Stocks are bouncing back after yesterday’s sell-off. Bonds and MBS are down small.

Mortgage Applications fell 1.3% last week. Purchases were up 1.9% while refis fell 2.9%.

Attitudes about the US economy are finally turning around, according to the Fannie Mae National Housing Survey. More people think the economy is on the right track than the wrong track. Also interesting is that consumers sense that mortgages are becoming easier to get.

Inflation remains low, partly because the rally in the dollar is keeping a lid on import prices. Ever since the ECB began the march towards full QE, the dollar has been screaming. The dollar is approaching parity on the Euro – start thinking about that summer vacation in the South of France. Fun fact, when the euro was trading around 86 cents on the dollar, you could stay at the Ritz in Paris for roughly about the price of a good business hotel in Manhattan.

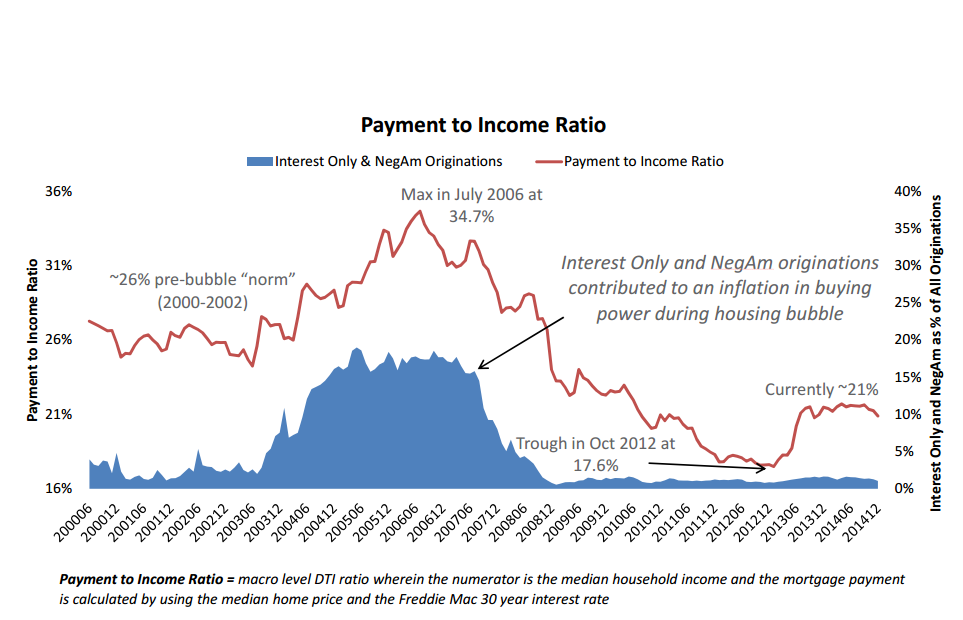

Housing affordability has decreased a bit since the trough of 2012, but still remains well above the pre-bubble years of 2000 – 2002, at least as measured by mortgage payment to income ratio. Pre-bubble, the DTI ratio for the median income and mortgage payment was about 26%. It rose to almost 35% during the bubble, fell to 17.6% in the trough, and is now around 21%. If you look at the chart below, you can see how much interest only and negative amortization loans factored into the bubble years. Pretty amazing to think that almost 1 in 5 mortgages was an IO / neg am during the go-go days of the bubble.

Interesting story about the mess that is Detroit. As downtown begins its gentrification / hipster renaissance, the rest of the city is struggling, and the biggest problem are these sales based on quitclaim deeds, which can leave the buyer with massive liabilities for back taxes.

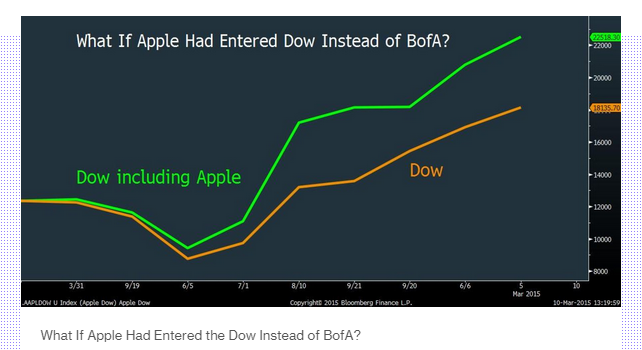

In February of 2008, Bank of America was added to the Dow Jones Industrial Average, just as the financial sector was beginning its swan dive. At that time, Apple was a $100 billion dollar company. What would have happened to the index if Apple was added instead of Bank of America?

Filed under: Morning Report | 32 Comments »