Markets are down small on no real news. Bonds and MBS are up.

This week promises to be relatively quiet with the New Year’s holiday in the middle of the week. There might be some volatility in bonds as dealers square up their positions for year’s end.

Greece is back in the news, as political wrangling risks the rescue package they have from the ECB. The 10 year Greek bond yield is up 130 basis points this morning, to 9.8%. At the margin, this will help keep a bid under Treasuries.

Home Prices are up 4.5% year-over-year, according to Black Knight Financial Services, which puts prices about 10% off of their peak levels in June 2006. We will get Case-Shiller tomorrow.

Will 2015 herald the return of the first time homebuyer? It is looking like it might happen, as lending loosens up, the job market improves, and supply comes on line. Note the homebuilders like D.R. Horton and KB Home are rolling out more starter homes.

Holiday spending was strong, according to data released by MasterCard. They saw spending up 5.5%, while the National Retail Federation saw sales up 4.1%. Online sales rose 14%. Pent-up demand is beginning to be satisfied. Low gasoline prices are a big help.

It being Boxing Day in the UK and a Friday for the rest of the world, there is no European markets open and no Asian markets to follow our own. So the US is pretty much dead today, despite being officially open. I posted this mainly to avoid having to despoil the Merry Christmas post with a link to Matthew Yglesias.

Markets are higher as decent data comes in. Bonds and MBS are down small. Almost all of this week’s data is being released today. Today is a full day, Wed will be a half day, and Friday will be a full day (so far).

Third quarter GDP was revised upward to to +5% from +3.9%. Personal Consumption was revised upward from 2.2% to 3.2%. Inflation remained unchanged at +1.4%.

Durable Goods orders on the other hand came in weaker than expected, down .7%, after the Street was expecting +3%.

New Home Sales fell to 438k from 458k last month. This is the seasonal slow period, so I wouldn’t read too much into it.

Personal Income rose .4% in November, while Personal Spending rose .5%. The PCE deflator (the preferred inflation measure for the Fed) was down .2% on a month-over-month basis and up 1.2% on a year-over year basis.

The University of Michigan Consumer Sentiment Index ticked down to 93.6 in December. The Richmond Fed Manufacturing Index rose to 7 from 4.

The FHFA Home Price Index rose .6% in October after a flat September. On a year over year basis, home prices increased 4.5%. The index is roughly 5% lower than its April 2007 peak. Remember, this index only looks at homes with a conforming mortgage, so it is a narrower sample than Case-Shiller.

Ocwen stock got slammed yesterday as they announced a settlement with New York State and its founder stepped down. Ocwen will not be able to purchase any more MSRs without New York State approval. They also were fined $150 million. The stock got rocked for 27% yesterday, and is down 70% for the year.The stock is down another 3 bucks (19%) this morning.. This one may be a value trap, folks.

Rick Santelli from CNBC spells out the yield curve flattening scenarios. The yield curve has been flattening (the spread between long term rates and short term rates has been narrowing), and many traders continue to have “flattening” trades on. Essentially, this is what i was talking about yesterday with the Fed – the Fed could raise short term rates yet the 10 year (and mortgage rates) might not move all that much because of global demand for long-term sovereign debt. He also points out the big caveat to this: that ECB President Mario Draghi pursues a less aggressive policy than the market is already pricing in. This would put pressure on Euro sovereigns with microscopic yields (like the German Bund at 59 basis points), and could cause world sovereign bond markets to sell off in a co-ordinated fashion. Remember the economic backdrop in the US: A 5% GDP growth rate and a 2.2% 10 year bond yield are strange bedfellows. Note that a sell off in bonds might not guarantee a rally in the stock market either…

Finally, the MR will be on hiatus for the holidays. Wishing you and yours all the best.

This week is for all intents and purposes a two day week. Markets will close early on Christmas Eve and many will take off Friday.

The big deluge of data is tomorrow, with GDP, personal income, personal spending and a host of other indicators.

The risk-on trade continues this morning, with stocks up small and bonds down a tad. Oil continues to fall.

