Posted on September 25, 2015 by Brent Nyitray

Markets are higher this morning after Janet Yellen soothed concerns over global growth and said the Fed is probably still going to raise rates this year. Bonds and MBS are down.

I see a headline coming across the tape that House Speaker John Boehner is going to resign from Congress, according to the New York Times. Don’t see anything on the NYT site, but if so, this is big news.

The third revision to second quarter GDP came in at +3.9%. Personal consumption was revised upward to 3.6% from 3.1%. Inflation remains more or less at the Fed’s target rate of 2%. 3Q GDP forecasts are much lower, in the 1% – 2% range.

Consumer sentiment slipped in September, according to the University of Michigan. This is the lowest reading in a year.

Janet Yellen spoke yesterday, and said the Fed will probably still raise rates this year, however they were willing to let the labor market run hot for a while. The markets were cheered by these statements. She mentioned getting discouraged workers back into the workforce, and that is somewhat new – historically, they have focused on unemployment and wage inflation. Here is a deeper dive into what she was talking about. Interestingly, the Fed thinks that early on ZIRP had little to no effect on the economy, and that only now, are we starting to see the economic benefits of ZIRP. IMO, it has always been about real estate prices. Once real estate bottomed in 2011 / 2012 the economy began a more robust recovery.

Filed under: Morning Report | 26 Comments »

Posted on September 24, 2015 by Brent Nyitray

Markets are lower this morning after Caterpillar warned and announced it will cut 5,000 jobs. Bonds and MBS are up.

New Home Sales rose to an annualized 552k in August, which easily beat expectations. While new home sales have more than doubled from their early 2011 lows, we are still well below what could be considered “normalcy.”

Durable Goods orders fell 2% in August, coming in better than estimates. Capital Goods Orders (a proxy for business capital expenditures) fell 0.2% versus expectations of 0.5%.

The Chicago Fed National Activity Index slipped in August from 0.51 to -.41. This index has had one positive reading all year.

Initial Jobless Claims came in at 267k. The Bloomberg Consumer Comfort Index fell to 41.9.

Builder KB Home reported better than expected earnings this morning but disappointed on orders. Orders were up 19% to 2,167 units. Backlog increased 36%. Average selling prices rose 9% to $357.2k from $327k. The stock is down about half a buck on the open.

Filed under: Morning Report | 21 Comments »

Posted on September 23, 2015 by Brent Nyitray

Markets are flattish this morning on no real news. Bonds and MBS are down small.

Mortgage Applications rose 13.9% last week, with purchases rising 9.1% and refis rising 17.7%. Refis increased to 58.4% of all loans. This was the first full week after the Labor Day holiday, so don’t break out the champagne quite yet – the increase was due to a holiday-shortened week before.

Mario Draghi (European Central Bank President) said more time is needed to assess whether more stimulus is needed.

Bill Gross wrote about financial repression (essentially having rates pegged at the zero bound) and the risks it poses to the financial system. He makes the point that pension funds are getting hammered because they cannot generate the required return on assets with safe assets so they are taking more and more risk, citing municipalities like Chicago, Detroit, etc. He argues that we should be willing to take some short-term financial pain for longer term financial stability. Of course Dr. Cowbell has a different take, which is that bankers want higher rates because they hate poor people and want them to suffer. Or something.

Has ATR and HMDA restricted mortgage credit? Not according to the Fed. Probably because credit has been highly restrictive since 2008. It couldn’t have gotten any tighter to begin with. Note that QM was intended to make lender more likely to lend. Given what we have seen with the big banks exiting FHA (Wells and Chase), the CFPB’s new rules aren’t having the desired effect.

Filed under: Morning Report | 24 Comments »

Posted on September 22, 2015 by Brent Nyitray

Stocks are lower this morning on overseas weakness and slumping commodity prices. Bonds and MBS are up.

The Richmond Fed Manufacturing Index fell in September. The strong dollar is hurting manufacturing.

