Stocks are higher this morning on no real news. Bonds and MBS are down.

The week ahead will have some important data on housing and inflation, with the Consumer Price Index on Tuesday, and the Producer Price Index on Thursday. We will also get housing starts and builder sentiment. Other important data points are retail sales, small business optimism and leading economic indicators.

Mr. Cooper reported fourth quarter numbers on Friday. Funded volume was $3.2 billion, a decrease of 39% QOQ and 82% compared to the fourth quarter of 2021. Servicing income kept the lights on, and Mr. Cooper is valuing its MSR portfolio more conservatively (at 5.1x) than many of the mortgage REITs which seem to have values from 5.5x – 6.1x.

Loan demand is falling, while lending standards are getting tighter, according to the Fed. This is typical for an economy that is poised to enter a recession. Loan demand for residential real estate was weak, and standards tightened for HELOCs, credit cards, auto loans and other consumer debt.

The Fed also observed the same phenomenon for commercial and industrial loans, as well as commercial real estate.

The Atlanta Fed GDP Now Index sees 2.1% GDP growth in Q1, while the Street sees it coming in mildly negative.

Stocks are lower this morning on no real news. Bonds and MBS are down.

Consumer sentiment rose in February, according to the University of Michigan Consumer Sentiment Survey. The strong jobs report last week probably contributed, however gasoline prices are a factor too. Unfortunately for those who want the Fed out of the way, inflationary expectations increased, rising to 4.2% from 3.9% in January. Longer-term inflationary expectations were steady at 2.9%. To put the current numbers into perspective, we are about 22% below the historical average since 1978.

Mortgage credit availability contracted slightly in January, according to the MBA. “Mortgage credit availability was essentially unchanged in January and remained close to its lowest level since 2013,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Similar to December 2022, the availability of credit has been driven lower by declining originations and shrinking industry capacity as lenders have streamlined their operations to cope with lower volumes. Additionally, as mortgage rates declined over the past month, the share of adjustable-rate mortgages has fallen – consistent with a slight pullback in ARM offerings in this month’s results. However, there has been a revival in mortgage application activity over the past month and our forecast is for rates to continue to decline and housing activity – including home sales and new home construction – to gradually pick up as we approach the spring homebuying season. These developments could potentially change the credit availability landscape in the months ahead.”

Rental growth grew only 2% in January, according to Redfin. This was the slowest increase in 20 months. “We’re watching closely to see whether rents start falling year over year. That would be a welcome relief for renters because it hasn’t happened since the onset of the pandemic,” said Redfin Chief Economist Daryl Fairweather. “If rents do start falling on a year-over-year basis, it will mean that renters have more room to negotiate. It may also prompt more landlords to sell their properties because they’re no longer getting a good return on their investment.”

There is a seasonal aspect to rental growth, which you can see in the chart above. Rents tend to bottom in January-February and then accelerate as the Spring Selling Season begins. It happened in 2020 and 2021, but not 2022. Historically, rents have lagged home price growth by 21 months, so we should probably see another pickup into the spring.

Stocks are up this morning on positive earnings. Bonds and MBS are up.

Initial Jobless Claims rose to 196,000 last week. This comports with the jobs report last Friday.

New York City is the most “rent-burdened” MSA out there, with people paying 69% of their income in rent. In order to NOT be considered rent-burdened, you have to make $177k. Other MSAs include Miami, Fort Lauderdale and Los Angeles.

Rithm Capital (aka New Rez) reported earnings yesterday. Mortgage origination volume fell 43% QOQ and 80% YOY to $7.9 billion. The company is guiding for Q123 volume to fall further to $5 – 7 billion. On the plus side, gain on sale margins rose 10 bp QOQ and 16 bp YOY to 1.81%. Funds available for distribution came in at $0.33, so the $0.25 dividend is well-covered at least for now.

The servicing portfolio has been the engine of growth, but it looks like they are valuing their portfolio pretty much fully at 4.9x servicing revenue.

Rithm is also building other businesses including single family rentals and its reno / construction / bridge loan businesses.

