Vital Statistics:

| Last | Change | |

| S&P Futures | 2176.0 | 0.0 |

| Eurostoxx Index | 341.5 | -1.9 |

| Oil (WTI) | 46.4 | -0.2 |

| US dollar index | 85.8 | 0.2 |

| 10 Year Govt Bond Yield | 1.58% | |

| Current Coupon Fannie Mae TBA | 103.3 | |

| Current Coupon Ginnie Mae TBA | 104.2 | |

| 30 Year Fixed Rate Mortgage | 3.52 |

Markets are flat this morning on no real news. Bonds and MBS are down small.

The FOMC minutes come out today at 2:00 pm EST. Be careful locking loans around then since we could see some volatility.

Mortgage Applications fell 4% last week as both purchases and refis fell by 4%.

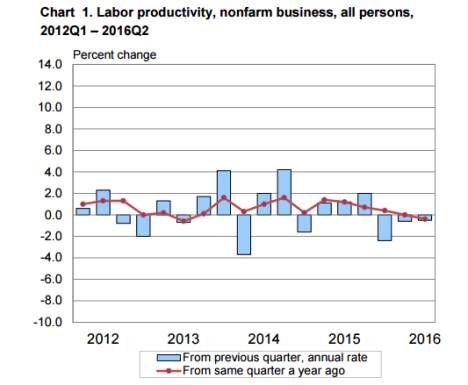

Mohammed El Arian has a good piece on what to look for in the minutes. The main things to look for: labor (and what the Fed considers “full employment), productivity (and why we aren’t seeing it), inflation (and why we don’t see it), external threats (China slowdown, Brexit), and finally why ultra-low interest rates and QE aren’t achieving the desired result (the elephant in the room). Expect the Fed to prod the government to use fiscal policy to help stimulate the economy.

For those complaining that US fiscal policy has been in austerity mode, I would remind them that the biggest post WWII deficits as a percentage of GDP are (in order) 2009, 2010, 2011, 1983, 2012, 1946, 2013.

Yesterday, William Dudley suggested that a September rate hike is still on the table and the markets may be underestimating the chance of one. The Fed Funds futures market have now back to pre-Brexit levels in terms of predicting the probability of a rate hike this year.

The lack of inventory is going to get worse, as we aren’t building enough homes to keep up with population growth, let alone obsolescence. I keep saying this, but we should be hitting 2 million starts a year given the shortage and the need to house Millennials. This is the difference between 2% GDP and 3% GDP. Unfortunately, Washington seems to think the biggest problem is that we aren’t slugging the banks hard enough.

Filed under: Economy, Morning Report | 12 Comments »