Posted on January 13, 2014 by Brent Nyitray

Vital Statistics:

| S&P Futures |

1832.4 |

-5.3 |

-0.29% |

| Eurostoxx Index |

3107.0 |

2.8 |

0.09% |

| Oil (WTI) |

91.7 |

-1.0 |

-1.10% |

| LIBOR |

0.239 |

-0.003 |

-1.14% |

| US Dollar Index (DXY) |

80.72 |

0.063 |

0.08% |

| 10 Year Govt Bond Yield |

2.86% |

0.00% |

|

| Current Coupon Ginnie Mae TBA |

105.5 |

0.8 |

|

| Current Coupon Fannie Mae TBA |

103.8 |

0.1 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.46 |

|

|

Stocks are down small this morning while bonds continue to hold onto Friday’s gains. There is no important economic data this morning with the exception of the budget report sometime later on today.

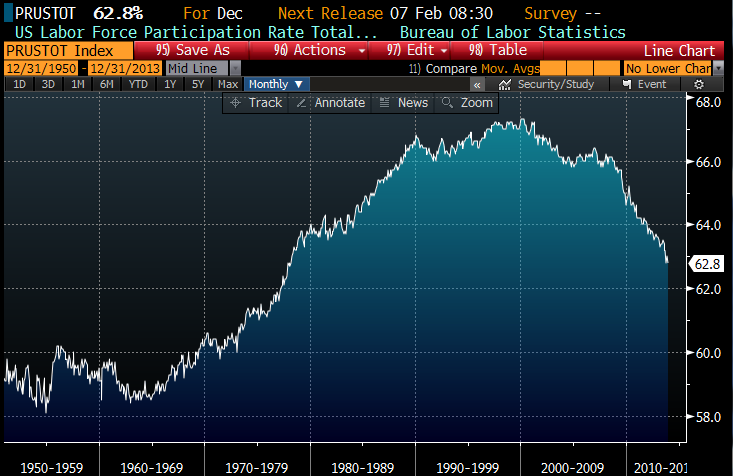

The stock market seems to be taking Friday’s jobs report as sort of a one-off, while bonds seem convinced that it signals something bigger. The most disappointing statistic in the report was the decline in the labor force participation rate to 62.8%, which means last month’s rebound was just a blip. One worrisome stat – the biggest decline in the labor force participation rate came in the 45 – 55 year old cohort. In other words, people in their prime spending years. I personally know a lot of people who were rounding the final turn towards Candy Castle and then drew the candy cane card.

This week begins earnings season, with the big banks reporting. J.P Morgan and Wells report tomorrow, Bank of America is on Wed, Citi is Thursday, and Suntrust is Friday. I’m sure we will hear about all of the woes in the origination business. From what I am seeing, margins have to be terrible for them, and a combination of lower volume and lower margins is a toxic cocktail.

Tomorrow morning we will get retail sales, which will be an important data point, particularly for estimates of Q4 GDP. Later on this week we will get housing starts and building permits. It will be interesting to see whether November’s 1.1 million print was a fluke or evidence of further strength in the housing market.

Filed under: Morning Report | 77 Comments »

Posted on January 10, 2014 by Brent Nyitray

Vital Statistics:

| S&P Futures |

1837.4 |

4.4 |

0.24% |

| Eurostoxx Index |

3111.5 |

21.2 |

0.69% |

| Oil (WTI) |

92.63 |

1.0 |

1.06% |

| LIBOR |

0.242 |

0.000 |

0.00% |

| US Dollar Index (DXY) |

80.8 |

-0.207 |

-0.26% |

| 10 Year Govt Bond Yield |

2.90% |

-0.07% |

|

| Current Coupon Ginnie Mae TBA |

104.7 |

0.2 |

|

| Current Coupon Fannie Mae TBA |

103.4 |

0.5 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.54 |

|

|

Markets are stronger after a mixed jobs report. Payrolls expanded at an anemic 74k in December (versus the Street expectation of 197k, and the unemployment rate came in lower than expected, falling to 6.7%. Alcoa kicked off 4Q earnings season with a miss. Bonds and MS are rallying on the news.

