Here is a “marked up” version of the statement, showing the changes from the April release. Note that the Fed took down its numbers in spite of a massive rally in the 10-year and mortgages courtesy of Europe.

Initial Jobless Claims came int at 387k, down from a revised 389k the prior week and more or less in line with expectations. Philly Fed was a disappointment as the Business Outlook Survey indicated weaker business conditions in its area. Rounding out the day’s economic data, May existing home sales came in at a 4.55 million annual rate, a drop of 1.5% MOM.

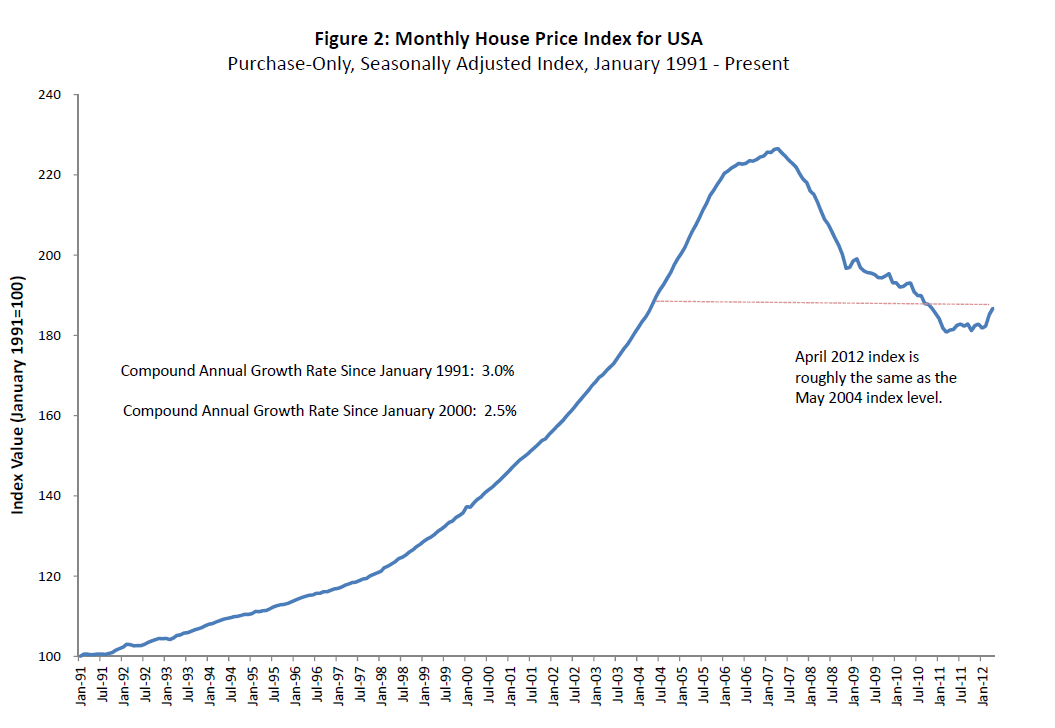

The FHFA House Price index was up .8% in April, while March was revised downward from + 1.8% to +1.6%. The FHFA House Price Index only considers Fannie and Freddie loans, so it acts as somewhat of a “center tendency” of the market, ignoring the high price and low price extremes. It certainly appears like the trend has shifted. See chart below:

Software Provider Ellie Mae released its May Origination Insight Report which provides data on mortgages originated though its Encompass system. The typical closed loan had a FICO of 744, a LTV of 81, and a DTI score of 24/35. A typical denied application had a FICO of 702, a LTV of 88, and a DTI of 28/43. The mix of refis vs purchase dropped to 54/46 from 56/44 in April and 61/39 in March, which is surprising given the drop in mortgage rates over the past 3 months. Closing times continue to increase, with the time to close up to 46 days from 42 in March. Overall, it shows a tight mortgage market with great rates for those who qualify.

On opposite ends of the economic spectrum, Octomom is getting foreclosed upon, while Larry Ellison is buying a Hawaiian Island.

Filed under: Morning Report | 111 Comments »