Vital Statistics:

|

Last |

Change |

| S&P futures |

2783 |

-23.1 |

| Oil (WTI) |

26.09 |

0.29 |

| 10 year government bond yield |

|

0.63% |

| 30 year fixed rate mortgage |

|

3.36% |

Stocks are lower this morning on no real news. Bonds and MBS are up.

Initial Jobless Claims came in at 3 million last week. This puts the number of jobs lost to COVID at 36.4 million, or about 430 jobs per death.

The FHFA made an announcement yesterday which permits servicers to allow borrowers who enter forbearance to wait to pay back the skipped payments until they either refinance the loan or at maturity.

“For homeowners in forbearance due to COVID-19, payment deferral allows them to make up missed forbearance payments when they sell their home or refinance,” said FHFA Director Mark Calabria. “This new forbearance repayment solution responsibly simplifies options for homeowners while providing an additional tool for mortgage servicers. Borrowers who can pay their mortgage should, because missed payments remain an obligation that will ultimately have to be repaid.”

Servicers are required to evaluate borrowers for one of several repayment options, generally referred to as a “hierarchy” of repayment and loan modification options. The big question is whether the borrower can demand the servicer provide the option they want. Who has the final say on the repayment plan? The borrower or the servicer? Plus, since Fannie will reimburse the 4 months of advances immediately, does the servicer have any financial incentive to choose one plan or the other?

One of the biggest deterrents to taking forbearance was that you would be unable to refinance your mortgage until the missed payments are made up. But, since this contemplates paying it off on a refi, then I guess that isn’t the case? I am sure FHFA and the GSEs will provide more guidance.

Remember the huge Fannie and Freddie LLPAs for loans that go into forbearance before they are sold to Fannie Mae? Correspondent lenders are removing them. I haven’t seen anything official, but it looks like the government might have backtracked on that one.

While Jerome Powell was greasing the skids for a prolonged recession, that might not be what happens. Don’t forget, there was nothing wrong with the economy to begin with. No bubbles, no buildup of inventory and bad debt, no mal-investments to work off. The economy was put into a medically-induced coma. The real work of recessions – working off excess inventory, disposing of bad assets, trimming bloated payrolls, isn’t applicable here.

The stimulus dollars (along with people being free to not pay their mortgage for a year) will provide an immense jolt to the economy. Think of what you would do if you all of a sudden could just, stop, paying your mortgage for a year. And you didn’t have to pay it off until you refinance or move? That is a lot of additional disposable income.

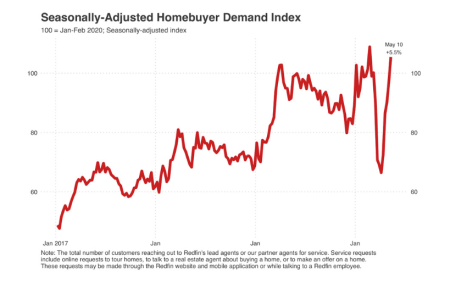

Even with COVID-19, some of the hottest markets are still going strong. The Denver area is still going strong. FWIW, I was listening to the Equity Residential earnings call the other day, and the company noted that traffic and applications started off down 50% on a YOY basis in March when the government initiated the stay at home orders. Things have improved so much that traffic and applications are now flat YOY. Delinquencies? About 5%. While Equity Residential is mainly affluent renters, this is a pretty interesting data point. Note however that the Multifamily Housing Council reported that 20% of renters have failed to make their May payment as of May 6, so it isn’t all great. But so far so good.

Filed under: Economy, Morning Report | 24 Comments »