Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1340.2 | -9.8 | -0.73% |

| Eurostoxx Index | 2199.2 | -55.4 | -2.46% |

| Oil (WTI) | 94.47 | -1.7 | -1.73% |

| LIBOR | 0.466 | -0.001 | -0.21% |

| US Dollar Index (DXY) | 80.51 | 0.248 | 0.31% |

| 10 Year Govt Bond Yield | 1.78% | -0.05% | |

| RPX Composite Real Estate Index | 175.3 | 0.0 |

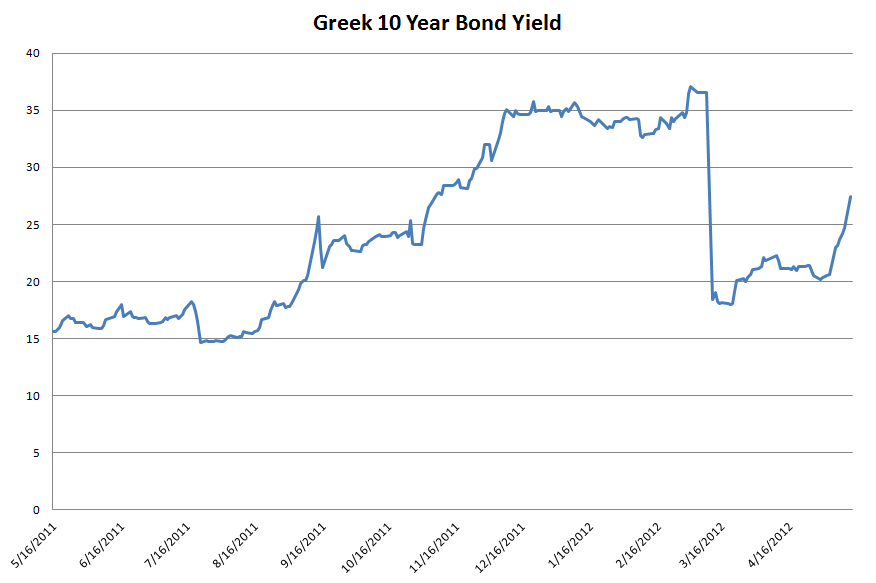

A sloppy start to the week as sovereign spreads widen in Europe. Greek sovereign debt is now trading at a 27.4% yield, which is the same level as last Nov. Don’t forget, this is the post-reorg debt – for those keeping score at home, Greek sovereigns were at 15% last year at this time, rose to over 40%, did a restructuring two months ago which pushed yields down to 17%, and now they are 27%. Spanish yields are rising, and it is time to start paying attention to the credit default swaps on the big European banks – Dexia is considered one of the worst cases, and is trading at the 17.75% level.

All of the stress in Europe is pushing down Treasury yields which sit about 10 basis points above September’s lows. MBS are higher as well, with the Fannie and Ginnie 3.5s up 6 ticks. This is putting pressure on oil and the Euro. The S&P futures are suggesting that the 200 day moving average is going to get broken on the open.

It is official – Ally’s Residential Capital has filed for bankruptcy protection. This move separates the auto loan and banking business, and should pave the way for the government to divest its 74% stake. Ally is providing the $150MM DIP and is kicking in $750MM.

It looks like 3 executives from JP Morgan will walk the plank over the $2 billion “hedging” loss in their Chief Investment Office unit. Jamie Dimon is not resigning, at least not yet. It is surprising that JP Morgan disclosed the loss before it fully exited the position – if disclosure rules forced his hand, that is a big unintended consequence. This episode will undoubtedly elicit calls for more regulation, and strengthens the view in Washington that there is no alpha in banking, just beta.

Chart: Greek 10 year bond yield:

Filed under: Morning Report |

“It looks like 3 executives from JP Morgan will walk the plank over the $2 billion “hedging” loss in their Chief Investment Office unit. Jamie Dimon is not resigning, at least not yet. It is surprising that JP Morgan disclosed the loss before it fully exited the position – if disclosure rules forced his hand, that is a big unintended consequence. This episode will undoubtedly elicit calls for more regulation, and strengthens the view in Washington that there is no alpha in banking, just beta.”

