Vital Statistics:

| Last | Change | |

| S&P futures | 2642 | 0 |

| Eurostoxx index | 357.3 | 2.93 |

| Oil (WTI) | 52.35 | 0.36 |

| 10 year government bond yield | 2.73% | |

| 30 year fixed rate mortgage | 4.62% |

Stocks are flat as we begin the FOMC meeting. Bonds and MBS are up small.

Despite the end of the shutdown, we will have to wait for economic data. Two big reports this week – GDP and personal incomes – have been delayed.

Economic activity picked up in December, according to the Chicago Fed National Activity Index. Production-related indicators and employment drove the increase. Note that the CFNAI is a meta-index of a number of announced economic indices, and the government shutdown has decreased the amount of data going into the index. We’ll see the same effect next month as well, so the index won’t be as accurate as it usually is. Regardless, the CFNAI is an amalgamation of previously released data, so it doesn’t move markets.

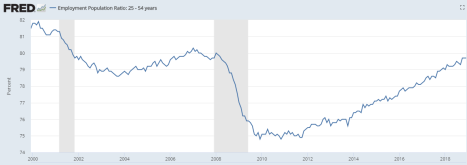

Ex-Fed Head Narayana Kochlerakota thinks the Fed should consider easing at the next meeting. His argument is that the Fed has been falling short in maintaining inflation at its 2% target and that notwithstanding the latest unemployment data we are still not at full employment. He is looking at the percentage of prime age people (age 25-54) who are currently employed. We are just south of 80%, and were closer to 82% during the late 90s. Given that the number of prime age people in the US is roughly 100MM, then we have about 2 million more jobs to create in order to get to back to where we want to be. Interestingly, he not only advocates maintaining the current balance sheet, he thinks it should increase about 4% a year to grow in lockstep with the economy.

Guess what has been one of the best performing assets so far this year (almost tripled in under a month). If you guessed the GSEs, you would be correct. The market is betting that shareholders won’t get wiped out when / if housing reform happens this year. Check out this chart of Fannie Mae:

Ginnie Mae is stepping up oversight of its partners, particularly non-bank lenders, telling some that they must improve some financial metrics before they will be granted more commitment authority, which is the ability to securitize FHA and VA loans. The government is concerned that non-bank lenders have replaced a lot of the traditional banks in servicing government loans. Indeed, they have – nonbanks now service 61% of government loans, up from 34% at the end of 2014. FHA was largely a backwater of the mortgage market pre-crisis, however post crisis, it has picked up the load that subprime left. Servicers for government loans have a lot more liquidity demands than servicers for GSE loans – and in a downturn the advances liability could take out undercapitalized mortgage bankers. VA lenders can face what is called no-bid risk, which can be a disaster for many servicers without a line of credit to cover advances and loan buyouts.

Filed under: Economy, Morning Report | 21 Comments »