Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1325.5 | 10.0 | 0.76% |

| Eurostoxx Index | 2161.6 | 23.9 | 1.12% |

| Oil (WTI) | 86.19 | 1.2 | 1.38% |

| LIBOR | 0.468 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 82.02 | -0.306 | -0.37% |

| 10 Year Govt Bond Yield | 1.66% | 0.00% | |

| RPX Composite Real Estate Index | 178.3 | 0.2 |

Markets are higher this morning after China cut interest rates to boost their economy. The benchmark lending rate will drop from 6.56% to 6.31%, effective tomorrow (such precision!). The allowed discount from the benchmark was widened from 10% to 20%. Initial Jobless Claims in the US came in at 377k, more or less in line with expectations. Bonds and MBS are flat.

Given last Friday’s dismal jobs report, the market was definitely concerned about the Fed’s Beige Book survey which was released yesterday afternoon. Overall, the tone of the report did not confirm fears of an imminent slowdown. The Fed reported that “overall economic activity expanded at a moderate pace” and that “Economic outlooks remain positive, but contacts were slightly more guarded in their optimism.”

In another positive datapoint for the real estate industry, homebuilder Hovnanian reported better than expected earnings yesterday, with a 50% increase in backlog and a 52% increase in contracts. Perhaps this portends the rise in housing starts and construction we have been waiting for since 2008.

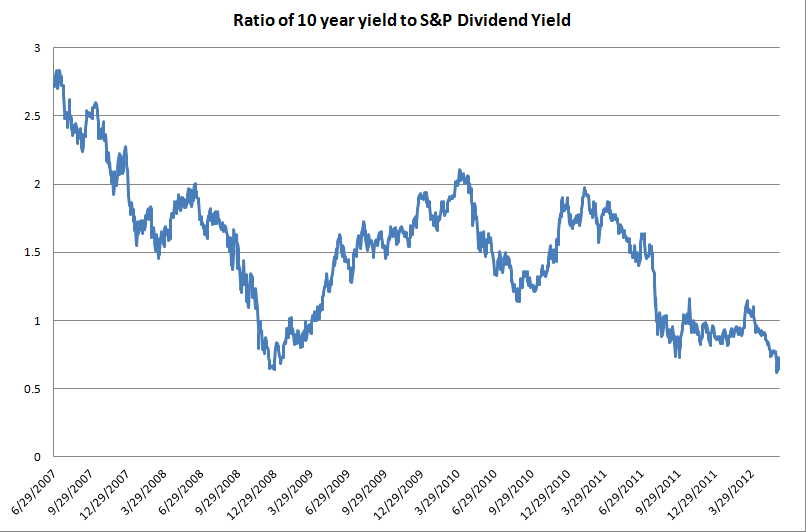

To get an idea how cheap stocks are compared to bonds right now, consider the fact that the 10 year yields about 1.65%, while the dividend yield on the S&P 500 is 2.2%. A dividend yield (let alone earnings yield) higher than the 10-year is a rare event. If you look at the ratio of the 10 year to the dividend yield, it reached just over 60% last week, and the last couple times it reached that level (2008 and fall of 2011), it portended a huge stock market rally. At any rate, it seems to trigger asset allocation decisions and may account for some of the velocity of the moves in the S&P futures and the bond futures. It also means buy stocks and sell bonds. Or borrow money long term.

Chart: Ratio of the 10-year bond yield to the S&P 500 dividend yield:

Filed under: Morning Report |

Headlines just coming through: Merkel says Germany ready to back “Euro-area instruments”.

update: Headline is misleading. Turns out she said “existing” Euro-area instruments.

LikeLike

Has Sep gone front-month yet?

LikeLike

Brent:

Has Sep gone front-month yet?

Not until the 18th. June expires the 20th.

LikeLike

No, Sep will go front-month at least a week before expiry. I think it might happen tomorrow, but I wasn’t sure if it happened earlier this week.

LikeLike

Brent…which product are you referring to?

LikeLike

S&P futures. Are bond futures on a different expiration schedule (3rd Friday in Dec, Mar, June, and Sep) than equity futures?

LikeLike

I’ve been monomaniacally focused on the short end, and so was thinking of libor contracts, which expire on the 3rd Wednesday, and this month that comes after the 3rd Friday. Bond futures are also third Wednesday. But volume in the Jun bond is already well below the Sep, so Sep is trading as the front contract.

LikeLike

i never knew LIBOR contracts expired on the 3rd Wed. You learn something new every day..

LikeLike

Is a LIBOR contract an option on what the future LIBOR will be? If so, that is like betting the over – under. What purpose does it serve?

LikeLike

Mark:

Is a LIBOR contract an option on what the future LIBOR will be? If so, that is like betting the over – under. What purpose does it serve?