It also seems to be strengthening the view that the purpose of regulation is to ensure that banks never loose money. Apparently everyone is entitled to a stock market that always goes up.

“The fact that JPMorgan’s loss — which Mr. Dimon has warned could “easily get worse” — is not enough to topple the bank, is not the point. What matters is that JPMorgan, like the nation’s other big banks, is still engaged in activities that can provoke catastrophic losses. If policy makers do not strengthen reform, then luck is the only thing preventing another meltdown.”

see also:

The purposes of regulation should be to ensure that bank losses are borne by bank stakeholders (i.e. stockholders and bondholders) and not transferred (“socialized”) to some other party. The goal shouldn’t be to end the ability of banks to loose (or make) money, but rather to end a system of “Too Big to Fail” where losses are not borne by the same parties who share the profits.

Edit: looks like I’m subconsciously channeling the WSJ editorial page:

“That mistakes can happen even in a bank run by a capable CEO is not news. But J.P. Morgan and the other financial giants are still playing with taxpayer money in the form of both explicit and implicit guarantees, which makes this episode a reminder of the need to make investors, not taxpayers, pay for such mistakes. It also illuminates the failure of Washington’s well-advertised efforts to fulfill this need.”

http://online.wsj.com/article/SB10001424052702304371504577402331446053716.html?mod=WSJ_Opinion_LEADTop

LikeLike

jnc:

Just wanted to make sure you saw my answer to your question on Friday. I posted it late Friday night, so thought you may have missed it.

LikeLike

“A sloppy start to the week as sovereign spreads widen in Europe. Greek sovereign debt is now trading at a 27.4% yield, which is the same level as last Nov. Don’t forget, this is the post-reorg debt ”

Banned – Krugman seems to be agreeing with me, for whatever that’s worth. (mostly it disturbs me).

“May 13, 2012, 1:11 pm

Eurodämmerung

Some of us have been talking it over, and here’s what we think the end game looks like:

1. Greek euro exit, very possibly next month.

2. Huge withdrawals from Spanish and Italian banks, as depositors try to move their money to Germany.

3a. Maybe, just possibly, de facto controls, with banks forbidden to transfer deposits out of country and limits on cash withdrawals.

3b. Alternatively, or maybe in tandem, huge draws on ECB credit to keep the banks from collapsing.

4a. Germany has a choice. Accept huge indirect public claims on Italy and Spain, plus a drastic revision of strategy — basically, to give Spain in particular any hope you need both guarantees on its debt to hold borrowing costs down and a higher eurozone inflation target to make relative price adjustment possible; or:

4b. End of the euro.

And we’re talking about months, not years, for this to play out.”

http://krugman.blogs.nytimes.com/2012/05/13/eurodammerung-2/

“May 14, 2012, 8:41 am

Euro Reversibility

A brief blast from the past. What I hadn’t realized when I wrote that two years ago was the extent to which eurozone banks could float through a slow-motion bank run by borrowing from the ECB. So the real moment of truth comes if and when the ECB — or more accurately the Bundesbank, which may ultimately be on the hook — decides to pull the plug.

The point, of course, is that this moment may not be far off.”

http://krugman.blogs.nytimes.com/2012/05/14/euro-reversibility/

LikeLike

” Krugman seems to be agreeing with me, for whatever that’s worth. (mostly it disturbs me).”

Does it make you review your thinking?

LikeLike

“bsimon1970, on May 14, 2012 at 8:41 am said:

” Krugman seems to be agreeing with me, for whatever that’s worth. (mostly it disturbs me).”

Does it make you review your thinking?”

That was more of a joke. I do believe that he frames the choices of 4a. and 4b. properly.

Edit: Like Banned, I draw a distinction between Krugman the pure economist and Krugman the liberal/progressive polemicist. His analysis of the Eurozone is more of the former. His arguments on technical flaws inherent in the creation of the Eurozone have merit. His arguments on why I should pay more taxes to fulfill his view of what constitutes social justice, not so much.

