Posted on February 23, 2015 by Brent Nyitray

Existing home sales fell to a 4.82 million unit pace in January from an upward-revised 5.07 million pace in December, according to the National Association of Realtors. Inventory is still tight at 4.7 months (6.5 is more or less a balanced market), but it is up from 4.4 months in December. The median home price is $199,600, an increase of 6.2% year over year. All cash transactions were 27%, down from 33% a year ago, and distressed sales were 11%, down from 15% a year ago.

Janet Yellen will make her semiannual trek to the Hill to discuss monetary policy in front of Congress. The prepared remarks will undoubtedly be closely parsed, and the sense on the Street is that Yellen wants to lower expectations somewhat for a June rate hike. Aside from that, HH is generally a waste of time for market watchers. These are generally for the benefit of politicians who like to use it as a platform to pontificate on issues important to them. The left will try to get her to agree with their views on inequality and the minimum wage, while the right will probably go after the long-term risks of ZIRP. It will be interesting to see if someone asks about the “audit the Fed” movement. She testifies in front of the Senate tomorrow at 10:00 am EST, and in front of the House on Wed.

A deal in the servicing field this morning: New Residential is buying subprime servicer Home Loan Servicing Solutions for $1.3 billion. HLSS has been examining strategic alternatives since last November, and the stock is up smartly. The servicing sector as a whole has gotten slammed from the Ocwen mess and the drop in interest rates.

Speaking of servicing, Ocwen is trying to sell a 9.8 billion servicing portfolio to Nationstar.

If the US economy is improving (and all evidence says it is), why are banks still piling into Treasuries? There are a couple of reasons. First, is Basel III. They were required by the regulators to increase their holdings of Treasuries. Second, if you look at the Bloomberg total return index on US Treasuries over the past year, they returned 8.8% in 2014. That includes periodic interest and capital gains. Compare that to the typical rate on a business development loan, or a line of credit paying LIBOR + 200 or something. Treasuries are working. And given the yields in European bonds, and the strength of the dollar, there is an underlying foreign demand for Treasuries. Yes, at some point Treasuries will become an awful bet, but that won’t happen until inflation kicks in and that isn’t happening at the moment.

Chart: Bloomberg 10 year Treasury total return index:

Filed under: Morning Report | 38 Comments »

Posted on February 20, 2015 by Brent Nyitray

Markets are lower this morning as the EU / Greek kabuki dance continues. Bonds and MBS are up.

The Markit US Manufacturing PMI Index rose to 54.3 in Feb from 53.9 in January. Good reading, given the fact that the Northeast got slammed with snow all month.

Greece is set to run out of cash as early as next month, so the talks with the EU are increasingly important. Remember, this is all a kabuki dance. Greek voters want to stay in the Euro, and German voters want Greece to stay in the Euro. They will get a deal done, although bonds will be buffeted by the day-to-day headlines.

Megan McArdle on why Wal-Mart raised wages. It was not due to labor activists – it was a business decision to try and minimize turnover and motivate employees. This is good news for wage growth in general, as companies may be forced to raise wages to compete. The great stagnation might be ending.

Filed under: Morning Report | 67 Comments »

Posted on February 19, 2015 by Brent Nyitray

Markets are flattish after Germany rejected a loan extension request from Greece. Bonds and MBS are flattish as well.

Initial Jobless Claims fell to 283k last week, which is a good number given the drop in oil prices. Eventually layoffs will start in the energy patch.

The Bloomberg Consumer Comfort Index rose to 44.6 last week, while the Philly Fed fell and the Index of Leading Economic Indicators ticked down from .5% to .2%.

WalMart reported Q4 earnings that beat analyst expectations. The biggest news out of it, is that WMT is increasing starting wages to $9.00 / hour in April and by Feb next year, all current associates will be making at least $10 an hour, If this is due to market pressures, then that is great news for the economy. If it was due to political pressure (though no one is taking credit so far) then it tells you less. The raise will be part of a larger program to streamline scheduling and other operational issues, and should cost about 20 cents a share over the next year.

The minutes of the Jan FOMC meeting were considered more dovish than expected. Bonds rallied hard on the announcement, as it appears some members are beginning to get cold feet about raising rates this June. Janet Yellen and Ben Bernanke are students of the Great Depression and are probably going to err on the side of waiting too long versus tightening too early.