Scott Walker dropped out of the Republican presidential campaign yesterday. His staffers went to the Rubio campaign, which tells you how the pros are reading the tea leaves with respect to the Republican presidential nomination.

Housing affordability is the lowest since 2008, as the median house price to median income ratio becomes stretched again. Affordability peaked between 2011 and 2013, however professional investors were the ones in a position to take advantage of it. Credit conditions continue to improve, but are still a fraction of what they were pre-crisis.

The big banks are backing away from the FHA market, citing regulation and worries about giving loans to 520 FICO borrowers who only put 3.5% down. Separately, Ginnie Mae is worried about the fact that small independent mortgage bankers are filling the void left by the big banks. The industry is concerned that the big bank withdrawal is hurting the housing recovery.

Filed under: Morning Report | 22 Comments »

Posted on September 21, 2015 by Brent Nyitray

Stocks are up this morning on no real news. Bonds and MBS are down small.

Existing Home Sales fell 4.8% month-over-month in August. On a year-over-year basis they were up about 4.7%. The median home price rose to $228,700, which puts the median house price to median income ratio over 4x, which is pretty high. The first time homebuyer accounted for 32% of sales, which is an uptick from 28% last month. Inventory continues to be a problem, although it did increase to 2.29 million homes, which represents a 5.2 month supply. A balanced market is about 6 – 6.5 months’ supply. Days on market increased to 47 days from 34 two months ago.

Homebuilder Lennar reported earnings that topped estimates this morning. Deliveries were up 16%, while orders were up 20%. Average selling prices were 350k, up 8.9%. Incentives were down to 5.6% from 5.8%. Stuart Miller, CEO characterized the market this way: “During the third quarter, the housing market continued to improve in its slow and steady manner, as demonstrated in the past few years. The new home and rental markets continued to have significant pent-up demand, which positions us well for years to come. This demand is driven primarily by a large production deficit built up over the last several years, an increasing millennial population, reasonable affordability levels and high-rental occupancy rates.”

A new Harvard study points out how the rent vs buy decision is becoming even more skewed towards buying as rental inflation continues to increase. The number of US households that spend at least half their income on rent could increase 25% to almost 15 million over the next decade. Note that the homebuilders are pretty much all venturing into multi-family housing as well as single family, which should alleviate this problem at least to some extent. We have had a production deficit for single and multi-fam construction for several years, prices keep rising, and yet housing starts remain at about 75% of normal levels (ignoring the boom and bust years).