LikeLike

Matt Taibbi on the JPMorgan Chase news:

http://www.rollingstone.com/politics/blogs/taibblog/jamies-cryin-dimon-j-p-morgan-chase-lose-2-billion-20120511

LikeLike

“ScottC, on May 14, 2012 at 9:00 am said:

jnc:

Just wanted to make sure you saw my answer to your question on Friday. I posted it late Friday night, so thought you may have missed it.”

I did. Thanks for the detailed response. So your bottom line recommendation is a sliding scale of FDIC insurance premiums tied to the perceived risk of the activities that the banks chose to engage in?

Edit: I’d also note that this description of the discount window, while accurate is incomplete:

“The discount window acts simply as a short term lender of last resort in order to provide liquidity during illiquid times.”

It’s also an implicit subsidy for those banks vis-a-vis other financial institutions that (theoretically) don’t have access to the discount window.

LikeLike

jnc:

So your bottom line recommendation is a sliding scale of FDIC insurance premiums tied to the perceived risk of the activities that the banks chose to engage in?

Basically, yes. If you are going to sell insurance, you need to tie the premium to the risks being underwritten.

It’s also an implicit subsidy for those banks vis-a-vis other financial institutions that (theoretically) don’t have access to the discount window.

But other financial institutions are not required to hold reserves at the Fed. How do you see this subsidy manifesting itself in ordinary, daily business?

LikeLike

I don’t have anything to add to either the hamburgers or the morning report but I did see this headline at Yahoo and though it was funny. I have no interest in the trial however.

John Edwards Defense Relies on Definition of ‘The’

That sounds really boring compared to the definition of “sex”.

LikeLike

“ScottC, on May 14, 2012 at 10:08 am said:

It’s also an implicit subsidy for those banks vis-a-vis other financial institutions that (theoretically) don’t have access to the discount window.

But other financial institutions are not required to hold reserves at the Fed. How do you see this subsidy manifesting itself in ordinary, daily business?”

Having access to a line of credit that others do not have access to allows them to take on greater risk as it acts as an emergency cushion. This is true even if it’s collateralized.

The analogy I would draw would be to having access to a home equity line of credit versus not having one allows the person with access, even if they don’t use it, to structure their own personal finances in a way that can pursue higher returns from personal investing in illiquid assets without having to worry about a cash crunch should the roof need a repair.

LikeLike

jnc:

Having access to a line of credit that others do not have access to allows them to take on greater risk as it acts as an emergency cushion. This is true even if it’s collateralized.

But this is balanced by the reserve and capital requirements, which restricts the amount of risk they can take relative to other institutions. To use your home equity line of credit analogy, it would be like the bank offering that line of credit, but only if you keep a minimum balance in your savings account. Also, to make the analogy more apt, the home equity line of credit would be an overnight line of credit, and your home would have to be a lot more liquid than it actually is, since the bank would need to be in a position to easily liquidate your home overnight should it decide you were not going to make good on the loan. And you’d also have to pay an above market interest rate. (My guess is that banks have lost more money on home equity lines of credit than the fed has lost on discount window lending.) It’s just not clear to me that access to the discount window provides a clear advantage in the way that, say, FDIC does.

BTW, you may be interested to know that, according to the Fed web site:

“In unusual and exigent circumstances, the Board of Governors may authorize a Reserve Bank to provide emergency credit to individuals, partnerships, and corporations that are not depository institutions. Such lending may occur only when, in the judgment of the Reserve Bank, credit is not available from other sources and failure to provide credit would adversely affect the economy.”

LikeLike

Good and reasonably balanced piece on Romney and Bain for those who haven’t seen it.

“The Romney Economy

At Bain Capital, Romney remade one American business after another, overhauling management and directing vast sums of money to the top of the labor pyramid. The results made him a fortune. They also changed the world we live in.

