Posted on May 6, 2015 by Brent Nyitray

Stocks are higher this morning after yesterday’s bloodbath. Bonds and MBS are flat

The ADP Employment Change index is forecasting a weak employment report this Friday. They report shows 169,000 jobs were created in April, which was lower than the 200,000 estimate. The Street is forecasting an increase of 230,000 for Friday. This is the weakest report in over a year, and you can see the marked slowdown beginning this year. If the early weakness was just weather-related, then you should see some sort of rebound. You aren’t.

Some more disappointing data this morning – productivity fell 1.9% in the first quarter after falling 2.1% in the fourth quarter. Output fell .2% while compensation increased 6.2%. Unit Labor Costs rose 5%. Lower productivity has been driven by a combination of a stronger labor market and weak GDP growth, so it isn’t necessarily a bad thing, at least in the short term. It means that we could still see improvement in the labor market despite weak economic growth.

Mortgage Applications fell 4.6% last week as purchases rose .8% and refis fell 8.3%. Bonds got slammed last week, so that isn’t a surprise. The 30 year fixed rate mortgage rate rose to 3.93% from 3.85%. Refis as a percentage of loans fell to 52.5%.

Foreclosures fell to 2.22%, according to the MBA. Delinquencies fell to 5.54%.

As the rhetoric between Greek Prime Minister Alexis Tsipras and the EU gets more and more heated, the ECB is wrestling with how much of a haircut to demand on Greek collateral. The machinations between the Greeks and the EU are driving Euro yields, which are driving US yields. “The fundamentals have not changed, but bond markets have,” said Christoph Rieger, the Frankfurt-based head of fixed income strategy at Commerzbank AG. “The European bond markets are broken, hampered by low yields, high regulation and central bank intervention. Markets will have to get used to these erratic swings.” The European situation is why so many bond strategists got it so wrong in the US over the past year and explains why bonds are selling off in the US despite some weaker economic data.

Home Prices rose 5.9% annually, according to CoreLogic. A combination of tight inventory, low mortgage rates, and improving confidence is the culprit. Of course we need wage growth to make this actually sustainable, and it looks like we could be seeing the start of wage growth, at least according to the Employment Cost Index.

Filed under: Morning Report | 35 Comments »

Posted on May 5, 2015 by Brent Nyitray

Stocks are lower this morning on economic data. Bonds and MBS are getting slammed.

Bonds in the US have been buffeted by the volatility in the European bond markets as

optimism and pessimism over a bailout wax and wane. The German Bund is now trading at 51 basis points after hitting 7.5 bps about two weeks ago. The snapback has been vicious and caught a lot of people on the wrong side of the boat.

Chart: German 10 year bond yield:

The ISM Services Index rose to 57.8 in April from 56.5 in March. These are strong numbers, which should bode well for the jobs report on Friday.

Economic optimism fell, however from 51.3 to 49.7. While a lot of things figure into these sentiment statistics, they are very sensitive to gasoline prices.

Oil is back over $60 a barrel as the supply glut begins to dry up. This could bump up the inflation numbers a bit, which would be good news for the Fed, as long as it is stays muted and inflation holds around 2%. If it goes above, get ready for all the “The Fed is Behind The Curve” handwringing. That would be Hillary’s nightmare scenario.

Note David Einhorn

took aim at fracking (and specifically Pioneer Natural Resources) with regard to profitability at a value investing conference.

Filed under: Morning Report | 9 Comments »

Posted on May 4, 2015 by Brent Nyitray

Stocks are higher this morning after a stronger-than-expected European manufacturing report eased fears of deflation. Bonds and MBS are up small.

This week has some important economic data, with the biggest being the jobs report on Friday. The market has been backing away from the June rate hike forecast, and IMO the jobs report will have to be outstanding (300k+ payrolls, and a meaningful increase in wages) to bring a June tightening back into play. We will also get productivity and unit labor costs this week, which will figure heavily into the Fed’s thinking.

The ISM New York Index increased to 58.1 from 50 in March. Factory Orders rose 2.1%, topping the analyst 2% forecast.

A few stronger than expected economic reports turned around G7 debt in a hurry. The German Bund, which hit a record low of 7.5 basis points two weeks ago is now trading at a 41.5 basis point yield, which is a 3 month high. G7 sovereigns have been a one-way bet for a long time, so a sell-off is to be expected.