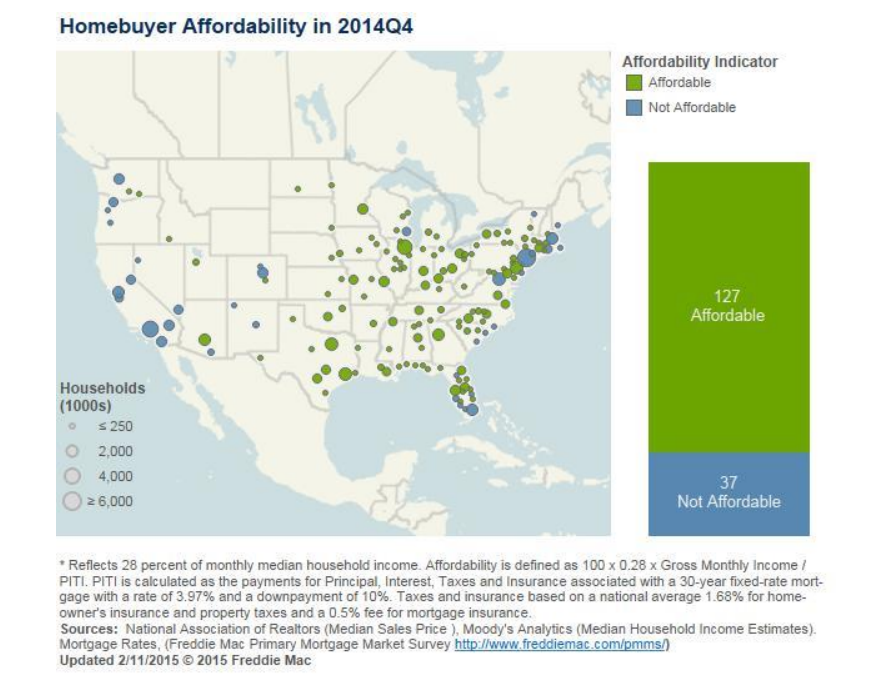

Freddie Mac took down its numbers for Q1 GDP to 2.5% from 3%, raised 2015 origination forecasts to $1.3 trillion from $1.2 trillion, cut the forecast 30 year fixed rate mortgage rate to 3.9% from 4.2% and is predicting 3.9% home price appreciation. Forecasts for home sales (5.6 million) and housing starts (1.18 million) are unchanged. Affordability is still a tale of two Americas, with the NYC / DC / South Florida / West Coast being unaffordable, and the rest of the country being affordable.

Filed under: Morning Report | 9 Comments »

Posted on February 18, 2015 by Brent Nyitray

Markets are lower as Greece seeks to limit some of the reforms being demanded from other Euro area members as a condition to extending the country’s 240 billion euro rescue package past February. Bonds and MBS are up small.

Mortgage Applications fell 13.2% last week as purchases fell 7.1% and refis fell 16%. It looks like mortgage rates didn’t move tremendously, at least according to the Bankrate 30 year fixed rate mortgage numbers. Mortgage rates had lagged the move downward in the 10 year, so it is unsurprising they are lagged the move back up. It appears they are beginning to move up with bond yields this week, however.

Housing starts fell 2% in January to an annualized pace of 1.065 million units. Building permits fell .7% to an annualized pace of 1.053 million.

Inflation remains muted at the wholesale level, with the Producer Price Index falling .8% month-over-month. Stripping out food and energy, it fell .1%, month over month, and increased 1.6% year over year.

Industrial Production rose .2% in January, and capacity utilization fell from 79.7% to 79.4%.

Speaking of inflation, there is a labor dispute between the longshoremen and the ports on the West Coast. We are starting to see some stirrings from labor unions, which could mean we are finally seeing the start of wage inflation. That said, the two labor unions involved are in industries which are in the middle of dramatic change. Ports are becoming more and more automated, and quite frankly do not need as many workers as they used to. The longshoreman are simply trying to delay the inevitable and are fighting over work rules that require two people supervise an automated crane. The steelworkers decided to pick a fight just as oil prices are falling and a labor surplus in the oil patch is being generated. Neither side has much in the way of negotiating leverage. That said, it will be interesting to see if they win.

Another data point for the energy patch: Buffett sold all of his Exxon Mobil and ConocoPhillips.

The minutes from the last Fed meeting should be released around 2:00 pm EST, so there is a chance for some bond market volatility around that time.

While it seems like Democrats and Republicans are in a death match struggle over the direction of this country and the days of genteel civility are in the past, here is some perspective. Turkey’s President Recep Tayyip Erdogan has filed a lawsuit against the head of Turkey’s central bank, Erdem Basci, charging him with mismanaging the country’s interest rate policy and not lowering rates as demanded by the government. He faces two years in jail.

Filed under: Morning Report | 10 Comments »

Posted on February 17, 2015 by Brent Nyitray

The Empire Manufacturing Index fell in Feb and came in slightly light. There is almost certainly some weather-related noise in that report.

The NAHB Housing Market Index fell to 55 in February from 57 in January. The index increased in the Northeast and fell in the Midwest. The South and West were more or less unchanged.

We have a lot of data this week with housing starts tomorrow, industrial production / capacity utilization, and finally the FOMC minutes. The minutes should be the big event for the week. The focus will be on handicapping a June rate hike.