Headline statistics from the report:

- Payrolls + 74k vs 197k expected

- Unemployment rate 6.7% vs 7% expected

- average hourly earnings + .1% MOM, + 1.8% YOY

- Average workweek 34.4 hours, down .1 hour

- Labor force participation rate 62.8% down from 63%.

The low payroll number was blamed on weather, which may explain the moves in the market. Stocks initially sold off hard and then rallied back. That said, even if you exclude the weather related effects, payroll growth was still sluggish. The labor force participation rate moved right back to its lows. The participation rate is back to levels we haven’t seen since the late 70s. To put that in perspective, roughly half of the gains in the labor force participation rate that began in the 1960s with women entering the labor force have been given back. We still have a lot of wood to chop before we get back to a semblance of normalcy. One other observation – ADP has been lousy at predicting the jobs number lately. They had the number at 238k.

Chart: Labor Force Participation Rate 1950 – Present

The jobs report probably does not change the stance of the Fed, and I would expect another $10 billion reduction in QE at the Jan FOMC meeting.

The Mortgage Bankers Association is

forecasting $1.2 trillion in origination for 2014, the lowest level in 14 years. Banks will continue to fire people and there is still overcapacity in the system. I wonder what assumptions about cash purchase percentages they are using…

Filed under: Morning Report | 24 Comments »

Posted on January 9, 2014 by Brent Nyitray

Vital Statistics:

| S&P Futures |

1836.9 |

4.4 |

0.24% |

| Eurostoxx Index |

3119.8 |

9.1 |

0.29% |

| Oil (WTI) |

92.79 |

0.5 |

0.50% |

| LIBOR |

0.242 |

0.001 |

0.52% |

| US Dollar Index (DXY) |

81.05 |

0.026 |

0.03% |

| 10 Year Govt Bond Yield |

2.97% |

-0.02% |

|

| Current Coupon Ginnie Mae TBA |

104.5 |

0.0 |

|

| Current Coupon Fannie Mae TBA |

103.3 |

0.0 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.52 |

|

|

Markets are up this morning as initial jobless claims drop to 330k. Of course last week contained the New Year’s holiday so it is tough to read too much into this number. Alcoa kicks off fourth quarter earnings season after the bell. Bonds and MBS are up small.

There was nothing earth-shattering in the

FOMC minutes which were released yesterday afternoon (the bond market basically yawned at the whole thing). Things were more or less characterized as expanding “moderately”, with a few “modests” thrown in as well. Manufacturing expanded “briskly” which was a first. The Fed did mention the issue of possible capital losses on its portfolio, and particularly how that would affect the reputation of the Fed. They talk about how spin the losses – basically telling people that you need to look at the whole picture, not just the Fed’s p/l. In other words, the Fed may end up passing losses to Treasury, which will increase the deficit, but you have to take into account the fact that this process helped the economy, which increased tax revenues. Guess dynamic scoring is permitted for the Fed but not for anyone who proposes a tax cut.

Retailers are reporting same-store sales this morning, so far it looks looks like a mixed bag with Costco and Macy’s beating estimates, while apparel retailers like Limited Brands missing.

It is official: the FHFA has delayed the increase in G-fees and the new new LLPAs. Luckily for lock desks, the FHFA will give 120 day’s notice if they decide to change things. Borrowers are probably going to save 3/8 of a point with this. The NAR is onboard with this move.