It is not an option, but it does behave precisely like an over-under bet. The contract price implies a libor rate (100 minus the price) for the expiration date. When the contract expires, it will settle at the contract price implied by the libor setting for that date (100 – libor rate). As the buyer or seller of the contract, you will either pay or receive the difference between the settled price and the purchase price.

What purpose does this serve? It allows interest rate risk to be managed. To give you just one example, imagine you are a bank and one of your customers asks for a 2 yr fixed rate loan. You fund yourself in the short term market via 3m libor. If you lend him the money for a fixed rate for 2 years starting today, you will have funding exposure to rate movements in each quarter for the next two years, because what you receive on the asset is fixed, but where you are borrowing to fund it will change every 3 months. You can manage this mismatch by buying 2yrs worth of libor contracts, which essentially fixes in 8 quarters of libor settings. Now it doesn’t matter to you whether libor rates move up or down. Even though you fund in the short term, the libor contracts allow you to fix in longer term funding rates by fixing in future libor settings.

[edit – BTW, there are options on libor contracts, called eurodollar options, or EDO’s. But the eurodollar contracts themselves are not options.]

LikeLike

OK, Scott, thanks. I may have more ???

LikeLike

mark:

I may have more ???

Ask away. Hopefully I have answers.

LikeLike

At the risk of interrupting the LIBOR contract expiration discussion, I’ll note that the now bipartisan Senate investigation of the Obama administration’s selective national security leaking may prove interesting in the months ahead:

“Probing Obama’s secrecy games

Will high-level Obama officials who leak for political gain be punished on equal terms with actual whistleblowers?

By Glenn Greenwald

Thursday, Jun 7, 2012 06:05 AM EDT”

http://www.salon.com/2012/06/07/probing_obamas_secrecy_games/singleton/

“Stuxnet, a worm infecting the Obama campaign

By Ed Rogers

Posted at 07:39 AM ET, 06/07/2012”

http://www.washingtonpost.com/blogs/the-insiders/post/stuxnet-a-worm-infecting-the-obama-campaign/2012/06/07/gJQAomTpKV_blog.html

LikeLike

I find myself in agreement with Paul Krugman on this being an appropriate beginning to all stories about the government:

““During a recent panel on the numerous failures of American journalism, I proposed that almost all stories about government should begin: ‘Look out! They’re about to smack you around again!’” – Molly Ivins”

http://krugman.blogs.nytimes.com/2012/06/07/good-golly-miss-molly-2/

http://www.texasobserver.org/mollyaward

LikeLike

Scott:

How accurate would say that they are as a forcasting mechanism for the economy, any correlation?

LikeLike

banned:

How accurate would say that they are as a forcasting mechanism for the economy, any correlation?

I wouldn’t say that they are a good forecasting mechanism. They are more of a measure of expectations. For example, when the Fed announced a while back that their zero rate policy was good until at least 2013, you could see the futures contracts out to 2013 rally in a big way, flattening the curve. And as different economic news comes out suggesting, say recovery, you can see those contracts sell off in the expectation that the fed will change their policy.

The other thing to note is that, ultimately, forward rates (which is what libor contracts are) are actually implied by current rates. For example, if I know what the 2yr treasury yield is, and I know what the 3yr treasury yield is, then I can calculate what the implied 1yr treasury yield, 2 yrs forward is. This is not a prediction of what the 1yr yield will be in 2yrs. It is a calculation of what the 1yr yield starting in 2yrs that I can achieve today is.

Does that make sense?

LikeLike

yes and thanks.

In other news, Ben spoke and the beautiful dream is over. back to the slog

LikeLike

I opposed the Paycheck Fairness Act as unnecessary. Hell, it would even ultimately prove counterproductive for women, but my concern is, admittedly, for employers.

Rand Paul opposed it as “communist”.

http://www.economist.com/blogs/democracyinamerica/2012/06/paycheck-fairness-act?scode=3d26b0b17065c2cf29c06c010184c684

Rand Paul, in this case, proves himself a fool.

I can explain why it was a bad statute, if anyone cares.

LikeLike

I care.

LikeLike

Good morning, Scott.

It would have changed the Equal Pay Act in three ways.

1] Previously, management could prove that plaintiff female was paid less, or a male was paid more, for a reason other than gender. An example from my practice: I proved the superficially similarly situated male had just been given a big raise to keep him from being stolen by a competitor.

If the bill had passed, the new standard would have been:

(B) The bona fide factor defense described in subparagraph (A)(iv) shall apply only if the employer demonstrates that such factor (i) is not based upon or derived from a sex-based differential in compensation; (ii) is job-related with respect to the position in question; and (iii) is consistent with business necessity.

An inventive plaintiff’s attorney (and inventiveness is endemic) would have said, in my case situation, that the reason the male was offered more was because of the historical bias in the industry in favor of males, and would have provided an expert and a computer analysis. The burden of proving my client’s decision to meet that offer was not derived from a sex based differential would have been on my client and me!