By Benjamin Wallace-Wells

Published Oct 23, 2011”

http://nymag.com/news/politics/mitt-romney-2011-10/

LikeLike

” Good and reasonably balanced piece on Romney and Bain for those who haven’t seen it.”

Thanks. There’s a lot to digest. One question I’m left with… what skills does the presidency require & does WMR have them?

LikeLike

bsimon:

One question I’m left with… what skills does the presidency require & does WMR have them?

What skills does BO have that WMR doesn’t have?

LikeLike

“ScottC, on May 14, 2012 at 7:10 pm said:

bsimon:

One question I’m left with… what skills does the presidency require & does WMR have them?

What skills does BO have that WMR doesn’t have?”

I thought this passage could apply equally to both:

“Romney never worked from any particular “macro theme,” any philosophy of how the economy was moving. What he employed instead was an exhausting habit of playing devil’s advocate, proposing sequential objections to a particular project or idea, until eventually, through a kind of Darwinian process, consensus was reached. “I never viewed Mitt as very decisive,” says one of his Bain Capital colleagues. “The idea was that if there’s enough argument around an issue by bright people, ultimately the data will prevail.” ”

http://nymag.com/news/politics/mitt-romney-2011-10/index2.html

LikeLike

That was an interesting piece jnc, thanks.

Here, too, private equity seemed to provide an early warning of broader changes. In three years during the early nineties, the Princeton economist Henry Farber has found, roughly 10 percent of American white-collar male managers lost their jobs. For the first time, according to data collected through the General Social Survey, white-collar workers were nearly as worried about losing their jobs as blue-collar workers. Those white-collar workers who kept their jobs worked harder, and the compensation that had once been spread through the broader middle ranks of corporations now collected at the top. In 1980, a CEO had earned about 35 times the wages of an average worker; by 1990, it was about 80; and by 2000, it was about 300. The portion of America’s gross national product that ended up in the hands of workers declined by more than 10 percent between 1979 and 1996; the portion that went to investors rose by a similar amount. “What you end up with is a choice between a bigger cake less equally split and a smaller cake equally split,” says Bloom, the Stanford economist. “But that’s a social question.”

This is really fascinating to me. My father was a VP of a large manufacturing company in the mid west, although he started with the company here in CA. It wasn’t a publicly traded company. The last ten years or so he worked, before retiring in 1987, he was a numbers guy and did a lot of forecasting but also became involved in some motivational speaking to address the concerns at the lower ends of the totem pole. He was very successful traveling around the country selling the bottom up sales and customer service scenarios at the dealer level. It’s literally the opposite of what these financial giants and venture capitalists seem to be doing, at least according to my understanding of the piece. Of course, as a staunch conservative I always thought his motivational speaking was out of character, but apparently it really worked and turned the company around to a certain extent along with customer and dealer satisfaction.

LikeLike

I wonder how much simple things like the PC, databases, and Excel has eliminated the need for middle managers.

LikeLike

Brent, they mention that in the piece. I agree it’s an issue. One of the things that’s interesting to me right now is something my daughter recently learned. If you want something done right, do it yourself (I wanted to tell her). She’ll be going into middle management in the oil industry soon and all those programs are essential to her work, and she needs to do them herself as she’s the one who understands the concept. She said last time she was here she ought to be getting a Master’s in Illustrator, Excel, GIS, modeling and all the rest as they are essential to her work. Just a thought.

LikeLike

I liked the framing of the piece that yesterday’s reforms set up the problems for tomorrow, specifically the use of stock options/grants to align management and shareholder incentives and how that can devolve to a myopic approach to managing the quarterly earnings statements to boost the stock price at the expense of long range planning.

This was also worth noting from the paragraph following the one you quoted lmsinca:

“There is no doubt that the tools of this efficiency movement helped to build the economy of the nineties, and this fact makes Bloom’s social question somewhat more complicated. That booming decade, with unemployment declining by 3.5 percent and real GDP growing by nearly 4 percent each year during the Clinton administration, depended heavily on a spike in productivity, which itself had hinged on the wide deployment of computer technology to displace more expensive forms of labor. Economists believe there was a clear connection between the labor-market changes in the early nineties and the great profits that soon followed. “Could we have had the productivity boom without displacement? My answer would be no,” says Frank Levy, an MIT economist.”