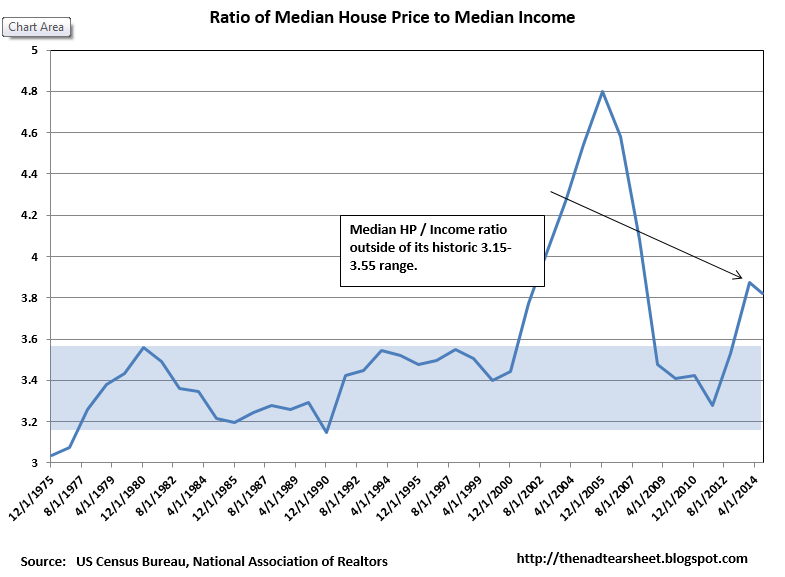

Existing Home Sales fell 6.1% to a seasonally adjusted annual rate of 4.93 million, according to NAR. Housing inventory was tight and bad weather didn’t help things either. The median existing home price was 205,300, which is 5% above November 2013. According to Sentier Research, the median income in the US was $53,700 as of the end of October. This makes the median home price to median income ratio just over 3.8, which is above its historical range of 3.15x – 3.55x. This means home price appreciation is probably going to be hard to come by until wage inflation begins to pick up.

One other thing to keep in mind: a flattening yield curve is a classic “tell” that the economy is slowing down, and by all accounts, it looks like the economy is accelerating. This will be another situation where the classic investing playbook isn’t going to help you all that much. In other words, if the Fed starts hiking rates and mortgage rates stay where they are, don’t all of a sudden dump your portfolio and pile into defensives like Proctor and Gamble or General Mills.

Markets are flattish this morning after a torrid 2 day run courtesy of Santa Yellen. Bonds and MBS are up small.

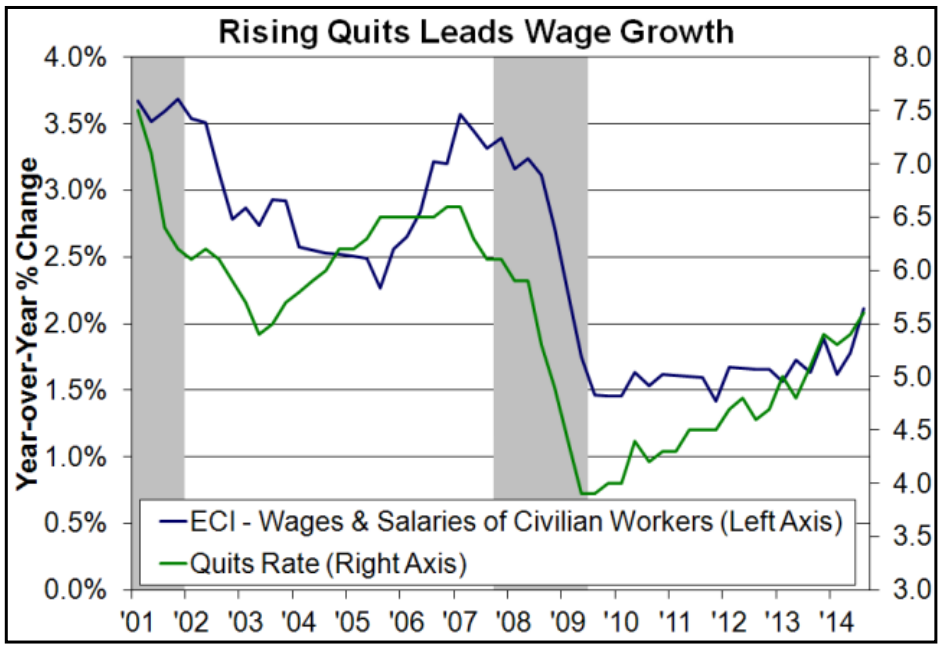

Fannie Mae is forecasting that wage growth is just around the corner and focuses on an interesting indicator out of the JOLTS job report – the quit rate. The quit rate is a leading indicator for job growth, and it has has been moving up for quite some time while wages have been flat. Another reason to be somewhat optimistic about 2015.