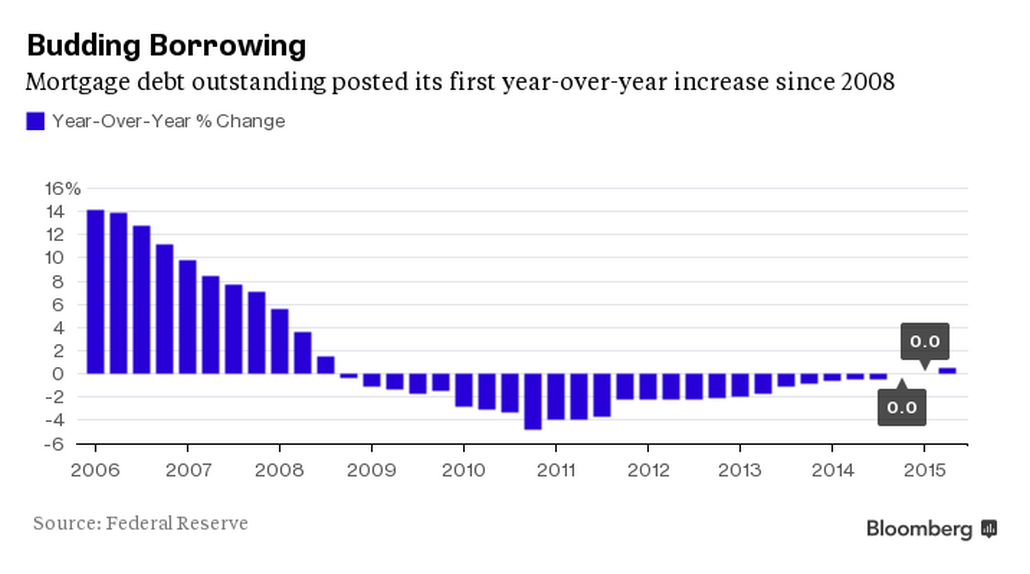

At least one housing statistic is showing signs of returning to normalcy – mortgage debt outstanding is rising again. This was the first gain since 2008. Such an extended contraction in mortgage debt is pretty much unprecedented, at least as far back as the data goes (late 1940s). Of course anyone in the mortgage business could tell you it has been nuclear winter since the crisis began.

Various Fed-heads are still making the case for a December rate hike. Note that the Fed Funds futures contracts are pricing in something like a 50-50 chance for a hike in December. It is kind of hard to reconcile the Fed forecasting sub 5% unemployment and rates pegged to the zero bound.

Filed under: Morning Report | 22 Comments »

Posted on September 18, 2015 by Brent Nyitray

Stocks are getting crushed this morning after the FOMC decision to not raise rates. Bonds and MBS are rallying.

The index of leading economic indicators rose 0.1% in August.

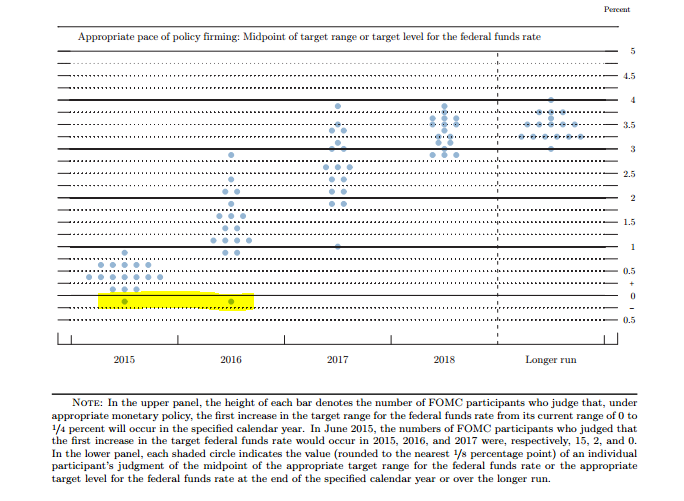

The Fed maintained rates yesterday, citing concerns over the global economy. Bonds rallied on the news while stocks rallied initially and then sold off. Even the statement was dovish. The new economic forecasts lowered GDP, unemployment, and inflation projections. The dot graph showed FOMC participants are forecasting lower interest rates through 2018 than they were in June. In fact, one participant thinks rates should be lower! Take a look at the dot graph below. Someone is predicting the Fed Funds rate should be negative this year and next. That is new.

Here are the economic projections:

GDP is lowered, as is unemployment to below 5%. Note the Fed doesn’t think it will hit its inflation target of 2% until 2018 (!). To me, this means the Fed is anticipating that the labor force participation rate is going to stay low – that is the only way to explain low unemployment and low GDP. They also seem to think that the overhang of these workers on the sidelines will be enough to keep wage inflation low.

What does that mean for bonds and mortgage rates? If that forecast plays out, you could see short term rates increase and long term rates really not move all that much. To me it means a few more years of mortgage rates right around where they are now. This should be good for housing.

Filed under: Morning Report | 25 Comments »

Posted on September 17, 2015 by Brent Nyitray

Markets are lower this morning after housing starts disappoint. Bonds and MBS are flattish.

Today is Fed day. We should get the decision around 2:00 pm EST. Expect bond market volatility (or at least be prepared for it). The consensus seems to no move and very hawkish language in the statement.