Bill Gross’s latest Investment Outlook is good. He is calling for the end of the secular bull market in bonds and is recommending shorting the Bund (good trade over the past two weeks). He also believes that cheap credit, which has fueled the bull market in stocks is going to slowly dry up. Is he suggesting to sell your portfolio and bury the cash in the back yard? Not at all. However he is arguing that the trade going forward may be focusing on lightly levered income trades instead of searching for capital gains.

Filed under: Morning Report | 9 Comments »

Posted on May 1, 2015 by markinaustin

About Labour, this: Mr Miliband is fond of comparing his progressivism to that of Teddy Roosevelt, America’s trustbusting president. But the comparison is false. Rather than using the state to boost competition, Mr Miliband wants a heavier state hand in markets—which betrays an ill-founded faith in the ingenuity and wisdom of government. Even a brief, limited intervention can cast a lasting pall over investment and enterprise—witness the 75% income-tax rate of France’s president, François Hollande. The danger is all the greater because a Labour government looks fated to depend on the SNP, which leans strongly to the left. http://tinyurl.com/nwqjron

Filed under: Elections, EU, UK | 1 Comment »

Posted on May 1, 2015 by Brent Nyitray

Stocks are higher this morning on no real news. Bonds and MBS are down. Most of Europe is closed for May Day.

Construction Spending fell .6% in March – another bad economic number. Residential Construction fell 1.6%, although we already knew that from the lousy housing starts number of 926k.

The ISM Manufacturing Survey was flat in April, coming in at 51.5. A reading of 51.5 would correspond to a GDP growth rate of about 2.6%. The comments suggest that conditions are good, and while the rise in the dollar is a headwind, it isn’t choking off growth. The West Coast port strike didn’t help either.

Consumer sentiment fell slightly in April, according to Reuters and the University of Michigan.

And of course, it probably means the end of the secular bear market in stocks that began in 2000.

The open question is whether the Fed can raise rates without crashing the markets.

Filed under: Morning Report | 18 Comments »

Posted on April 30, 2015 by Brent Nyitray

Stocks are lower this morning on no real news. Bonds and MBS are down as European bonds continue to sell off.

European bonds have been selling off as fast money gets caught on the wrong side of the boat. This is pushing up Treasury yields, which should be moving down based on some of the economic data lately.

There is a lot of economic data this morning. Initial Jobless Claims fell to 262,000, the lowest reading in 15 years. The ISM Milwaukee index fell to 48.08. The Bloomberg Consumer Comfort Index fell to 44.7 and the Chicago Purchasing Manager Index rose to 52.3.

The Employment Cost Index rose .7% in Q1. Wages and Salaries increased .7%, while benefits increased .6%. On an annualized basis, wages and salaries were up 2.6%, while benefits were up 2.7%. This is a big jump from the fourth quarter reading of 2.1%, and the average over the past few years of around 2%. One data point does not make a trend, but economically this is encouraging – wage growth has been a long time coming.

Personal Income was flat in March, however compensation was up .2%. Personal spending rose to 0.4%, and the savings rate dipped slightly to 5.3%. The savings rate has been trending upward however, as people use some of the added income to pay off debt. The increase in spending is an encouraging data point.

Inflation remains low, using the Fed’s preferred inflation measure, personal consumption expenditures. On a year-over-year basis, the core number is up 1.3%, well below their 2% target. Given the weak Q1 GDP number and the weak inflation numbers, I find it hard to imagine the Fed moving in June.

The FOMC statement was pretty bland, and we didn’t see much of a reaction. The slowdown was attributed largely to “transitory factors.” On rate hikes: “The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.” Given unemployment is back at normal levels, they are probably looking at wage growth as their key metric.

Household formation increased at an annual rate of 1.5 million in Q1, even as the homeownership rate dipped. This is good news for landlords, however it isn’t spilling over to residential construction yet, with housing starts still mired about 70% of normalcy.

Filed under: Morning Report | 10 Comments »

Posted on April 29, 2015 by Brent Nyitray

Markets are subject to some push-pull this morning with stronger data out of Europe and weaker data out of the US. Bonds and MBS are down.

