Vital Statistics:

| Last | Change | |

| S&P Futures | 2180.0 | 3.0 |

| Eurostoxx Index | 344.3 | 4.0 |

| Oil (WTI) | 42.6 | -0.2 |

| US dollar index | 86.0 | -0.2 |

| 10 Year Govt Bond Yield | 1.51% | |

| Current Coupon Fannie Mae TBA | 103.8 | |

| Current Coupon Ginnie Mae TBA | 105.2 | |

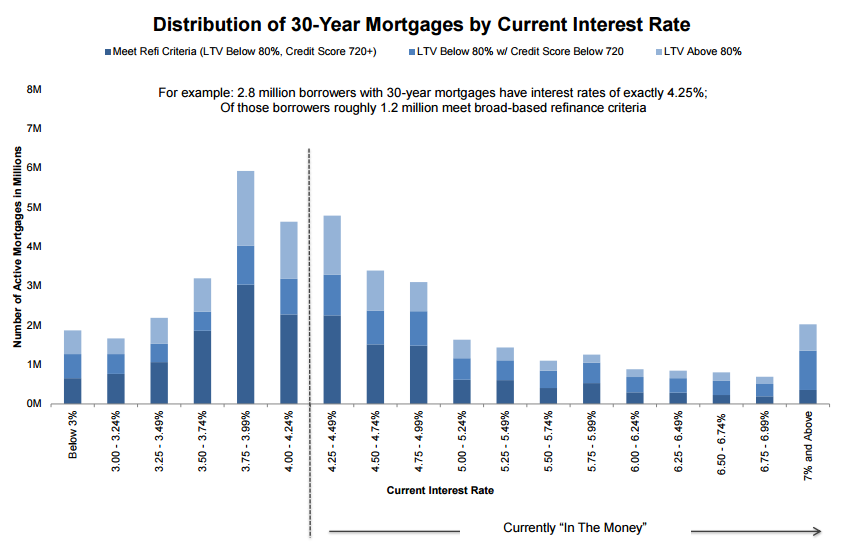

| 30 Year Fixed Rate Mortgage | 3.52 |

Markets are up this morning on no real news. Bonds and MBS are rallying

Bond markets worldwide are rallying after the Bank of England tried to buy Gilts as part of its QE program and had a tough time finding sellers.

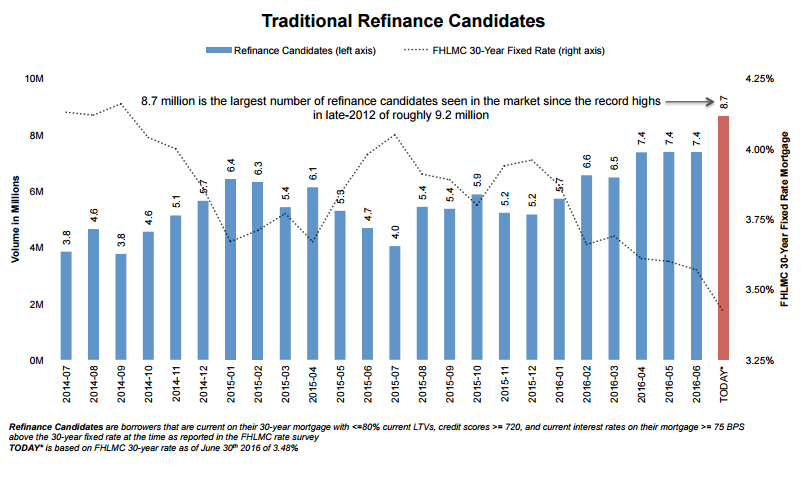

Mortgage applications rose 7% last week as purchases rose 3% and refis rose 10%.

Job openings were unchanged in June, at 5.6 million. The quits rate at 2% was more or less unchanged. This number is the tell for a strengthening labor market.

The bond market has given back the losses from the strong payrolls report last Friday. The Fed Funds futures markets are pricing in a 45% chance of another rate hike this year. Meanwhile, global bond yields continue to fall, with the German Bund at -9 basis points.

Affordable starter homes are becoming scarce in many parts of the country. We are seeing bidding wars in the hotter markets. Low housing starts are playing a factor here, and government regulation is a big driver of that. Mandates that increase the cost of construction make starter homes too expensive for an entry-level income.

Technology is helping drive down realtor commissions, according to Redfin. Of course Redfin is talking its own book, however many sellers are foregoing the use of an agent, especially at the higher price points, which makes sense.

Filed under: Economy, Morning Report | 28 Comments »