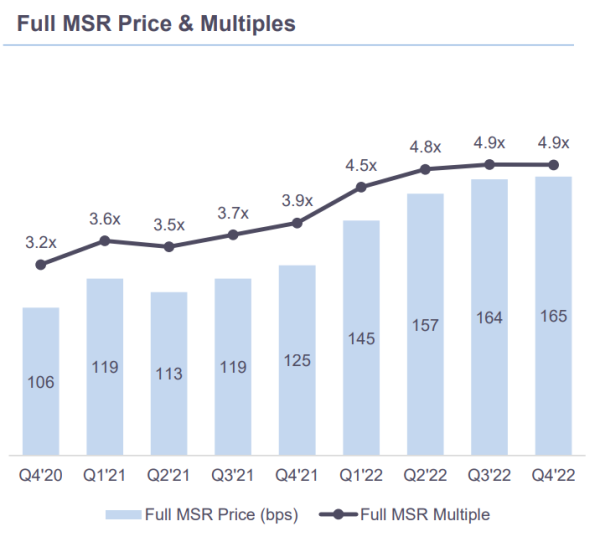

PennyMac Mortgage Investment Trust got beat up in the fourth quarter, as origination income fell. Note where they are valuing their servicing portfolio:

6.1 times is pretty hefty, and with their origination volume at 50% government, I wonder how much is FHA. Government servicing is not trading at 6 times. The MSR market is pretty well-supplied with originators selling their servicing portfolios to raise cash. I have to imagine the actual secondary market is well below that regardless of size.

Stocks are lower as investors continue to digest Jerome Powell’s comments yesterday. Hawks and doves both found something to seize upon. Bonds and MBS are up small.

We have 5 Fed speakers today, with Neel Kashkari (heavy hawk) speaking at 12:30.

Jerome Powell spoke yesterday, calling the US labor market “extraordinarily strong.” He did acknowledge that the disinflationary process has begun and we have seen progress on goods, however services remain high. It will take “not just this year but next year to get down to 2%,” the central bank’s inflation target, Powell said. And rates will have to remain at a restrictive level “for a period of time” before that happens, he noted. There has been an expectation that [inflation] will go away quickly and painlessly; I don’t think it’s guaranteed that’s the base case,” Powell said. “It will take some time.”

Jerome Powell talked with David Rubenstein and discussed the Fed’s plans to reduce the size of its balance sheet. Powell characterized it as passive reduction, which means it will let its portfolio mature and run off but not actively sell its holdings. While the Fed said it could consider sales of mortgage backed securities, it isn’t something that is being actively considered.

The Fed purchased its portfolio of mortgage backed securities when rates were extremely low, and liquidity is fickle in the MBS market. Unless a coupon is being actively originated, it won’t trade with any meaningful liquidity. The 3.5% coupons the Fed owns are trading well below par and the Fed would struggle to actually sell any of its holdings.

Mortgage applications rose 7.4% last week as purchases rose 4% and refis rose 18%. “Applications rose last week as the 30-year fixed mortgage rate inched lower to 6.18 percent, its fifth consecutive weekly decline. The 30-year fixed rate is almost a percentage point below its recent high of 7.16 percent in October 2022,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Both purchase and refinance applications increased last week and have shown gains in three of the past four weeks because of lower rates. Overall applications remained 58 percent lower than a year ago and rates are still significantly higher, however, this week’s results are a step in the right direction. Purchase activity that was put on hold last year due to the quick runup in rates is gradually coming back as rates ease and housing demand remains strong, driven by supportive demographics and the ongoing strength in the job market.”

Added Kan, “The average loan size on a purchase application increased to $428,500 – the largest average since May 2022. This increase is a sign that the recent upward trend in purchase activity remains skewed toward larger loan sizes and less first-time homebuyer activity, as entry level housing remains undersupplied, and buyers struggle with affordability in many markets.”

I talked about yield curve inversions and what they mean in a recent Substack article.

“The continued slowing of home prices at the end of 2022 reflects weaker housing market demand, primarily caused by higher mortgage rates and a more pessimistic economic outlook in general. But while prices continued to fall from November, the rate of decline was lower than that seen in the summer and still adds up to only a 3% cumulative drop in prices since last spring’s peak.

Some exurban regions that became increasingly popular during the COVID-19 pandemic saw prices jump and affordability erode at the time, but these areas are now seeing major corrections. And while price deceleration will likely persist into the spring of 2023, when the market will probably see some year-over-year declines, the recent decrease in mortgage rates has stimulated buyer demand and could result in a more optimistic homebuying season than many expected.”

