Vital Statistics:

| Last | Change | |

| S&P Futures | 2085.7 | 2.0 |

| Eurostoxx Index | 328.9 | -2.6 |

| Oil (WTI) | 44.1 | -0.6 |

| US dollar index | 87.7 | 0.0 |

| 10 Year Govt Bond Yield | 1.79% | |

| Current Coupon Fannie Mae TBA | 103 | |

| Current Coupon Ginnie Mae TBA | 104 | |

| 30 Year Fixed Rate Mortgage | 3.61 |

Stocks are higher after a decent jobs report. Bonds and MBS are up as well.

Jobs report data dump:

- Payrolls increased by 161,000

- Unemployment rate 4.9%

- Labor Force Participation rate 62.8%

- Average hourly earnings 0.4%

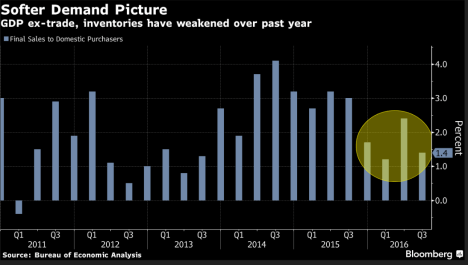

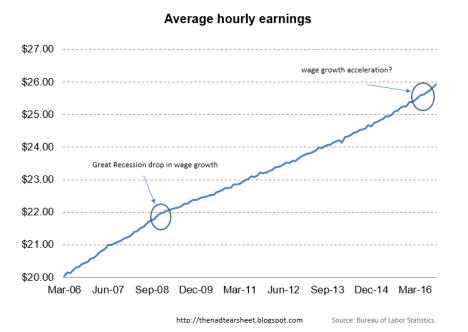

The payroll data was disappointing, as was the decrease in the labor force participation rate. The plus side was wage growth, where wages rose at a 2.8% annual rate, the biggest increase since 2009. The employment to population ratio slipped to 59.7%. Basically, it looks like the number of unemployed fell, however they didn’t get jobs – they exited the labor force. Below is a chart of average hourly earnings. You can see the slope of the line decrease in 2008 as the Great Recession began and wage growth slipped from its bubble year growth rate of 3.3% to 2%, where it largely stayed during the recovery. It appears like the slope of the line is beginning to increase, which solves a lot of problems in our economy. Too early to tell if it is a trend, though. Bottom line: This gives the Fed all the ammo they need to raise the Fed Funds rate next month. FWIW, the Fed Funds futures are now assigning a 80% chance of a 25 basis point hike next month.

Ordinarily, this report would be bond bearish, however global sovereigns are rallying and pulling the 10 year along for the ride.

Ex Dallas Fed Head Richard Fisher blames the rise of Donald Trump partially on Fed policy. The Fed’s policy of driving interest rates to the floor and flooding the system with money to support asset prices is great news for people who own real estate and stocks, however for those that save it has been terrible:

“Global monetary policy has “skewered the middle-income groups, the ‘middle class,’ adding to the angst that has sprung from their sense of an overbearing, intrusive central government….Small wonder that we have ended up at a political crossroad, with a choice for the presidency between a candidate who advocates having government distribute still more to ease the pain and another arguing to provide relief by changing gears entirely, though we know not how, when or where…My more acerbic friends on both sides of the aisle consider it a Hobson’s choice,” he said, referring to a situation where it seems there’s free choice but in reality there’s no good alternative. On the one hand, Republicans believe the other party’s candidate is channeling Eva Peron, planning policies that will ultimately lead us down the Argentine path to economic ruin while basking in personal profit and glory. On the other, Democrats liken the Republican candidate to Caligula.”

On the subject of QE, he is spot-on. QE and unconventional monetary policy has certainly increased inequality, and made life tough if you are a renter. Rental inflation is increasing at a 4% annual clip, and as we saw above, wages are well below that. QE has been great for the landlord, but not the tenant. I find it amazing that the Fed gets a free pass in the media and from the political class on the subject of inequality.

For all the sturm and drang regarding how markets will react to a Trump presidency, bond traders appear to be relatively sanguine. Just like stocks have the VIX index which measures fear indirectly by tracking the price of options, bonds have an index too. And it is close to yearly lows.

Filed under: Economy, Morning Report | 40 Comments »