Initial Jobless Claims fell to 264k last week, an extremely strong reading. People who have jobs are keeping them.

The Bloomberg Consumer Comfort Index fell to 40.2 from 41.4 last week. 31% of respondents think the economy is excellent / good, while 69% think it is not-so-good / poor.

Housing starts fell to a 1.12 million pace in August, below the 1.16 estimate. July was revised downward from 1.21 million to 1.16 million. Building Permits rose to 1.16 million from an upward-revised 1.13 million. Both single fam and multi-fam dropped. We are entering the seasonally slow period for the builders, so I wouldn’t read too much into these numbers.

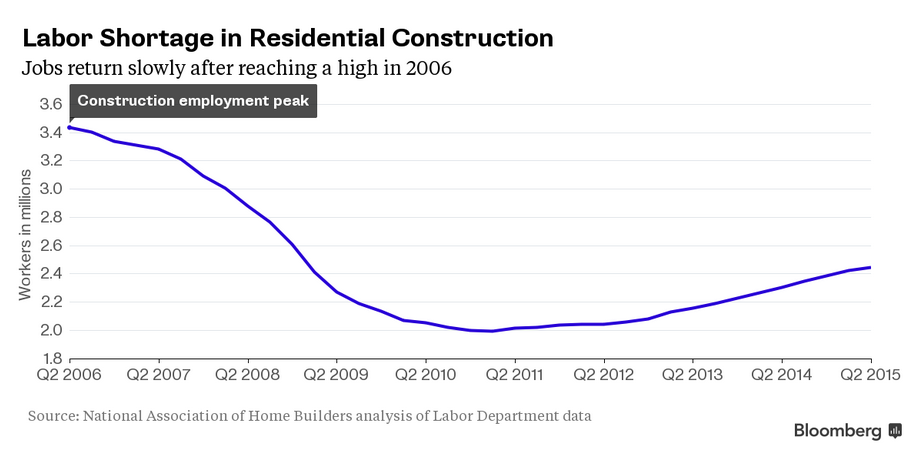

We have tremendous pent-up demand for homes and the inventory of homes for sale is very light. So why aren’t we seeing more homebuilding? Part of the problem is a shortage of labor. Many of the construction workers from the housing boom have either left to new industries (mainly energy), aged out of the workforce, or left the country. 22% of construction workers are foreign, and the NAHB is asking for a temporary guest worker program to fill demand for workers. Right now, the builders are stealing skilled workers from each other using higher pay as an incentive to move.

This of course begs the question why there is a shortage in the first place. The labor force participation rate is stuck at almost 40 year lows and presumably many would want these jobs, which pay well. They aren’t retail / hospitality minimum wage jobs. Are the people who involuntarily left the workforce too old to do construction work? Are they untrainable? It seems strange we would have labor shortages with so much apparent slack in the labor market, but here we are….

Filed under: Morning Report | 31 Comments »

Posted on September 16, 2015 by Brent Nyitray

Stocks are flat this morning as the FOMC begins their two day meeting. Bonds and MBS are up small after getting whacked yesterday.

Mortgage applications fell 7% last week, as purchases fell 4.2% and refis fell 9.1%.

The NAHB Homebuilder index hit a post-recession record of 62 – the highest since October 2005.

The consumer price index fell 0.1% month-over-month as the strong dollar hurts commodity prices. Ex-food and energy, prices were up 0.1% month-over-month and 1.8% year-over-year. That is close to the Fed’s target, however they prefer to use the personal consumption expenditures data, which uses a different balance of goods to calcluate it.

Real average weekly earnings rose 2.3% last week.