I am accepting ads for this blog if you would like to make an announcement, highlight something your company is offering or want more visibility. I also offer white-label services which give you the ability to use this content for your own daily emails. Please feel free to reach out to nyitray@hotmail.com if you would like to discuss this further.

Stocks are flattish as we await Jerome Powell’s speech this afternoon. Bonds and MBS are down.

Neel Kashkari went on CNBC this morning to say that the Fed still had to raise rates “aggressively” in order to get inflation under control. The data “tells me that so far we’re not seeing much of an imprint of our tightening to date on the labor market. There’s some evidence that it’s having some effect, but it’s pretty muted so far,” Kashkari said. “I haven’t seen anything yet to lower my rate path, but I’m obviously keeping my eyes open and we’ll see how the data comes in,” he added. Neel Kashkari thinks the Fed Funds rate will have to rise to a range of 5.25% – 5.4% in order to cool off the labor market.

Rate locks saw an uptick in January as mortgage rates fell, according to the Black Knight Mortgage Monitor. “Based on our Optimal Blue rate lock data, we can see definite signs of a January uptick in purchase lending on lower rates and somewhat lower home prices,” said Graboske. “Indeed, locks on purchase mortgages soared 64% from the first through the fourth week in January. On the surface, it may seem the market has been stirred by a full point decline in interest rates and home prices coming off their peaks – but it’s not that simple. Yes, according to the Black Knight Home Price Index, December did see home values post their sixth consecutive monthly decline, and prices at the national level are now 5.3% off their June 2022 peaks. But affordability still has a stranglehold on much of the market, with the monthly mortgage payment on the average-priced home more than 40% higher than it was this time last year. It’s also important to keep January’s surge in purchase activity in perspective. While up, purchase locks were still running roughly 13% below pre-pandemic levels for the last full week of the month.

The affordability metric is (the monthly mortgage payment as a percentage of income) is above levels we saw during the bubble years, and compares to levels last seen in the early 1980s when the Fed took the Fed Funds rate into the teens to whip 1970s inflation.

In order to square the affordability circle either mortgage rates have to fall, home prices have to fall or wages have to increase. The problem is that we need a dramatic move in at least one of these to fix the issue. If mortgage rates fall somewhat and wages rise by 4%, we still have an affordability problem. Ultimately I think the lack of supply carries the day and homes stay unaffordable for the near term until homebuilding rebounds. And if you look at the big decreases in backlog reported by the builders (along with elevated cancellation rates) that doesn’t appear to be in the cards this year.

With home prices stabilizing or even falling, some financial “power buyers” are stuck holding the bag. These companies would bid for a property on behalf of a buyer and then sell the property to the buyer at the same price once they got a mortgage. The power buyer would earn a fee and the buyer would get to submit a non-contingent offer. Some of these buyers are now backing out of these deals because they can’t qualify for a mortgage at current rates. Ribbon, one of these power buyers is stuck with 400 homes and has been forced to cut 85% of its work force.

“There was sort of a power shift, from the power sitting with the seller knowing that their home is going to sell within a day, to the power sitting with the buyer,” said Tim Heyl, founder of the Austin-based power buyer Homeward Inc. Note the location. Goldman recently said that Austin could see a 2006-esque decrease in prices.

Given the track record of Zillow, OpenDoor and these power buyers, perhaps investing in real estate is harder than it looks, and a gee-whiz model to value real estate isn’t enough to crack the code.

Stocks are lower this morning as investors continue to digest the strong jobs report. Bonds and MBS are down.

The week after the jobs report is generally pretty data-light and next week is no exception. We have limited Fed-speak as well, and about the only thing remotely market-moving next week will be consumer sentiment on Friday.

The strong jobs report caused a more hawkish move in the Fed Funds futures. The march meeting is a lock for another 25 basis points, and there is a 73% chance for another 25 in May. Before the jobs report, investors saw a 40% chance of another hike this year. That said, the December futures see rates at the end of the year between 4.75% and 5%, which is 25 basis points higher than here.

The Wall Street Journal has an article about how housing has probably bottomed. We are seeing traffic increase and realtors are getting more calls. A big difference is that mortgage rates are now around 6% versus 7%+ in the fall of 2022. That said, homebuilders are still seeing outsized cancellation rates, and 2023 is expected to be another tough year for the sector.

One of the markets Goldman mentioned as vulnerable to a 2008-style decline was Austin, TX. The median home prices has fallen by 20% since June, but the rise in mortgage rates means that the median income required to buy that home has increased by 27%. Out-of-town buyers drove up prices beyond what the median income could support. We are seeing the same phenomenon in many Western MSAs like Boise, ID.

