Vital Statistics:

| Last | Change | |

| S&P Futures | 2177.0 | 1.0 |

| Eurostoxx Index | 342.8 | 1.0 |

| Oil (WTI) | 42.9 | -0.2 |

| US dollar index | 86.9 | -0.2 |

| 10 Year Govt Bond Yield | 1.58% | |

| Current Coupon Fannie Mae TBA | 103.3 | |

| Current Coupon Ginnie Mae TBA | 104.2 | |

| 30 Year Fixed Rate Mortgage | 3.5 |

Markets are flattish this morning on no real news. Bonds and MBS are flat

Small Business Optimism ticked up last month according to the NFIB. Sentiment remains well below its historical average. The interesting thing is that the inability to find quality workers rose to the #3 problem facing small business after taxes and government regulation. While small business is interested in hiring, they still have very little appetite for capital expenditures. Inflation at the small business level remains nowhere to be found, as small business cut prices on average last month.

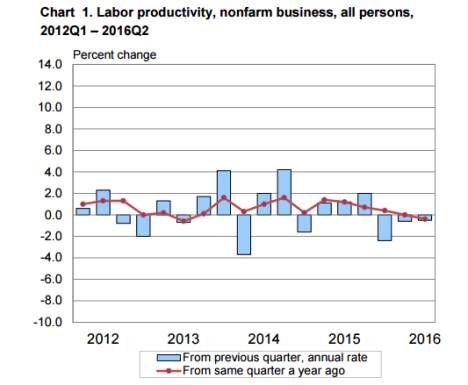

The lack of capital investment ties into another economic number this morning: productivity (or lack thereof). Nonfarm productivity fell .5% in the second quarter, making it the third negative quarter in a row. The Street was looking for a positive .5% reading so the number was a big miss. Productivity is also negative on a year-over-year basis.

Unit Labor costs rose 2% which was a little higher than expected. Comp costs were up 1.5% and productivity losses added another 50 bps.

Productivity growth is what increases standards of living, which is why a lack of it makes people feel like the recovery is so weak. Part of the explanation is found in the NFIB report – no capital expenditures. Productivity is tough to measure these days, with so much free technology. You know GoToMeeting increases productivity, yet it won’t show up in the output numbers because no one pays for it. Same thing with Skype, LinkedIn, etc. While academia suspects there is a problem with the way we measure productivity, no one has found a good way to correct for it.

Completed foreclosures came in at 38,000 in June, a 4% increase from May and a 5% drop year over year. The national foreclosures inventory stands at 375k homes, which is down 26% from a year ago. The number of mortgages seriously delinquent fell 21% YOY to 2.8%, or about 1.1 million homes. The big judicial states like New York and New Jersey lead the pack in foreclosure inventory.

FHFA says that Fannie Mae and Freddie Mac could require as much as $126 billion in the next housing crisis. Separately, Fannie’s home purchase sentiment index hit a new high, albeit it is a relatively new index.

Wells is saying that the expiration of HARP at the end of the year. Does this mean a dramatic drop in prepay speeds? Not necessarily, in that HARP will probably be replaced with a high LTV refi program.

Filed under: Economy, Morning Report | 5 Comments »