Vital Statistics:

| Last | Change | |

| S&P futures | 4,237 | 2.8 |

| Oil (WTI) | 72.32 | 0.24 |

| 10 year government bond yield | 1.49% | |

| 30 year fixed rate mortgage | 3.14% |

Stocks are flat as we await the FOMC decision. Bonds and MBS are flat.

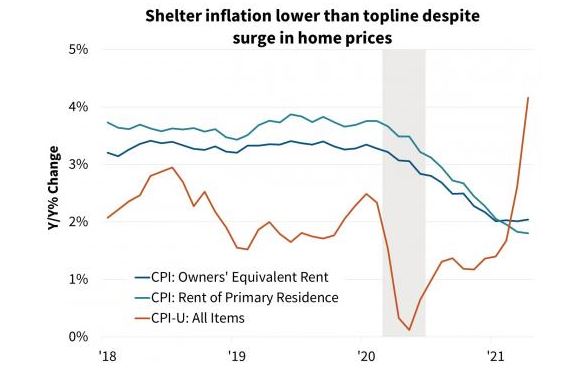

The FOMC decision will be released at noon today. The markets will be listening for language pointing towards an end of MBS and Treasury purchases as well as the dot plot. I also think markets will be sensitive to how the Fed describes the state of the economy. Finally, I hope they discuss what is driving the current labor shortage and offer up a reasonable explanation for it.

Speaking of disappointing economic data, housing starts came in below expectations. Starts came in at 1.57 million, while permits came in at 1.68 million. Starts were more or less flat with April, while permits showed a small uptick. Labor and materials shortages are probably behind the disappointing numbers. That said, homebuilder sentiment remains elevated, despite challenges with input costs and labor.

Mortgage applications rose 4.2% last week as purchases increased 2% and refis rose 6%. Rates have been coming back down, which is increasing refi opportunities. “U.S. Treasury yields have slid because of the uncertainty in the financial markets regarding inflation and how the Federal Reserve may act over the next few months,” said Joel Kan, MBA Associate Vice President of Economic and Industry Forecasting. “Purchase activity also rebounded, even as supply constraints continue to slow the housing market. An almost 5 percent increase in government purchase applications drove most of last week’s gain while also tempering the recent growth in loan sizes. Purchase applications were still down 17 percent from a year ago, which was when the mortgage market started seeing large post-shutdown increases in activity.”

Note that NAR believes we have a 5.5 million unit gap in housing demand versus supply.

Mortgage credit availability rose in May, according to the MBA. “Mortgage credit availability in May increased to its highest level since near the start of the pandemic, but still remained at 2014 levels. The increase was driven by a 3 percent gain in the conventional segment of the market, with a rise in the supply of ARMs and cash-out refinances. This is consistent with the uptick in mortgage rates and a slowing refinance market, as well as MBA’s Weekly Applications Survey data showing increased interest in ARMs,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting. “The jumbo index jumped 5 percent last month, but even with increases over the past two months, the index is still around half of where it was in February 2020. A rapidly improving economy and job market has freed up jumbo credit, as banks have deposits to utilize. However, there is still plenty of restraint, as many sectors have not fully returned to pre-pandemic capacity, and there are around 2 million borrowers still in forbearance.”

Filed under: Economy, Morning Report | 58 Comments »