Are the high premiums for FHA loans creating an adverse-selection problem? The MBA thinks so. Creditworthy borrowers are going for the cheaper Fannie and Freddie loans, leaving only the borrowers with poor credit in the FHA risk pool. The new 3.5% down Fannie Mae loans will undoubtedly exacerbate this trend.

The drop in oil prices is causing pain in economies that rely on oil revenues, particularly Russia and Venezuela. It looks like Russian banks are going to need some sort of bailout. This could have impacts on the US real estate market, particularly at the high end. On one hand, Russian billionaires will want to move assets out of Russia ahead of the capital controls that are probably coming, On the other hand, in a crisis, you sell what you can, not necessarily what you want to. Not sure how this will shake out, but it bears watching. It will probably be a preview of what happens when China’s real estate bubble bursts as well. The Asian Crisis of the late 90s did have some reverberations in US credit markets, so we may feel a bit of credit tightening as banks back away from each other.

Stocks are continuing yesterday’s Fed-driven melt-up. Bonds and MBS are down hard. That window where rates were around 2.05% did not last long.

As advertised, the FOMC statement basically substituted “patience” for “a considerable time.” That said, it still contained the “considerable time” language, but referred to it in the past tense. Probably the biggest surprise was their downward forecast for 2015 inflation to a range of 1% – 1.6%. Their September forecast was 1.6% to 1.9%. They also took down their 2015 unemployment forecast to 5.25% from 5.5% in September. The Street seems comfortable that rates are going up in the second half of 2015.

Initial Jobless Claims fell to 289k last week, and we have been solidly below 300k for quite some time. The leading indicators have been strong for a while, however we have not been seeing the wage growth. That said, I am seeing anecdotal evidence that wage inflation might be be around the corner. At lunch I noticed the “help wanted” placard had taped over the starting salaries and increased them by a buck an hour. Sample size of 1, of course, but still…

The Markit US PMI came in weaker than expectations. The Bloomberg Consumer Comfort Index ticked up to 41.7 from 41.3 last week. The Philly Fed Index fell from 40.8 to 24.5 and the Index of Leading Economic Indicators was flat at .6%.

Mortgage lenders are worrying more about lackluster demand impacting margins, according to the latest Fannie Mae Lender Sentiment Survey. The biggest headache remains regulatory, of course. Lenders anticipate a modest housing expansion in 2015. It seems like the homebuilders agree. It is all going to hinge on the return of the first time homebuyer.

Markets are higher this morning on no real news. Bonds and MBS are down.

Oil continues to fall, with a barrel of West Texas Intermediate now down below $55 a barrel. This is putting pressure on prices. The Consumer Price Index fell .3% in November. Ex food and energy, it rose .1%. Will be interesting to see how the Fed addresses (if at all) falling energy prices in the FOMC statement.

Mortgage Applications fell 3.3% last week. Purchases were down 6.9% while refis were flat.

The FOMC will announce their decision at 2:00 pm. Expect volatility around that time and after as the press conference starts.

“A considerable time.” Sounds like a novel. Anyway, that is the phrase that will be the focus of the Fed statement. Will the Fed drop the language that states that rates will remain near zero for a “considerable time?” The new expected buzzword? Patience. Given how far bonds have moved to the upside already I don’t know how much a dovish statement will move them further. If anything the risks are on the downside.

Stocks are lower as oil continues to fall. Bonds and MBS are rallying hard.

Euro yields are continuing to move lower. The German Bund is currently trading at 57.6 basis points. It began the year at close to 2%. Think about that for a moment. FWIW, the trader in me is starting to think about a capitulation low in rates. Which means we are ripe for a snap-back in yields. LOs, I know this is a dead period of the year, but there might be some refis to be had with the us 10 year yield falling towards 2%. I don’t know how long this gift lasts.

Another observation is that we are getting close (40 basis points or so) to the lows set before the the Fed hinted that QE was ending. If we are getting this sort of movement in rates without QE, it does beg the question of whether QE was effective in the first place.

The Russian Ruble fell to a record low as the Russian Central Bank raised interest rates to 17%. The ruble has been slammed by a combination of low oil prices and international sanctions over Ukraine. The last stop is capital controls. The swoon in oil prices has hit Russia and Venezuela particularly hard.

Housing starts fell to 1028k in November from an upward revised 1045k. Building Permits fell from 1092k to 1035k. For once it was single fam that accounted for most of the decline – multi-fam actually rose. Note that weather may have affected the numbers as winter storms arrived early this year for the upper Midwest and New England.

The FOMC meeting begins today. The decision will be released tomorrow at 2:00 pm.