“The upside is that local first-time homebuyers finally have an opportunity; they’re no longer facing fierce competition from out-of-towners and investors,” Austin Redfin agent Maggie Ruiz said. “The downside is that 6% mortgage rates are still making homes unaffordable for many people. I’m advising buyers to negotiate with sellers on price and terms, consider buying down their mortgage rate and get into the market now if possible. As soon as rates drop, competition will be back.”

“I’m not seeing many local move-up buyers. Most Austin locals who already own their home are staying put because they don’t want to take on a higher mortgage rate,” she continued. “Some are capitalizing on higher home values, selling and relocating out of Texas to somewhere that’s still more affordable.”

Stocks are lower after the strong jobs report. Bonds and MBS are down

The economy added 517,000 jobs in January, which was way above expectations, while the unemployment rate inched down to 3.4%. The labor force participation rate the employment-population ratios were unchanged and remain below pre-pandemic levels. November and December payrolls were adjusted upward by 71,000.

Leisure and hospitality added the most jobs (+128,000) however employment in this sector remains below pre-pandemic levels. Professional and business services and health care were also big contributors to job growth. Average hourly earnings rose 0.3% month-over-month and 4.4% year-over-year.

The growth rate in average hourly earnings is declining, however we are still above pre-pandemic levels.

Needless to say, this report will be too strong for the Fed’s liking. This explains the reaction of stocks and bonds to the report. The Fed wants to cool the labor market and so far it hasn’t gained any traction. The unemployment rate has broken below pre-pandemic levels and is now back at the lowest in over 50 years.

PennyMac Financial Services reported that origination volumes in the fourth quarter were $23 billion, down 12% from Q3 and 41% from a year ago. For the year, PFSI originated $109 billion, which was down 54% compared to 2021. In terms of profitability, servicing carried the load, offsetting the losses in the production segment.

Production margins fell to 55 basis points from 99 in Q3 and 119 basis points a year ago. The decline in margins was driven primarily by origination mix – consumer direct fell dramatically while correspondent remained stable. Delinquency rates ticked up again, but remain below pre-pandemic levels.

The ISM Services Index rebounded in January after contracting in December.“Business Survey Committee respondents indicated that capacity and logistics performance continue to improve. Although responses varied by industry and company, the majority of panelists indicated that business is trending in a positive direction. Employment was unchanged for the month. Some companies still find it difficult to fill open positions, while others are facilitating staff reductions.”

I am accepting ads for this blog if you would like to make an announcement, highlight something your company is offering or want more visibility. I also offer white-label services which give you the ability to use this content for your own daily emails. Please feel free to reach out to nyitray@hotmail.com if you would like to discuss this further.

Stocks are higher this morning as markets digest the Fed’s move yesterday. Bonds and MBS are up.

As expected, the Fed hiked the Fed Funds rate by 25 basis points yesterday. The vote was unanimous and raised the target range to 4.5%-4.75%. They signaled that the tightening cycle is not done: “The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”

Stocks and bonds loved the announcement, with the 10-year bond yield falling 9 basis points in the immediate aftermath of the announcement, while the S&P 500 tacked on close to 100 points. Jerome Powell acknowledged that inflation has moderated but stressed the need to stay the course.

The Fed Funds futures currently see a 85% chance of another 25 basis point hike in March, with 15% handicapping no change in policy. The markets see a 30% chance of another 25 basis point hike at the May meeting. The yield curve continues to invert, with the 2s-10s spread at -71 basis points.

The ECB also hiked rates 50 basis points this morning, which is kicking off a furious rally in European sovereign yields. The German Bund yield is down 17 basis points, while UK Gilt yields are down 21 basis points. Global sovereign market tend to correlate pretty closely, so this provides further impetus for lower rates.

Nonfarm productivity increased 3% in the fourth quarter of 2022, which was above Street expectations. Output increased 3.5% while hours worked rose 0.5%. Unit labor costs rose 1.1% as compensation rose 4.5% and productivity rose 3%. During 2022, nonfarm productivity fell 1.3%, which was the worst annual reading since 1974. Declining productivity and inflation go hand-in-hand.