When the FOMC releases their decision tomorrow, they will include their economic forecasts. For this entire recovery, the Fed’s estimates of future growth have been consistently high. IMO, the reason for this comes from the fact that the Fed’s models are largely based on prior experience which has been Fed-driven inventory-based recessions since WWII. In these cases, inflation increases -> the Fed raises rates -> the economy slows -> inventory builds up -> people get laid off -> a recession begins -> the inventory gets sold -> new production starts up -> workers get re-hired -> the economy recovers. These recessions are typically short and the recoveries tend to be V-shaped. This recession is different because it wasn’t driven by the Fed raising rates and inventory buildup, it was driven by a bursting asset bubble. The issue with these recessions is that the problem isn’t excess inventory – it is bad debt and mal-investments. And these are typically longer and deeper recessions, with longer and shallower recoveries. Instead of a V-shaped recovery, you get a bathtub-shaped recovery. The economy recovers once the bad debt and bad assets are liquidated, which takes longer.

This leads into the latest negative equity report by CoreLogic. 10.9% of all homes with a mortgage (or about 5.4 million homes) have negative equity. 9 million (or about 18%) have a small amount of equity. 800k homes with negative equity would become equity positive if house prices increase 5%. Note that many of these properties may never sell (abandoned homes in rust-belt cities for example) so the effect on the real estate market will probably be muted. But that is one of the reasons why the inventory of existing homes for sale is so small. Negative equity has a drag on the economy be preventing workers from moving to where the jobs are because they cannot sell their house without a ding on their credit ratings. Just another example of the mal-investments that hold back the economy. The economy will accelerate as these mal-investments are liquidated and borrowers and creditors move on.

Filed under: Morning Report | 25 Comments »

Posted on September 15, 2015 by Brent Nyitray

Stocks are up this morning as we await the big day Thursday. Bonds and MBS are down.

Retail Sales rose 0.2% in August, just missing the 0.3% Street estimate. The control group (which excludes volatile and price-sensitive goods like autos, gasoline and building supplies) rose 0.4%, which was better than the 0.3% Street estimate. August is the back-to-school month, so overall decent numbers, which bodes well for the holiday shopping season. Big retailers like Amazon.com and Wal Mart are up pre-open.

Industrial Production fell in August by 0.4%, which was lower than the -0.2% estimate. Capacity Utilization fell to 77.6% from 77.8%. Separately, the Empire Manufacturing Survey (which measures manufacturing activity in New York State) was highly negative at -14.7. The strong dollar is taking a bite out of manufacturing activity.

Business inventories and sales rose 0.1%. The inventory-to-sales ratio held steady at 1.36x. The inventory / sales ratio has been ticking up recently, which is a worrisome sign, at least for a cyclical recession. During recessions, it is not uncommon to see a big spike in this ratio. Historically, it has been much higher. You can see on the graph below the latest increase, and also the secular decline in the ratio that began in the mid-80s as manufacturing implemented just in time inventory management.

Tim Duy, an influential Fed-watcher makes the case for not moving this week. His argument: With rates at the zero bound and market turmoil, the Fed has no margin for error since it is more or less out of ammo. Better to wait until the waters are calmer to make a move. FWIW, I tend to agree with those arguments, and I think the Fed is very wary of a 1937 scenario. Inflation is nowhere to be found and while there is a bubble in credit markets, widening credit spreads are acting as a tightening all by themselves (the Larry Summers argument).

The argument for raising rates: – we have bubbles in the credit markets, and certainly in the pre-IPO market. Uber, which earns nothing, and has a market cap similar to Dow Chemical, is indicative of a craziness we haven’t seen since the skyrocketing IPOs of eToys and Pets.com in the late 90s. Stocks are up 200% from the lows in 2009. His point is that we DO have inflation – but it is “too much money chasing too few assets,” not “too much money chasing too few goods.” Imagine if the Fed had raised rates in 2003 and the real estate bubble had popped in 2004. We still would have had a recession, but I seriously doubt the banking system would have collapsed the way it did in 2008. And the recession would have certainly been shorter and less severe than 2008 – 2009. His point: it is time to end the addiction to low interest rates. The economy is strong enough to take a Fed Funds rate of 50 basis points. This argument is highly, highly unpopular in policy circles, so it won’t get any traction. The consensus in Washington (at least on the left, which runs things at the moment) was that policy had absolutely nothing to do with the bubble – it was 100% Wall Street Sharpies that did it, and “smart regulation” will prevent another one from happening.