Bonds are getting roughed up this morning after Germany reported inflation that was higher than expected. The German Bund is trading at 26.3 basis points, up 10 basis points this morning. This has pulled US Treasuries lower. Note the Fed rate decision is scheduled for 2:00 PM EST.

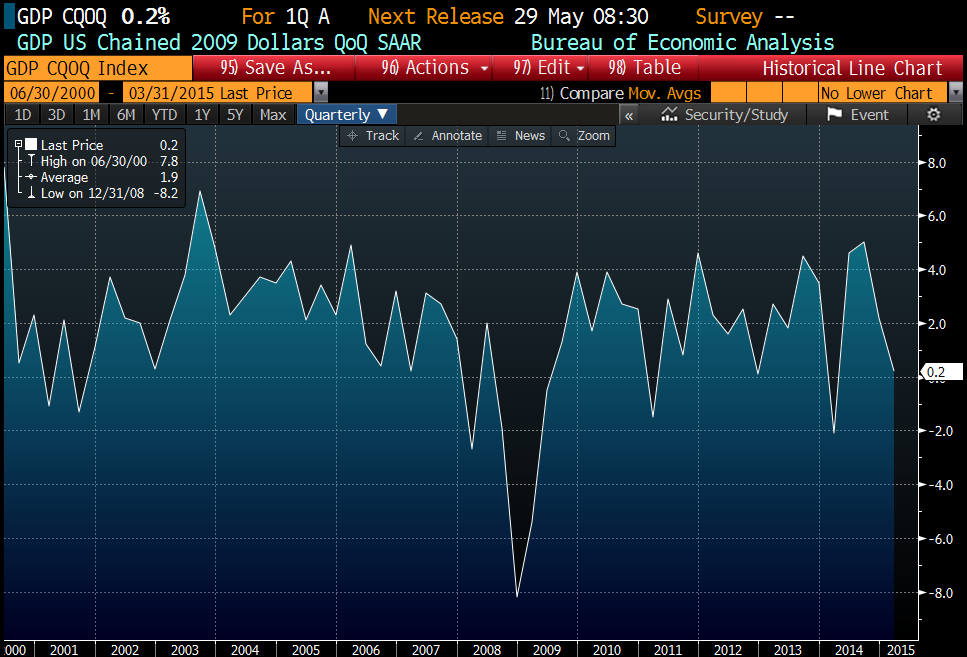

Stocks on the other hand are dealing with a huge miss on GDP. The advance estimate came in at +0.2% for the first quarter. The Street was already expecting weakness due to the weather, however the number still missed the +1.0% street estimate by a wide margin. Consumption growth fell to 1.9% from 4.4% in the fourth quarter. Investment fell from 3.7% to 2.0%. Government spending improved from -1.9% to -.7%, although that was driven by decreases in defense and increases in non-defense spending. Finally, the trade balance decreased a little.

This number is going to be subject to two more revisions, and I would expect this number to be revised upward. Most economic data do not suggest that growth ground to a halt in Q1, just that it slowed down from Q4’s +2.2%. I suspect this will seal the deal that the first rate hike will be in September, not June.

Mortgage Applications fell 2.3% last week, as purchases were flat and refis fell 3.7%.

Pending Home Sales rose 1.1% in March, more or less in line with estimates.

Filed under: Morning Report | 13 Comments »

Posted on April 28, 2015 by Brent Nyitray

Markets are flattish this morning as the FOMC begins their meeting. Bonds and MBS are down.