Filed under: Morning Report | 16 Comments »

Posted on January 8, 2014 by Brent Nyitray

Vital Statistics:

| S&P Futures |

1830.6 |

-0.1 |

-0.01% |

| Eurostoxx Index |

3107.9 |

-3.1 |

-0.10% |

| Oil (WTI) |

93.86 |

0.2 |

0.20% |

| LIBOR |

0.24 |

-0.002 |

-0.70% |

| US Dollar Index (DXY) |

81.04 |

0.203 |

0.25% |

| 10 Year Govt Bond Yield |

2.99% |

0.05% |

|

| Current Coupon Ginnie Mae TBA |

104.4 |

-0.2 |

|

| Current Coupon Fannie Mae TBA |

103.3 |

-0.2 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.5 |

|

|

Stocks are flattish after the ADP Employment change came in better than expected at 238k jobs. The Street was at 200k and the estimate for Friday’s number is 195k. Bonds clearly didn’t like the number, with the 10 year yield around 2.99%.

Mortgage applications rose 2.6% last week, although the holiday makes any sort of week-over-week comparison difficult. Later on today we will get consumer credit and the minutes of the FOMC meeting.

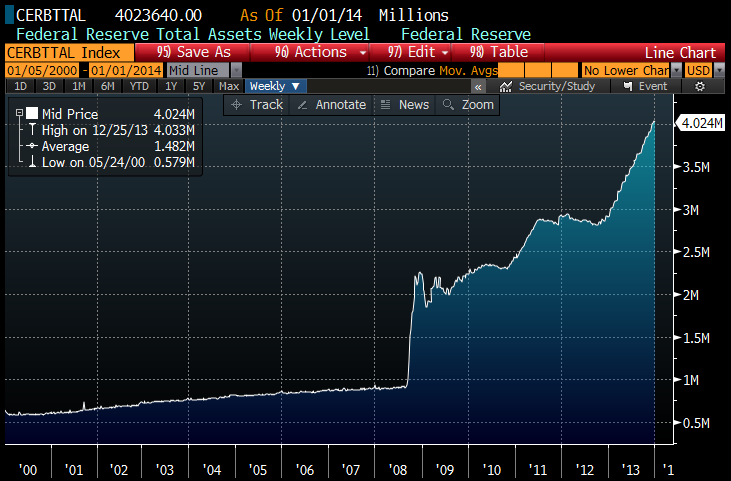

When I discussed Janet Yellen’s new role at the Fed and also showed a chart of the Fed’s balance sheet, I forgot to mention the other important side of things – the equity. Turns out the Fed announces these things weekly. And right now, we have a $4.02 trillion balance sheet supported by $55 billion in equity. For those keeping score at home, that works out to be 73:1 leverage, or about 2.6 times the leverage that blew up Long Term Capital Management. The Fed is long duration and levered 73:1 in a rising interest rate environment. And they are still building up the balance sheet, just at a slower pace than before. Everyone hopes Janet can stick the landing, but this is no sure bet.

56 out of 350 metro areas returned to or exceeded their last normal levels of economic and housing activity,

according the the NAHB. More than 35% of all the markets are withing 90% of previous norms. Where does your MSA stack up? Find out

here.

State of the unemployment extension: Yesterday, the Senate

had a test vote that passed a 3 month extended unemployment benefits extension, however several of the Republicans who said “yea” would vote “nay” if there weren’t paid for. Of course we have the House which would probably extend benefits if they are paid for with spending cuts.

Filed under: Morning Report | 32 Comments »

Posted on January 7, 2014 by Brent Nyitray

Vital Statistics:

| S&P Futures |

1827.6 |

6.9 |

0.38% |

| Eurostoxx Index |

3094.6 |

25.4 |

0.83% |

| Oil (WTI) |

93.82 |

0.4 |

0.42% |

| LIBOR |

0.242 |

0.003 |

1.15% |

| US Dollar Index (DXY) |

80.7 |

0.051 |

0.06% |

| 10 Year Govt Bond Yield |

2.95% |

-0.01% |

|

| Current Coupon Ginnie Mae TBA |

104.3 |

0.0 |

|

| Current Coupon Fannie Mae TBA |

103.3 |

-0.5 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.53 |

|

|

Markets are higher this morning on no real news. The trade gap narrowed on lower oil imports. Bonds and MBS are up small.