Everything has a price and involves tradeoffs.

LikeLike

jnc

how that can devolve to a myopic approach to managing the quarterly earnings statements to boost the stock price at the expense of long range planning.

It seems as though the incentives are all wrong. My dad only received a yearly bonus based upon his success in increasing sales and keeping production in line with orders as he forecast them. He won when the dealers won or his numbers weren’t way out of whack.

Incentive wise it really reminds me of the revolving door between the Fed and private firms, including the SEC, talk about unintended consequences. I tend to think it’s all a little crazy.

LikeLike

See y’all later. I”m bushed as we worked straight through the weekend. Manana………

LikeLike

jnc:

A late thank you for that piece from me too. That was a long, but good, read.

LikeLike

jnc4p writes

“I thought this passage could apply equally to both:

“Romney never worked from any particular “macro theme,” any philosophy of how the economy was moving. What he employed instead was an exhausting habit of playing devil’s advocate, proposing sequential objections to a particular project or idea, until eventually, through a kind of Darwinian process, consensus was reached. “I never viewed Mitt as very decisive,” says one of his Bain Capital colleagues. “The idea was that if there’s enough argument around an issue by bright people, ultimately the data will prevail.” ””

I’ve had that thought as well. Both have a reputation for being pragmatic realists.

LikeLike

This may just be political speculation, there’s a lot of that going around right now, and it’s way too early to tell but………………..

Will the women’s vote finally determine the outcome of the presidential election? Since women first got the vote, with the 19th Amendment in 1920, presidential politics has awaited this climactic moment.

Until now, election statistics have never proved that the 19th Amendment altered the outcome of any presidential race. In 2008, Barack Obama handily won the female vote. But given margins of statistical error in exit polls, the men’s choice is not determinable. In both 1992 and 1996, a similar pattern emerged in Bill Clinton’s victories.

This could be one reason for this fierce fight over women’s issues — far more than the typical Republican vs. Democratic battle of the sexes. It has an unusually angry edge.

A recent Washington Post poll hints at a possible answer. On the surface, the poll seems a replay of 2008 — giving Obama roughly the same percentage margin over Mitt Romney as candidate Obama won against Sen. John McCain. But there’s a big difference: Romney has a 4-point lead among men. Indeed, POLITICO’s battleground poll of key swing states gives Romney a statistically significant 7-point lead among men.

Experts are predicting a closer election than in 2008. But with the developing gender dynamic, it should not surprise anyone if, come Labor Day, the polls show men solidly favoring Romney with women lined up strongly behind Obama.

So this “battle of the sexes” could then set up a potentially historic climax if the president wins reelection. It would be a significant milestone, symbolic of one of the vast changes occurring in national politics.

LikeLike

Has anyone heard from Mark lately? I’m used to some of us (myself included) disappearing for days/weeks on end but not him normally. I don’t like it when he’s not here, as his influence is my best hope for forcing myself to be more moderate.

LikeLike

Hi – I am just back from five days in L.A. and am behind both on my ATiM reading and my actual work.

Thanks for the kind word, Lulu.

I am going to try to absorb the discussion here of Dimon/Chase and banking as quickly as I can, and comment on burgers, and reveal to Scott what makes BHO far more qualified then WMR, IMO, even though I will not be voting for either of them. But that might still leave me behind the curve here so that I would have to skip all that and just try to stay up with y’all again. Mike and QB provided a rich look at the drug labeling/tort area, and Dave! gave me a bittersweet laugh with the Pentagon study of studies. JNCP kept up the quality of links but I have not yet pursued them. Lulu’s comment on upside down incentives hit a chord for me.

Just letting y’all know that I did try to catch up last night! And y’all can get along great when I am gone for five days, BTW.