Speaking of rate hikes, wage inflation continues to be the missing piece of the puzzle for the economy. That said, Big Labor is waking up, with refinery strikes and a longshoreman’s strike on the West Coast. Strike activity is still well below where it was in the 70s and 80s, but it could be the start of wage inflation.

Finally, I appeared on Capital Markets Today and did a deep dive into the economy and housing. You can listen to the podcast here.

Filed under: Morning Report | 17 Comments »

Posted on February 13, 2015 by Brent Nyitray

Happy Friday the 13th.

Markets are higher this morning on optimism of a deal in Greece and encouraging economic data out of Germany. The Greek 10 year yield is down almost 100 basis points this morning and is approaching 9%. The market has a risk-on feel with stocks up and bonds / MBS down.

Import prices fell 2.8% MOM and 8% YOY. Consumer sentiment fell from 98.1 to 93.7.

Bloomberg has a good piece on Mel Watt and the issues surrounding principal mods for Fan and Fred loans. The biggest question remains: how can you help underwater homeowners without triggering a wave of strategic defaults? 85% – 90% of people whose mortgage is underwater are current on their payments. The last thing you want to do is encourage them to stop paying in order to get a principal mod. Luckily, time has been doing the heavy lifting here, as the number of homes with negative equity has fallen from 31% in 2012 to just about 17% today. Second, many of those homes are not Fan and Fred loans in the first place, and FHFA is only looking at cutting principal on Fan and Fred loans that it owns. The FHFA Home Price Index, which tracks the prices of homes with a conforming mortgage is within 5% of the peak.

Bob Shiller warns of a bond bubble. He is probably right, although it could last some time. Interest rate cycles are long: the current cycle began in 1981 or so. Note that in the 1950s, the bond market crashed and the generation that lost their shirts in the stock market crash of 1929 ended up blowing up in levered flattening trades. Persistently low interest rates can wreak all sorts of havoc, especially with pension funds and insurance companies. They have a return bogey they must meet, and the actuarial tables couldn’t care less that interest rates are zero. Note that Dr. Cowbell is copacetic with all of this. Note that the 4 most dangerous words in investing are: This Time Is Different.

Bill Ackman sees the common stock of Fannie Mae and Freddie Mac as “the best trade in capital markets” He is betting that Congress will eventually stop taking all of Fannie’s profits and allow them to recapitalize in private markets. The thing is, this is a litigation lottery ticket. It is either worth a lot, or worth nothing. If it actually had access to its profits – it doesn’t – all p/l goes to Treasury – it would have a P/E of 1. FWIW, the Administration is bound and determined to see that Fannie Mae common shareholders do not see a dime. But administrations could change, and Congress may decide that housing reform is simply too tough and we go back to the old F&F.

How bad are things in the energy patch? We have another arctic blast hitting the Eastern part of the country and natural gas cannot get out of its own way. Kind of amazing, really.

Filed under: Morning Report | 31 Comments »

Posted on February 12, 2015 by Brent Nyitray

Markets are higher this morning on news of a cease-fire in Ukraine. Bonds and MBS are up.

Greek bonds are rallying with bonds globally. Unusual, as a rally in Greek debt has been triggering the risk-on trade lately.

Retail Sales disappointed in January. The headline number fell .8%, however falling gas prices were a big contributor (gas is measured in dollars, not gallons). However, the control group, which strips out volatile segments like autos, gas, and building materials only rose .1%, versus Street expectations of .4%. The strength appears to be in autos and food service. Bad weather in the Northeast may have played a role in the number, however.

Business Inventories rose .1% and the Bloomberg Consumer Comfort Index fell to 44.3.

Initial Jobless Claims rose to 304k last week. This is going to be a number to watch – falling energy prices are triggering layoffs in the energy patch. Interestingly, part of the reason why labor has been so tight in construction was due to workers moving from the construction sector to the energy sector after the housing bust. As energy prices fall and construction begins to ramp up, this could be good news for the housing sector and especially the homebuilders. The builders have been frustrated by an inability to find skilled labor, and a reversal of the migration from construction to the energy sector should help them.

Julian Castro appeared before the House Financial Services Committee yesterday. His prepared remarks are here. He was there to defend the cut in mortgage insurance and to rah-rah everything the Administration has done to get housing (and the economy) moving. It was basically a defense of an activist government role in the housing market.

Filed under: Morning Report | 25 Comments »

Posted on February 11, 2015 by Brent Nyitray

Stocks are lower worldwide as Greece and Germany continue to posture over future Greek bailouts. The Greek 10 year bond yield is up 33 basis points to 10.58%. Global bonds are up small, and MBS are flat.

Mortgage Applications fell 9% last week as rates backed up 32 basis points. Purchases were down 6.5% while refis were down 10.3%.