3 days to QM…

Janet Yellen

was sworn in as the next Federal Reserve Chairman. She will officially take office Feb 1, and is tasked with slowly extricating the Fed’s footprint from the economy and bringing its balance sheet back to historical normal levels. Note that the

vote was actually closer than the Bernank’s (56-26) reflecting the political polarization happening in Washington and the Fed.

Mel Watt was sworn in as FHFA Director yesterday. In a statement issued by FHFA Watt said, “I am honored to serve as Director of the Federal Housing Finance Agency. Today’s housing finance system is one of the keys to our economic recovery and I am grateful for the opportunity to help develop a strong foundation for moving this system forward for the benefit of all Americans at this critical point in our nation’s history.” You can read the “for the benefit of all Americans” to mean that he is going to target lower income lending. Mel is a CRA guy to the bone.

The fight over unemployment extension seems to boil down over whether to pay for it or not. Democrats are against setting the precedent that extended unemployment benefits be “paid for” and are at the point where they believe no more non-defense spending can be cut. Republicans are coalescing around the “extend benefits, but find some other spending to cut” position.

Filed under: Morning Report | 8 Comments »

Posted on January 6, 2014 by Brent Nyitray

Vital Statistics:

| S&P Futures |

1831.2 |

5.7 |

0.31% |

| Eurostoxx Index |

3080.1 |

5.7 |

0.19% |

| Oil (WTI) |

94.1 |

0.1 |

0.15% |

| LIBOR |

0.239 |

-0.001 |

-0.21% |

| US Dollar Index (DXY) |

80.87 |

0.083 |

0.10% |

| 10 Year Govt Bond Yield |

2.98% |

-0.02% |

|

| Current Coupon Ginnie Mae TBA |

104.1 |

0.1 |

|

| Current Coupon Fannie Mae TBA |

103.1 |

0.1 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.55 |

|

|

Markets are higher this morning on no real news. Bonds and MBS are up small.

This week will have a couple big items – the FOMC minutes and the jobs report. The big question with the minutes will concern whether tapering is in fact on autopilot. Ben Bernanke indicated in the press conference that it more or less is on autopilot, but we will want to read the minutes to get some more clarity. Given that the mystery over whether the Fed will begin tapering is over, the jobs report will probably not have that much of an impact, unless it is extraordinarily strong. Finally, Janet Yellen will be confirmed this week, which should be a nonevent.

This week also kicks off earnings season, with Alcoa reporting after the bell on Thursday. Given the huge run-up we have seen in the stock market, companies better deliver. FWIW, perma-bull Jim Paulsen is cautious going into 2014.

Bloomberg has a

piece on the enigma that is Mel Watt. The only thing we know for sure is that he has suspended the g-fee increases and the LLPAs for the moment. Since he has yet to be officially sworn in, he is playing things close to the vest. I don’t know why people would call him an “enigma.” Mel couldn’t even bring himself to come out against the eminent domain policies that some localities are pursuing. That says it all, IMO. At the end of the day, Mel Watt is a liberal CRA guy. All you need to know about how he will conduct policy is to see him through that lens. He wants credit to be easier for low-income borrowers. He likes government involvement in the mortgage market. Whether that means Fannie and Freddie continue in their current form or not is an open question. But at the end of the day, he is going to err on the side of more government involvement, not less. Whether that makes the Fannie Mae prefs a buy is another question.