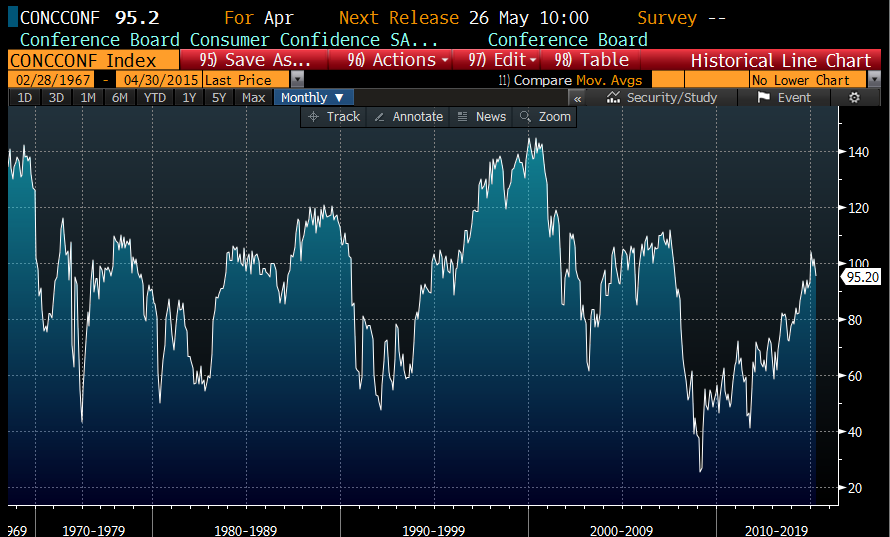

Consumer Confidence slipped in April, to 95.2 from 101.3. Consumers’ appraisal of current-day conditions continued to soften. Those saying business conditions are “good” edged down from 26.7 percent to 26.5 percent. However, those claiming business conditions are “bad” also decreased from 19.4 percent to 18.2 percent. Consumers were less favorable in their assessment of the job market. Those stating jobs are “plentiful” declined from 21.0 percent to 19.1 percent, while those claiming jobs are “hard to get” rose from 25.5 percent to 26.4 percent. The current reading is just about the historical average.

The FOMC meeting begins today. This is should be the last meeting where rate hikes are off the table. Given the weak first quarter, and subsequent economic weakness, the consensus has shifted markedly from a June hike to a September hike. As an aside, we will get the advance estimate for Q1 GDP tomorrow, and the consensus is that the economy grew at 1%. Granted, some of that is weather-driven, but there is no question the economy has slowed dramatically from the Q214-Q315 pace of 4.6%-5.0%. The jobs report next week will be huge.

Home Prices increased .93% month-over-month and 5.03% year over year, according to Case-Shiller. Overall, prices are about 10% below their 2006 peaks, however some hot markets like Denver and San Francisco have surpassed that peak already. Price inflation is being driven by a lack of supply, not wage growth, which means that prices will probably flatline once new home construction kicks into gear or until wages start increasing. We will get a good read on wages this Thursday, with personal income and personal spending.

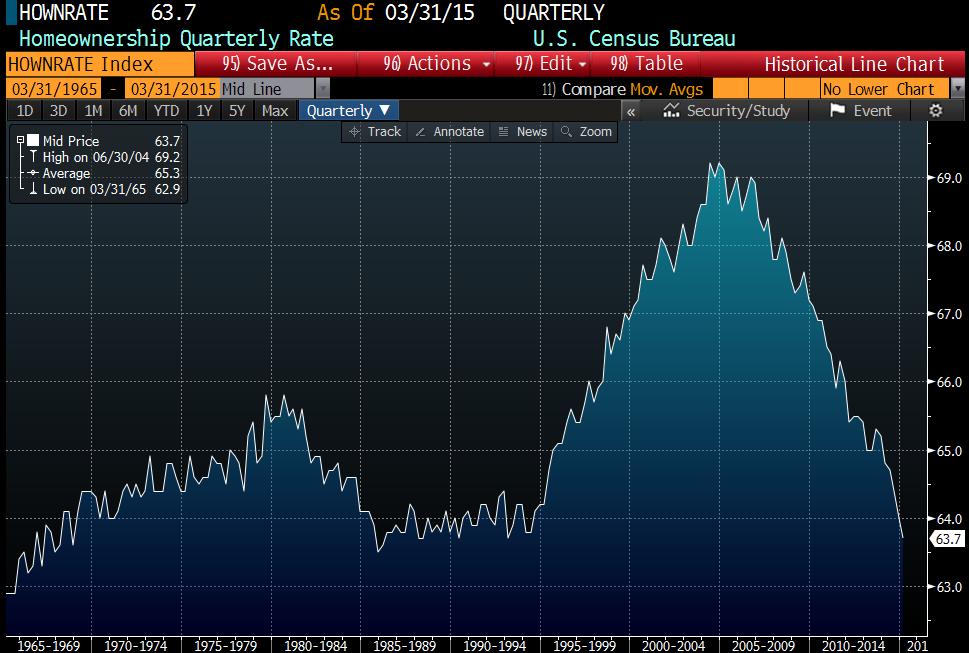

The homeownership rate fell to 63.7% in Q115, from 64% in the fourth quarter of 2015. Pretty much all of the increase that started with the Clinton Administration’s homeownership initiatives in the mid 90s have been given back.