2] Such defense shall not apply where the employee demonstrates that an alternative employment practice exists that would serve the same business purpose without producing such differential and that the employer has refused to adopt such alternative practice.

To me, #2 leaves a lot open to the imagination of plaintiffs’ attorneys. For example, not from my practice, but from the literature, a plaintiff’s attorney might suggest modeling on civil service classifications or union CBAs, if it suited his client’s purpose, and first demand that the employer adopt same, only filing suit when [my client] “refused to adopt such alternative practice.”

3] “…additional compensatory and/or punitive damages”

A game changer. The threat of a trial where the damages awarded could be unrelated in a meaningful way to the alleged harm would force many more nuisance value settlements on loser cases. In Austin, the defense retainer in Fed Ct. is $15K, minimum, for an obviously defensible case that can be won on summary judgment, because there will be one full round of preliminary discovery before the court will entertain the Motion. So a loser case is worth $14k, and the risk it will survive SJ is magnified by the potential for open ended damages. Pile loser cases on a small biz and it is in CH 11. If the employer’s insurance covers these claims the carrier will usually pay and raise rates, or pay and cancel.

WRT the minority of employers who still have significant pay differentials between men and women, usually for seniority reasons, which under the proposed statute would be castigated as the result of a history of discrimination:

the result over time would not be to raise compensation for all but to LOWER it, as employers’ lawyers would advise their clients: “never pay any man more than what the highest paid woman in a similar position is paid”, assuming that the employer was previously paying similarly situated males more. For that employer, women could further lose one current threshold competitive advantage for them in hiring.

In the union labor context, CBAs would be suspect if heavily based on seniority in some fields. For example, CWA used to represent female telephone operators and male linemen. Now there are many female linemen, but still not many male operators. The seniority rules would have to take into account at what point more seniority doesn’t make a better employee, or there would be a sex based differential against female linemen and against male operators. Under one version of this bill, the union could be a co-defendant with the employer and the employer could not use the CBA as a shield. I don’t know if that provision survived to the death of the entire bill, but I think you get the drift.

The Equal Pay Act is good law. It prohibits discrimination against women. It allows bona fide distinctions, not based on gender, to be drawn. I have seen it work, both as a prophylactic against bad practices and a remedy in court. But it was not a laydown for plaintiffs that made the workplace a lottery. And as I have described, I think that would have been the result of this proposed statute.

LikeLike

Mark:

Thanks. I tried to read thru the actual law, but gave up. Couldn’t make any sense of it, so your explanation is useful.

LikeLike

This was Obama in a press conference on Friday:

“The private sector is doing fine. Where we’re seeing weaknesses in our economy have to do with state and local government.”

How utterly clueless is this guy?

LikeLike

Well, he did pull it back shortly after in the same PC. Better than defending the position.

LikeLike

mark:

Better than defending the position.

True enough. But I think it is indicative of an instinct/ideology that views government as the primary driver of the economy. The idea that weakness in the economy even could be, much less is, caused by not enough government spending by states and localities is quite troubling.

LikeLike

The idea that weakness in the economy even could be, much less is, caused by not enough government spending by states and localities is quite troubling.

I disagree with you because of the absolutist view embodied in your statement. Failure of states and localities to spend on schools, hospitals, roads, bridges, tunnels, fire and police protection, will, at some point, redound to the economic disadvantage of that state or locality, IMHO. I think it is no accidental correlation that MN schools, etc., are way better than MS schools, etc., and so is the economy of MN.

I do not have the expertise to draw the lines and I do not know when more is better or when less is better, but I reject the absolutism that suggests weakness in the economy could not be related to state or local government failure of spending.

Scott – you might read this: http://www.texastribune.org/texas-environmental-news/water-supply/texas-water-woes-spark-interest-desalination/

and this: http://www.texastribune.org/texas-environmental-news/water-supply/raw-water-production-facility/

These are local gummint projects, or public-private partnerships, in some instances, without which TX will run dry.

LikeLike

Mark:

Failure of states and localities to spend on schools, hospitals, roads, bridges, tunnels, fire and police protection, will, at some point, redound to the economic disadvantage of that state or locality, IMHO.

I agree that a functioning government that provides certain services (we probably disagree on which services exactly) is important to economic development, so, yes, to the extent that government expenditures are required in order to provide those services, it follows that (certain) government expenditure matter. But what it matters to is the private sector economy. To say that the economy is weak is, necessarily, to say that the private sector is not doing well. It may make sense to say, for example, that private sector business is down, but if we build a bridge across the river, tourism will produce greater economic activity and create jobs. But it would never make sense to say hey, private business is doing fine, so unemployment must be the result of the absence of government bridge-building projects.

As an aside, with regard to your specific example, education, I wonder a) whether the correlation you mention actually does exist across the nation, and b) whether causation can be/has been established. For instance, assuming the existence of a correlation between local economic performance and government expenditures on education, I imagine it is at least as likely that the former produces the latter as it is that the latter produces the former.

LikeLike