Filed under: Morning Report | 30 Comments »

Posted on January 3, 2014 by Brent Nyitray

Vital Statistics:

| S&P Futures |

1830.5 |

3.9 |

0.21% |

| Eurostoxx Index |

3074.7 |

14.8 |

0.48% |

| Oil (WTI) |

95.11 |

-0.3 |

-0.35% |

| LIBOR |

0.24 |

-0.003 |

-1.24% |

| US Dollar Index (DXY) |

80.72 |

0.089 |

0.11% |

| 10 Year Govt Bond Yield |

3.00% |

0.01% |

|

| Current Coupon Ginnie Mae TBA |

103.8 |

-0.2 |

|

| Current Coupon Fannie Mae TBA |

102.9 |

-0.1 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.55 |

|

|

Markets are higher this morning on no real news. Bonds and MBS are flattish. A snowstorm in the Northeast has many traders at home, so I don’t expect a lot of movement today. The Bernank speaks at 2:30 EST. Can’t imagine he is going to steal any of Janet’s thunder, but you never know.

It is looking like December domestic vehicle sales are not coming in as strong as hoped. Many analysts attributed the disappointment to bad weather.

The ISM New York index of business conditions fell, but is still at the high end of its range. It looks like most retailers deferred releasing comp store sales to next Thursday, so that will be an important data point for the state of the consumer.

Filed under: Morning Report | 51 Comments »

Posted on January 2, 2014 by Brent Nyitray

Vital Statistics:

|

Last |

Change |

Percent |

| S&P Futures |

1836.4 |

-4.7 |

-0.26% |

| Eurostoxx Index |

3086.9 |

-22.1 |

-0.71% |

| Oil (WTI) |

97.66 |

-0.8 |

-0.77% |

| LIBOR |

0.243 |

-0.003 |

-1.32% |

| US Dollar Index (DXY) |

80.69 |

0.581 |

0.73% |

| 10 Year Govt Bond Yield |

3.02% |

-0.01% |

|

| Current Coupon Ginnie Mae TBA |

104 |

0.1 |

|

| Current Coupon Fannie Mae TBA |

103.1 |

0.1 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.55 |

|

|

Markets are down to kick off the new year. Bonds and MBS are down. Initial Jobless Claims came in at 339k, a little lower than expected. We are scheduled to get hit with a big snowstorm this afternoon in the Northeast, so I would imagine bonds are going to become a little more illiquid this afternoon.

Some more bullish economic data – the Dec ISM manufacturing index came in a little better than expected at 57, and construction spending increased 1% month-over-month, topping expectations.

The buy-and-rent business

is getting tougher. Part of the reason why the origination business has been so tough is that the most aggressive buyers these days are cash institutional buyers. Depending on who you ask, cash buyers are anywhere from 40% to 50% of buyers these days. Historically they have been closer to 20%. So even if existing home sales stay the same, the number of homes with mortgages on them could increase 45% or so if we went back to normal cash / mortgage percentages.

Filed under: Morning Report | 14 Comments »

Posted on December 31, 2013 by Brent Nyitray

Vital Statistics:

|

Last |

Change |

Percent |

| S&P Futures |

1838.2 |

3.5 |

0.19% |

| Eurostoxx Index |

3109.0 |

8.1 |

0.26% |

| Oil (WTI) |

98.32 |

-1.0 |

-0.98% |

| LIBOR |

0.246 |

-0.001 |

-0.20% |

| US Dollar Index (DXY) |

80.06 |

0.056 |

0.07% |

| 10 Year Govt Bond Yield |

2.99% |

0.02% |

|

| Current Coupon Ginnie Mae TBA |

104 |

-0.1 |

|

| Current Coupon Fannie Mae TBA |

103.1 |

0.0 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.54 |

|

|

Markets are slightly higher on the last day of the year. Bonds and MBS are down.