Hedge funds that bought distressed mortgage debt in 2008 and 2009 are unwinding their positions as spreads have tightened and real estate prices have risen. Probably next on the agenda is the unwind of the REO-to-Rental trade which has simply not lived up to the hype.

Homebuilder KB Home is doing a $250 million bond issue today. Separately, they announced new orders were up 25% so far this year. Key quote from CEO Jeffrey Metzger: “Based on our expanding community count and the strength of our recent net order results, we are optimistic about the spring selling season. We believe the momentum of these favorable trends, in combination with our solid backlog, support a positive revenue outlook for the remainder of the year, particularly in the third and fourth quarters.”

Lewie Ranieri’s Shellpoint Partners rolled out their non-QM credit repair product in October, and they hope to do their first securitization of these loans this year. They believe the agencies will demand 15% credit enhancement for AAA tranches with high quality non-QM loans, and credit enhancement of 34%-40% for the tougher stuff: 620 FICO, 50 DTI, 80 LTV loans. Shellpoint lends through its New Penn unit. Sounds like we are getting closer to non-QM securitization.

Filed under: Morning Report | 3 Comments »

Posted on February 10, 2015 by Brent Nyitray

Markets are higher this morning as the Greek government offered a compromise on the bailout. Bonds and MBS are down worldwide, with the US 10 year yield flirting with a 2 handle.

The NFIB Small Business Optimism Survey fell to 97.9 from 100.4 in January. Expectations were for a 101. The IBD / TIPP Economic Optimism Index fell in February from 51.1 to 47.5. Job Openings topped 5 million according to the JOLTS survey.

Consumers are feeling a little better about the housing market, according to the Fannie Mae National Housing Survey. Expectations of home price appreciation rose to 2.5% from 2.3% a month ago, and almost half of respondents thing prices will go up in the next year. Americans are still negative on the economy, but less so, with 49% believing we are on the wrong track and 44% believing we are on the right track.

Foreclosure Completions fell to 39,000 in December, a 4.9% drop month-over-month and a 13.7% drop year-over-year, according to CoreLogic. Current foreclosure inventory is 552k homes, a decrease of 34.3% from a year ago. New Jersey and New York continue to lead the US with the highest percentage of foreclosures.

Filed under: Morning Report | 20 Comments »

Posted on February 9, 2015 by Brent Nyitray

Markets are lower this morning on European weakness. Bonds and MBS are up.

This week is going to be relatively data-light, with retail sales being the highlight.

Friday’s jobs report was undeniably strong, but I would keep in mind one thing in the back of my mind: We are in a sort of a sweet spot, where lower energy prices are helping things along, but the big layoffs in the energy sector have yet to materialize. If energy prices stay here, producers will cut production and staff. Also, the Fed will start hiking rates in June and then all bets are off.

Note that last week, Ginnie Mae TBAs underperformed Fannie Mae TBAs are rates shot up. I suspect this is still related to the new MI changes. The bottom line is that conforming pricing is getting more attractive relative to government pricing.

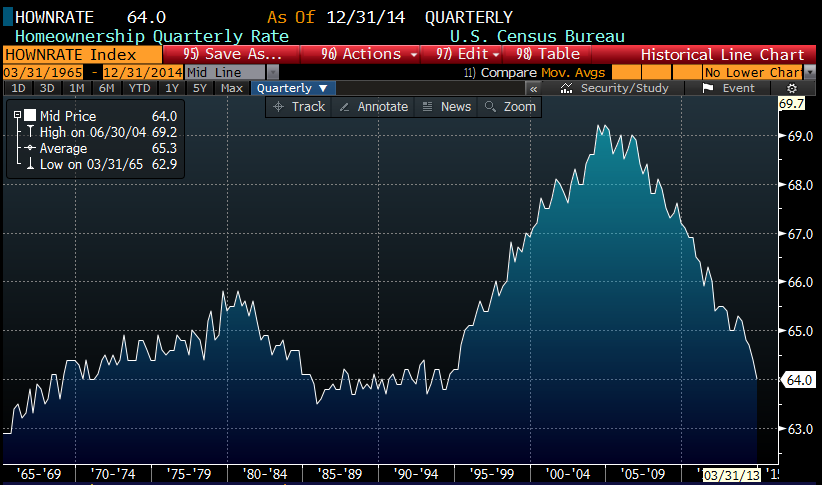

The NY Times comments on the social engineering aspects of the housing market. Note that one of Bill Clinton’s first acts was to prod Fan and Fred into increasing the homeownership percentage. That percentage is now back to 1994 levels more or less. Mel Watt is trying to push it up again, but really has limited tools given that he has to explicitly protect taxpayers and there is still not much of a private mortgage market.

Filed under: Morning Report | 21 Comments »