Filed under: Morning Report | 11 Comments »

Posted on April 27, 2015 by Brent Nyitray

Markets are higher on no real news. bonds and MBS are down small.

Not much in data this morning. The Markit PMI numbers fell slightly in April from March. I think we can officially scrap “the weather did it” excuse for weak numbers.

The FOMC meets this week, and this will be the last meeting where rate hikes are not on the table. It won’t contain any new forecasts and it won’t have a press release. It should be a nonevent.

This week contains some important economic data (especially for the Fed). We will get the advance estimate for Q1 GDP, Personal Income and Personal Spending, and the PCE deflator (the Fed’s preferred measure of inflation). Note that the first Friday of the month is this week, but the government is delaying the jobs report until next week. The GDP report is going to be weak – the Street forecast is +1.0% – however personal income could move the bond market if we start seeing wage inflation. The PCE deflator will be important on the other side – if inflation remains well below the Fed’s target they have an excuse not to move. Finally, we get construction spending and the Case-Shiller index.

The battle between Quicken and the DOJ is heating up. Quicken CEO Dan Gilbert spoke truth to power on Friday: “This is what happens when you dare to stand up for justice and the truth to the Department of Justice,” Gilbert said on a conference call Friday evening with the Free Press. “This was an attempt to embarrass us and continue to pressure us to write enormous size checks to settle (allegations) to make them go away, and to admit things that did not occur.” The industry is rooting for Quicken on this one – believing the government is systematically making mountains over immaterial clerical error molehills in order to squeeze more 8 and 9 digit settlements out of the industry. Of course, then the government scratches its head wondering why credit is tight, especially at the lower FICO scores. Is it time to start pushing the housing recovery forecast out to 2017? I hope not. At least one economist thinks 2015 is going to be good.

Filed under: Morning Report | 21 Comments »

Posted on April 24, 2015 by Brent Nyitray

Markets are higher this morning on good earnings out of US companies. Bonds and MBS are up small.

Durable Goods rose 4% in March, however if you strip away transportation, they fell .2%. February was revised downward. Capital Goods orders (a proxy for business capital expenditures) fell .5% and February was revised down to -2.2%. We have seen a slew of disappointing data this quarter – Merrill Lynch is now forecasting Q1 GDP growth of 1.5%.

Comcast has officially pulled the plug on its merger with Time Warner Cable. Washington hated this deal from Day 1, and it became apparent this week that neither the FCC nor the DOJ was going to wave this through.

Yesterday was a monumental day (of sorts) for stocks. The Nasdaq finally eclipsed its high from March 2000. Back then the mentality was to buy quality stocks, don’t worry about the price, just hold out for the long term. For a trip down memory lane, remember the “four horsemen” of tech – the supposedly bulletproof stocks according to Jim Cramer were INTC, DELL, MSFT, and CSCO. Where are they now? Intel is down 57% from the peak, Dell was taken private in 2013 at $13.75, a 77% discount to its 2000 peak, If you were in Mr. Softee, you would be up 10% over 15 years, and almost all of your return would have beeen via the 2.7% dividend. Finally, you would have been much better off in the “other Cisco” – food service company Sysco (SYY) – than you would have been in CSCO, which is down 60% from its peak. No, Virginia, you cannot simply “buy good companies whatever the price, and expect to make money over the long term.”

That era’s madness was perfectly encapsulated in the stock split beeper – a pager that would go off when a company announced a stock split. Cause nothing creates value like a stock split.

In many ways, the four horsemen of tech were similar to the Nifty Fifty of the 1970s – one decision stocks like Avon and Polaroid. They worked until they didn’t. In the physical sciences, knowledge is cumulative. In the financial markets, it is cyclical.

In other words, don’t worry about a bubble in the NASDAQ. People realize that stocks are just an asset that can go up or down – there is nothing special about them. Without that mentality of investors, you aren’t going to have a bubble. Bonds on the other hand…

The NAHB is forecasting 2015 will be “slow and steady” for housing and 2016 will be the breakout year. The pent up demand of the first time homebuyer will be the catalyst, but we have been waiting for a long time for that.

Filed under: Morning Report | 10 Comments »