Short day, with stocks and bonds closing at 1:00 pm. Expect low liquidity

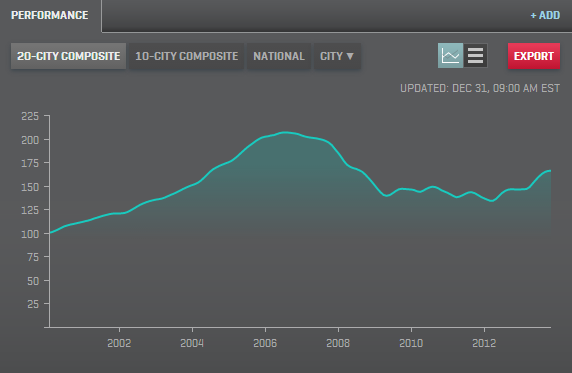

The

Case-Shiller index rose 13.6% year over year in October. This was slightly higher than the Street estimate of +13.5%. This is the biggest gain since Feb 2006. Same old story – a restricted inventory of foreclosed properties keeps supply tight and offsets the cooling demand from increasing mortgage rates. Of course the first time homebuyer is the one who suffers the most in this situation – competing for a limited supply of low-end homes with professional cash buyers who don’t care what mortgage rates are.

Short sales may be more difficult in the new year – the

tax break on principal forgiveness ends. It appears that there is some sort of desire to extend this through 2014 – it may get bolted on to an extended unemployment bill. I wonder if Mel Watt was planning some sort of new HAMP initiative. Given the acceleration we have been seeing in Case-Shiller, by the time any sort of new government program finally gets ready for launch, home price appreciation may make the whole thing moot anyway.

Filed under: Morning Report | 36 Comments »

Posted on December 30, 2013 by Brent Nyitray

Vital Statistics:

|

Last |

Change |

Percent |

| S&P Futures |

1836.3 |

-0.2 |

-0.01% |

| Eurostoxx Index |

3098.8 |

-12.6 |

-0.41% |

| Oil (WTI) |

99.86 |

-0.5 |

-0.46% |

| LIBOR |

0.247 |

0.000 |

0.00% |

| US Dollar Index (DXY) |

80.12 |

-0.270 |

-0.34% |

| 10 Year Govt Bond Yield |

2.98% |

-0.02% |

|

| Current Coupon Ginnie Mae TBA |

104 |

0.2 |

|

| Current Coupon Fannie Mae TBA |

103.1 |

0.2 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.56 |

|

|

Markets are flattish on the penultimate day of 2013. Bonds have bounced back below 3% in yield. The ISM Milwaukee came in better than expected, and we will also get pending home sales later.

Today is also Black Monday for losing NFL coaches. Leslie Frasier is gone, as is Rob Chudzinski. Are Shanny and Schwartz next?

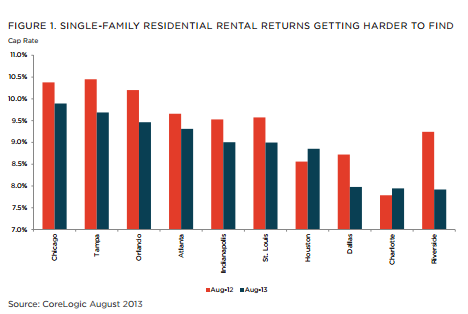

CoreLogic’s latest

Market Pulse is out, and as usual it is full of good stuff. One thing they discuss is that cap rates are falling for rental markets as prices have increased. Which means that the bidding wars of professional cash buyers are probably over. As prices appreciate, expect to see the pros begin to ring the register. For originators, this means we can still have purchase apps increase as cash buyers drop from 40% of buyers back to their more typical 20% of buyers.

The consensus is growing that 2014 will be the year the economy finally

gets out of first gear.

Job creation is back towards 200k a month, consumer confidence is rising, and 3Q GDP came in at +4.1%, though I wouldn’t read too much into that number. Pent-up demand is finally becoming unleashed. One thing to watch: if extended unemployment benefits aren’t renewed, we should see a drop in unemployment as people take part-time jobs to pay the bills. That won’t necessarily be an indication of economic strength, but it may matter psychologically.

Filed under: Morning Report | 22 Comments »