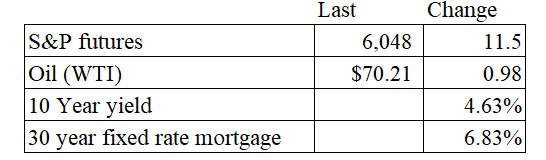

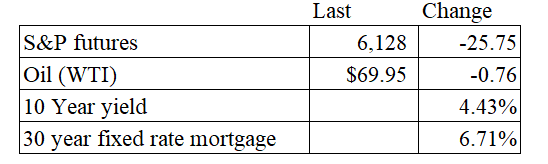

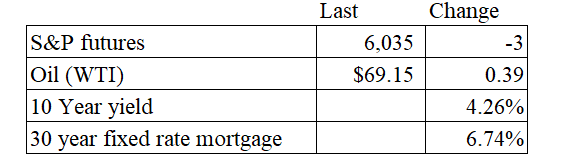

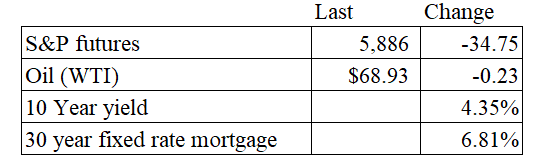

Vital Statistics:

Stocks are flattish this morning on no real news. Bonds and MBS are down.

The bond market is down again today, with UK Gilt yields up 12 basis points this morning. Adding to the pressure on bonds was a lousy auction yesterday, with the 10 year yield hitting the highest level since 2007.

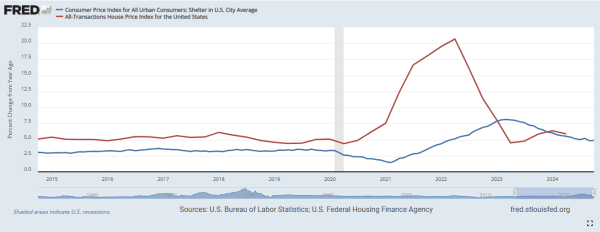

Job openings increased to 8.1 million at the end of December, according to the Bureau of Labor Statistics. This was an increase of 259k from the upward-revised November reading. On the other hand, the quits rate declined to 1.9%, which is a sign of weakness in the labor market.

Given the current bearish psychology of the bond market, bond investors focused on the 8.1 million job openings and ignored the quits rate. The red line is the job openings rate, while the blue line is the quits rate. The job openings rate is higher than pre-pandemic levels, while the quits rate is below pre-pandemic levels.

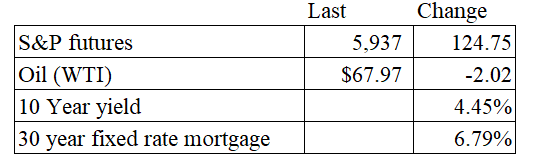

More indications that the labor market is cooling: The economy added 122,000 jobs last month, according to the ADP Employment Report. This was below expectations, and is less than Street expectations for Friday’s jobs report. “The labor market downshifted to a more modest pace of growth in the final month of 2024, with a slowdown in both hiring and pay gains,” said Nela Richardson, chief economist, ADP. “Health care stood out in the second half of the year, creating more jobs than any other sector.” Indeed, the bulk of the gains came in health care / education and leisure / hospitality. Manufacturing jobs fell.

Pay gains for job stayers fell to 4.6%, the lowest since July of 2021.

Mortgage applications fell 3.7% last week as purchases fell 7% and refis fell 2%. “Applications decreased last week as rising mortgage rates continued to discourage buyers from entering the market and put a damper on purchase activity. The 30-year fixed rate increased for the fourth consecutive week, reaching 6.99 percent – the highest rate since July 2024,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Purchase applications declined for both conventional and government loans and dropped to the slowest weekly pace since February 2024. Refinance applications increased despite higher rates, but the increase was compared to recent low levels and was driven entirely by an increase in VA refinances, which continue to show weekly swings.”

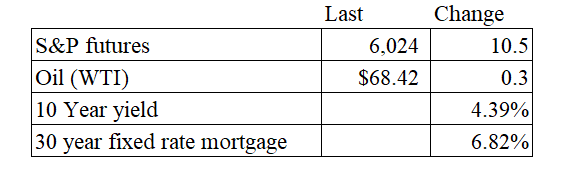

Adding fuel to the bonfire in the bond market was the ISM Services report, which showed the sector expanding again. “The Services PMI® in December was boosted primarily by strength in the Business Activity and Supplier Deliveries indexes. Many industries noted that end-of-year and seasonal factors were helping drive business activity or impact inventory management. Some of the increased business activity seems to have been driven by preparation for demand in the new year, or risk management for impacts from ports strikes and potential tariffs. There was general optimism expressed across many industries, but tariff concerns elicited the most panelist comments.”

The prices index increased to 64.4%,which was the highest reading since January of 2024. There might have been some seasonal / end-of-year effects going on, so this is something to watch.

Filed under: Economy | 22 Comments »