This number will almost certainly push the Fed towards a tighter monetary policy since it largely feeds into the services ex-housing component of inflation which is wage growth. Higher compensation without a corresponding increase in output = lower productivity and higher inflation overall.

Job cuts increased substantially in January, according to outplacement firm Challenger, Gray and Christmas. U.S. based employers announced 102,943 job cuts in January, compared to 43,651 in December and 19,064 a year ago. Tech companies have made lots of announcements and many over-hired during the pandemic years. “We’re now on the other side of the hiring frenzy of the pandemic years,” said Andrew Challenger, labor expert and Senior Vice President of Challenger, Gray & Christmas, Inc. “Companies are preparing for an economic slowdown, cutting workers and slowing hiring,” he added. Tech and retailers accounted for the bulk of the job cuts. Where are companies hiring? Entertainment and Leisure.

Despite the numbers from Challenger, initial jobless claims remain exceptionally low, coming in at 183,000 last week.

Pulte Homes announced fourth quarter earnings, with a 20% increase in revenues and a 200 basis point increase in gross margin. The increase in gross margin means that Pulte hasn’t been forced to grant concessions to move the inventory. That said, these Q4 sales were initiated earlier in 2022 before mortgage rates spiked.

Orders were down 41%, which reflects an elevated cancellation rate of 32%. Interestingly, the stock market is looking over the homebuilding valley. The homebuilder ETF (XHB) is up 29% over the past 3 months.

Stocks are lower as we await the Fed decision at 2:00 pm. Bonds and MBS are up.

The Fed decision is scheduled for 2:00 pm and there will be a press conference afterward. The expectation is for 25 basis points, and the markets will be looking for language in the press release indicating that the Fed is wrapping up its tightening cycle.

The economy added 106,000 jobs in January, according to the ADP Employment Survey. This was lower than the consensus estimate of 158,000 and the 185,000 forecast for Friday’s jobs report. It sounds like there was some sort of weather-related impact which depressed the number.

Leisure and hospitality accounted for 95,000 of the job gains, followed by finance and manufacturing. Trade / Transportation / Utilities and construction saw declines in employment. I suspect a lot of the jobs losses in trade / transportation / utilities were Amazon.com related as they over-committed to space and employment during the pandemic.

Pay growth was 7.3% for job stayers and 15.4% for job changers. Leisure and hospitality saw increases of 10% and was the outlier compared to all the other sectors which were bunched between 6.6% and 7.9%. This is something that will bother the Fed, as “services ex-housing” is their target for inflation reduction. The youngest cohort (ages 16-24) saw the biggest increase as well.

Mortgage applications fell 9% last week as purchases fell 10% and refis fell 7%. “Mortgage rates declined for the fourth straight week and have now fallen almost 40 basis points over the past month. Treasury yields were higher on average last week, while mortgage rates decreased, which was a sign of a narrowing spread between the two,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “The spread between mortgage rates and the 10-year Treasury has been abnormally wide since early 2022. Further narrowing of that spread is expected to put downward pressure on mortgage rates in the coming months. Overall application activity declined last week despite lower rates, which is an indication of the still volatile time of the year for housing activity. Purchase activity is expected to pick up as the spring homebuying season gets underway, bolstered by lower rates and moderating home-price growth. Both trends will help some buyers regain purchasing power.”

Joel Kan’s point about the difference between mortgage rates and Treasury rates is important. This gets into the whole esoteric discussion of MBS spreads, which can get complicated quickly. We did get some info on MBS spreads yesterday courtesy of AGNC Investment, a mortgage REIT which announced its fourth quarter results.

Mortgage REITs invest in mortgage backed securities, and they are often the buyer of the Fannie / Freddie securitizations. Think of them as the ultimate “lender” for your production. For the past year, the mortgage REITs have been reporting declines in book value per share as MBS spreads have widened – in other words MBS have fallen in value with interest rates, and the hedges mortgage REITs use have not increased in value enough to make up for the losses. This looks like it finally reversed in the fourth quarter. You can see it in the highlighted row below.

This spread increased significantly in 2022, which has exacerbated the increase in mortgage rates from 3.27% to 6.66%. Note I did a deep dive on MBS spreads in a Substack piece recently.

I am accepting ads for this blog if you would like to make an announcement, highlight something your company is offering or want more visibility. I also offer white-label services which give you the ability to use this content for your own daily emails. Please feel free to reach out to nyitray@hotmail.com if you would like to discuss this further.