LikeLike

I thought this was a good read as well. I know it’s too early to rely on polls but this piece has more than that. There are some really insightful comments from Veterans that I believe will be reflected in the election. I’m not sure that Obama’s Afghanistan policy appeases any of their concerns but it appears the Republican’s usual hawkish bluster isn’t impressing them either for the most part.

If the election were held today, Obama would win the veteran vote by as much as seven points over Romney, higher than his margin in the general population.

Michael Langston, a Baptist minister who served as commander of 110 military chaplains in Afghanistan, didn’t carry a weapon but often visited the front lines. “I would go to trauma centers where they worked on soldiers who were burned and disfigured,” he said. “We’d roll into villages where every man, woman and child had been massacred, and the Taliban had cut off heads and feet.”

Back in the U.S., Langston, 57, suffered nightmares and sweats. Always a mild-mannered man, he began yelling at his kids. When a vehicle backfired in a supermarket parking lot, “I hit the ground and rolled under a car.” He was diagnosed with PTSD.

Looking back, Langston, a graduate of the Naval War College, sees “a failed policy. When we leave, these places go back to the way they’ve done everything for thousands of years.”

LikeLike

I saw that article on the veterans too, lmsinca, and thought it was interesting. I think that is where the primary battle will hurt Romney. I have a hard time seeing him wanting to continue down a hawkish path, but it will be hard for him to walk back from some of what he has already said. It will be interesting to see what, if any, role foreign policy plays in the election. I think Romeny will be pretty successful in keeping the focus on the economy. If not, he definitely loses.

LikeLike

lms:

WaPo had a story on BHO and the veterans vote too.

“Republicans have long defined themselves in part on their hawkish stance on national security issues and their popularity among the military and veterans. But the makeup of the nation’s armed forces is changing, and Obama hopes to win over veterans by appealing to the same subgroups that propelled him to victory in 2008: women, minorities and young people.”

LikeLike

Hi Mark, glad you’re back and I was being dead serious. How was our weather compared to Austin?

Ash, I think it’s going to be interesting but I’m not sure Obama will be able to walk the tightrope either. I personally didn’t really care for his speech from Kabul. Delay, delay, delay, IMO. But we’ll see.

Mike, thanks for the link.

LikeLike

lmsinca, that’s a fair criticism of Obama. I do think he has two things going for him on that front though. First, he can point to successes (killing Osama) as a reason for shifting to quicker withdrawal or a less hawkish stance even if he’s been a wishy washy before the compaign. Second, he’s almost definitely going to be less hawkish than Romney. It doesn’t seem likely that Obama’s “delay, delay, delay” position will lead to liberals leaving his side.

LikeLike

ash

I’m sure most liberals will still vote Obama. Like you said though if the contest comes down primarily on the economy, I think Romney has a chance. A lot of what we’re hearing now is jockeying for position and trial balloons to see what has the most resonance with voters I think. As always, during an economic downturn, the economy generally trumps everything else.

LikeLike

I’m out to get some work done as I have tons of it, see y’all later.

LikeLike

“markinaustin, on May 15, 2012 at 6:50 am said:

…

JNCP kept up the quality of links but I have not yet pursued them.”

If you only read one, read the NY Mag piece on Romney and Bain Capital.

http://nymag.com/news/politics/mitt-romney-2011-10/

LikeLike

If you only read one, read the NY Mag piece on Romney and Bain Capital.

Done. Now back to work.

LikeLike

Lms & Mike, thanks for the links.

I’m wary of reading too much into national demographic breakouts. The media are coveting the race as a national one. What we need is more visibility into how those demographic groups are spread around the country.

For example, NPR was recently discussing the black vote & speculating on whether BHO’s pronouncement on gay marriage would influence support for him. But there was no attempt to contextualize this with the electoral college. If the black vote from Georgia to Mississippi is down, there is zero effect on the electoral college. But if the black vote in Detroit is down, they have big problems.

LikeLike

bsimon:

The media are coveting the race as a national one. What we need is more visibility into how those demographic groups are spread around the country.

Yesterday James Taranto made a similar point with regard to Obama’s evolution on same sex marriage and its effect on the so-called black vote:

LikeLike