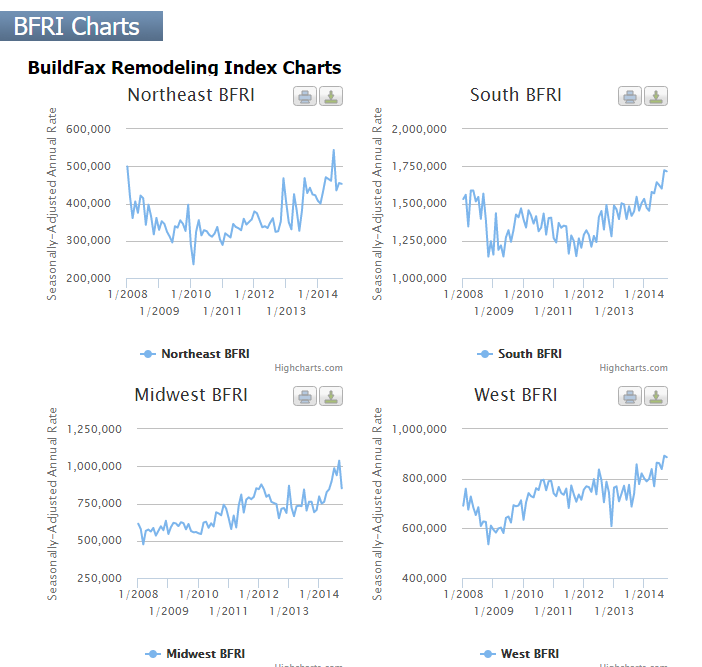

The Buildfax remodeling rate came in at just under 4 million, which is 4% below September and is 10% higher than a year ago. Activity continues to be strongest in the South and West, with the Midwest and Northeast lagging.

Markets are higher this morning after stocks got slammed in Asia last night. Bonds and MBS are down.

The NAHB Homebuilder Sentiment Index fell to 57 in December. Sentiment is still on the strong side, although the Street was clearly spooked by Toll’s numbers last week.

Wall Street is betting that inflation will remain dead for a long time. Treasury Strips are back (which basically slices and dices a long term Treasury into a bunch of zero coupon bullet bonds). This strategy has been a winner this year, rallying almost 50%. Foreign bond investors have had a great year with the the currency and bond markets posting big gains. The thing to remember is that US investors aren’t the only ones who play the Treasury market – and foreign bond investors are often looking at their domestic bond markets and finding more value in the US. To put this in perspective – the US 10 year yields 2.12%. The German Bund (10 year) yields 64 basis points. The Japanese JGB (another 10 year) yields under 38 basis points. The Spanish 10 year yields 1.79%. There is a global relative value trade happening here.

Strategists have gotten the bond market wrong all year. This is a case where the textbook response – sell Treasuries as the economy improves – has been dead wrong, overwhelmed by events overseas. Keep this in mind when thinking about rates in the US – strong data might not be enough to push bonds lower and originators might be getting a gift here. It won’t last, and the snap-back could be vicious. Second, anyone buying a 30 year zero at 43 which yields 2.86% should have their head examined. This is bubble behavior, and is the bond market equivalent of buying Cisco Systems at 70 (or 132x earnings) in 2000. Bonds will crack at some point, but keep in mind that bond market cycles are long.

Speaking of strong economic data, Industrial Production rose 1.3% in November and capacity utilization topped 80% for the first time since March of 2008. This production number was the highest since 2010. On the other side of the coin, the December Empire Manufacturing Index fell in December.

The FOMC meets this week, and the decision will be released Wednesday at 2:00 pm EST. This one should have a press conference, along with updated economic projections and a press conference. The focus is on the timing of rate hikes, and investors will key in on language regarding the labor market.

In the budget deal last week, some regulations were relaxed for the big Wall Street banks, particularly the provision requiring derivatives to be housed in an entity without recourse to the parent FDIC – insured bank. This sparked a big rebellion on the left, but it ended up going nowhere. FDIC insured banks may now use credit default swaps as hedging instruments for their own books. To hear the left tell the story, this basically returns us back to the bad old days of 2005. To the industry, this is a common-sense relaxation of a rule that went too far in the first place. That said, banks were always allowed to use these products, but had to post more collateral than they wanted to. This is a knotty question, as many “hedges” are really speculative bets when you delve into the details. I suspect JP Morgan’s 2012 London Whale trading loss was intended to act as a hedge in the first place.

Finally, there was a bit of dishing on this place in PL yesterday…