Note that the one advocating for standing pat is a professor, and the one advocating moving is a trader. So they will look at the issue from two entirely different points of view.

As credit spreads have widened, we have seen some jumbo securitizations pile up at the banks. This probably signals less aggressive jumbo pricing ahead. LOs – something to tell your borrowers, especially if they are thinking of floating right now. Even if the 10 year bond goes nowhere, jumbo rates could be heading up.

Filed under: Morning Report | 67 Comments »

Posted on September 14, 2015 by Brent Nyitray

Markets are flattish this morning as overseas markets stabilize. Bonds and MBS are up.

No economic data today. We will have some important economic data this week retail sales and industrial production on Tuesday, with housing starts on Wednesday.

The big event this week will be the FOMC meeting on Wednesday and Thursday. The announcement will come on Thursday. For mortgage bankers, the focus will be in the Fed Funds rate, and also “reinvestment tapering.” Reinvestment tapering has to do with the Fed’s re-investment of maturing Treasuries and MBS that it bought during QE. Currently, the proceeds from any maturing MBS are re-invested back into the MBS market, in order to keep the Fed’s balance sheet constant. At some point, they will stop doing that, and you may see mortgage spreads widen. This means that mortgage rates could increase, even if the 10 year goes nowhere. Note that they probably will taper, meaning they won’t stop re-investing maturing proceeds all at once. They’ll probably cut it by $5 billion a month, similar to how they executed the tapering in the first place.

The Fed Funds futures are currently projecting about a 30% chance the Fed will tighten this week. Fed Vice Chairman Stanley Fischer is advocating moving before the inflation numbers begin to rise. “There is always uncertainty and we just have to recognize it,” he told CNBC television on Aug. 28. Asked if the Fed should delay an increase until it had an “unimpeachable case” that a move was warranted, Fischer replied, “If you wait that long, you will be waiting too long.” On the other side of the coin, many in the Fed are worried about repeating the mistake of 1937, where the Fed tightened (really only by a little bit) and the economy dove back into recession.

Exhibit (A) in the “ZIRP is not free” argument: Petrobras sold 100 year (!) bonds last June, and as oil has dropped so have these bonds. They dropped into the 60s recently. What does this have to do with ZIRP? Everything. When central banks hold down rates artificially, the price signals the market uses to assign risk (interest rates) become distorted and investors are forced to reach for yield. You see it mainly with pension funds and insurance companies, which have to hit a return bogey based on longevity and health care inflation. Yes, getting 6.85% in this interest rate environment is attractive, but, you are lending to a Brazilian oil producer for 100 years and only getting 6.85% a year! The last 3 times the Fed raised rates (94,99, and 05) they blew up the MBS market, the stock market bubble and the residential real estate bubble. This bond issue shows how much of a credit bubble we currently have. The Fed may have painted themselves into a corner, but until inflation comes back, they can wait.

Presidential candidates are beginning to put out their tax and spending plans. Jeb Bush recently put out his tax plan, and there are some items that will directly affect those in the real estate business. First, his plan reduces rates and limits deductions. State and local taxes will no longer be deductible. Second, there will be a cap on itemized deductions, which means people who have a large mortgage and pay a lot of mortgage interest will find themselves with a higher tax bill. This will probably have a negative effect on the jumbo side of the market, although it will present an opportunity for LOs to try and pitch refinancing from 30 year mortgages to 15 year mortgages. While the mortgage interest deduction is as American as apple pie and may in fact be a political third rail, economists believe that it hasn’t really increased the homeownership percentage, as it was intended to do – it just encouraged people to buy bigger houses.

Filed under: Morning Report | 14 Comments »