Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1413.5 | 8.2 | 0.58% |

| Eurostoxx Index | 2500.1 | 9.5 | 0.38% |

| Oil (WTI) | 86.63 | 0.9 | 1.05% |

| LIBOR | 0.313 | -0.001 | -0.32% |

| US Dollar Index (DXY) | 79.82 | -0.091 | -0.11% |

| 10 Year Govt Bond Yield | 1.84% | 0.05% | |

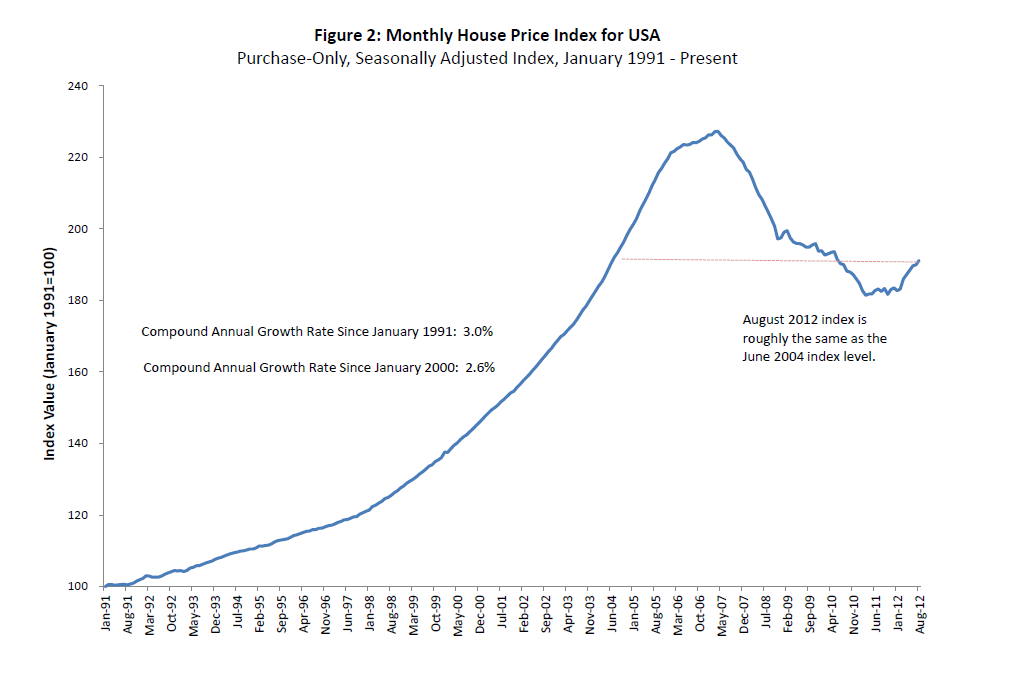

| RPX Composite Real Estate Index | 194.1 | -0.1 |

Markets are stronger this morning after a strong durable goods report and a good UK GDP number. Initial Jobless Claims came in at 369k and last week was revised upward to 392k. Capital Goods orders were flat. We had a slew of decent earnings reports this morning, and Apple will report after the close. Bonds are getting clocked on the durable goods number, with the 10 year down a point and mortgages down 10 ticks.

The Chicago Fed National Activity Index came in flat, but the 3 month moving average is still negative, indicating the economy is growing below trend.

The FOMC statement yesterday was more or less a rehash of the prior statement. Bond Traders who were looking for the Fed to add Treasuries to the QE mix were disappointed. The Fed noted that household spending has been advancing, while growth in fixed business investment has slowed. Today’s durable goods and capital goods reports bear that out.

The global slowdown is causing another round of job cuts. This time, it is more than just Wall Street as Ford, Dow Chemical, Colgate Palmolive, AMD, and HP are all cutting staff. The number of announced job cuts in the last 2 months is the highest since 2010.

The government is going after Bank of America for the sins of Countrywide. Needless to say, the consumer groups are delighted. Lenders warn that credit will become even tighter. Certainly the litigation risk will get passed onto borrowers through higher rates and fees. Barney Frank believes the government should lay off JP Morgan for the sins of Bear, and claims that the government asked BOA to buy Merrill, but not Countrywide.

Whatever happened to the San Bernardino eminent domain idea? This was the plan that involved the county taking performing underwater mortgages from the banks and forgiving principal. It appears the firestorm of criticism has caused the county to quietly table the idea.

Speaking of foreclosures, ABC News has a depressing photo essay of the foreclosure crisis.

Filed under: Morning Report | 13 Comments »