Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1325.5 | 10.0 | 0.76% |

| Eurostoxx Index | 2161.6 | 23.9 | 1.12% |

| Oil (WTI) | 86.19 | 1.2 | 1.38% |

| LIBOR | 0.468 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 82.02 | -0.306 | -0.37% |

| 10 Year Govt Bond Yield | 1.66% | 0.00% | |

| RPX Composite Real Estate Index | 178.3 | 0.2 |

Markets are higher this morning after China cut interest rates to boost their economy. The benchmark lending rate will drop from 6.56% to 6.31%, effective tomorrow (such precision!). The allowed discount from the benchmark was widened from 10% to 20%. Initial Jobless Claims in the US came in at 377k, more or less in line with expectations. Bonds and MBS are flat.

Given last Friday’s dismal jobs report, the market was definitely concerned about the Fed’s Beige Book survey which was released yesterday afternoon. Overall, the tone of the report did not confirm fears of an imminent slowdown. The Fed reported that “overall economic activity expanded at a moderate pace” and that “Economic outlooks remain positive, but contacts were slightly more guarded in their optimism.”

In another positive datapoint for the real estate industry, homebuilder Hovnanian reported better than expected earnings yesterday, with a 50% increase in backlog and a 52% increase in contracts. Perhaps this portends the rise in housing starts and construction we have been waiting for since 2008.

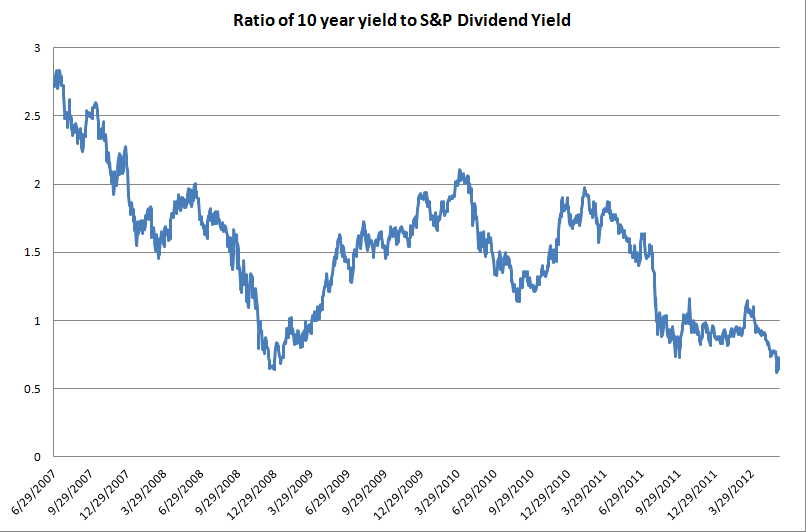

To get an idea how cheap stocks are compared to bonds right now, consider the fact that the 10 year yields about 1.65%, while the dividend yield on the S&P 500 is 2.2%. A dividend yield (let alone earnings yield) higher than the 10-year is a rare event. If you look at the ratio of the 10 year to the dividend yield, it reached just over 60% last week, and the last couple times it reached that level (2008 and fall of 2011), it portended a huge stock market rally. At any rate, it seems to trigger asset allocation decisions and may account for some of the velocity of the moves in the S&P futures and the bond futures. It also means buy stocks and sell bonds. Or borrow money long term.

Chart: Ratio of the 10-year bond yield to the S&P 500 dividend yield:

Filed under: Morning Report | 26 Comments »