Posted on May 13, 2016 by Brent Nyitray

Stocks are lower this morning on no real news. Bonds and MBS are up small.

Retail Sales increased 1.3% month-over-month, topping Wall Street forecasts. Autos, grocery and online led the charge. Ex-autos, gas and building materials, it increased 0.9%. We have had a laundry list of retailers miss earnings lately (Macy’s, JC Penney, Kohls, Nordstrom), so investors were probably expecting the worst. Given all of the weak economic data lately, this is one decent data point. We are seeing some sell-side firms take up Q2 GDP estimates on the number.

The chart below is retail sales as a percentage of GDP. It is not a seasonally adjusted number, so holiday spending accounts for the spikes. However, you can see that post the real estate crash, retail sales have been a much smaller percentage of GDP than they were for the 90s and the bubble years. Perhaps spending during the 90s and the bubble years was driven by the cash-out refi and now that is gone. If so, that would certainly help explain why growth has been so tepid. Or it simply means the Great American Deleveraging Process has further to go.

Inflation at the wholesale level remains well below the Fed’s target. The Producer Price Index rose 0.2% in April and is up 0.9% year-over-year.

Business inventories climbed 0.4% in March, while consumer sentiment jumped.

Janet Yellen doesn’t rule out the possibility of negative interest rates, however they would be a last resort.

The National Association of Homebuilders estimates that 14 million people are priced out of the housing market due to government regulation.

Filed under: Economy, Morning Report | 48 Comments »

Posted on May 12, 2016 by Brent Nyitray

Markets are higher this morning as commodities rally and the UK central bank maintained interest rates. Bonds and MBS are down small.

Mortgage delinquencies were flat at 4.77% in the first quarter, according to the MBA. The foreclosure percentage fell to 1.74% from 1.77%. We are back to pre-crisis levels in delinquencies.

Initial Jobless Claims rose by 20k to 294 last week, the highest level in over a year. We are seeing more and more evidence that the US economy might be slowing a little.

The other evidence of a slowdown? Lousy earnings from the retailers. Macy’s got slammed by 15% yesterday on lousy numbers. Today’s victim is Kohls, down over 7%.

Consumer comfort slipped to 41.7 from 42, according to the Bloomberg Consumer Comfort Index.

Interesting article on the dynamic that is driving long term yields lower: Right now, there is about $9 trillion worth of government bonds out there with negative yields. This is pushing investors to buy longer-dated stuff in order to get a positive yield. Japan recently sold 30 year bonds at a yield of 31.9 basis points, which makes sense given that everything with maturities of 15 years or less is negative. Spain sold 50 year bonds and Italy is exploring a 50 year bond sale. Given the strong US dollar, and the 10 year’s yield of 1.75%, any slowdown in the US economy should result in tremendous demand for US treasuries. Which means low mortgage rates are probably here to stay. Also, it looks like the slowdown in US corporate issuance is over.

Import prices rose 0.3% on a month over month basis, but are down 5.7% year-over-year. Yet another indication that inflation is going nowhere.

Interesting article on the new hard money lenders in the WSJ. (Behind the paywall unfortunately). They are lending money in the high single digits. There seems to be an arbitrage between underwriting and the box that bank mortgages will fit in. In other words, banks will decline a loan for a technical reason, which makes the loan unsaleable. These people look beyond that and decide if the risk is worth taking. If the rate is 10%, they might be getting compensated for that risk.

Filed under: Economy, Morning Report | 11 Comments »

Posted on May 11, 2016 by Brent Nyitray

Stocks are lower this morning on no real news. Bonds and MBS are flat.

Slow news day, with no economic data

Mortgage Applications rose 0.4% last week as purchases rose 0.4% and refis rose 0.5%. Refis accounted for 52.8% of all originations.

Bernie Sanders and Donald Trump won their respective primaries in West Virginia yesterday. Hillary looks to have sewn up the Democratic primary, despite Bernie Sanders’s determination to play it out. Neither Trump nor Hillary are especially popular in their respective parties. 2016 could be the year of the third party candidate, with Sanders supporters going for Green Party candidate Jill Stein and establishment GOP voters siding with Libertarian candidate Gary Johnson.

Stonegate Mortgage announced earnings yesterday, missing estimates on both the top line and the bottom line. Originations decreased by 15%, while the company took a $36 million writedown of its MSR portfolio. The write-down lowered revenues to $5 million from $47 million at the end of the fourth quarter. Originations decreased 15% to $1.94 billion sequentially and fell 26% on a YOY basis. The stock is trading at $4.16 early, down 28% in May alone.

Filed under: Economy, Morning Report | 22 Comments »

Posted on May 10, 2016 by Brent Nyitray

Stocks are higher this morning as commodities rally. Bonds and MBS are flat.

Why are markets looking at commodity prices? Because we have an enormous speculative bubble in commodities unraveling in China. As China deflates its many bubbles (including residential real estate), the reverberations will be felt in developing markets as China looks to export its way out. The deflationary impulse emanating from China threatens to send the European markets (who are closer to the edge than we are) into a Japanese-esque deflationary spiral. The German 10 year Bund yields 12 basis points, and is pushing towards its lows. The net effect to the US? Pain in the high end of the real estate market (think Seattle, San Francisco, Manhattan), and lower Treasury yields.

Speaking of Treasury yields, Citi is out with a call of 1.5% on the 10-year.

Despite a dovish bent, and a call to let the labor market run hot, Minneapolis Fed President Neel Kashkari still says 2 more rate hikes this year is a “reasonable expectation.”

Small business optimism increased slightly in April, according to the NFIB. The index rose about a point to 93.6, still well below its long term average of 98 and below the post-recession peak of 100 set in 2014. While the political climate is certainly not helping, small business is becoming more pessimistic about the economy, which certainly is consistent with the weakening economic data. The conundrum continues to be the labor force, where we have enormous slack, yet businesses talk about an inability to find qualified applicants. Will there be a bidding war for the current people in the labor force (and thus wage inflation), or will businesses decide to hire and train people who don’t quite fit what they are looking for? That dynamic will determine how fast the Fed moves to hike rates.

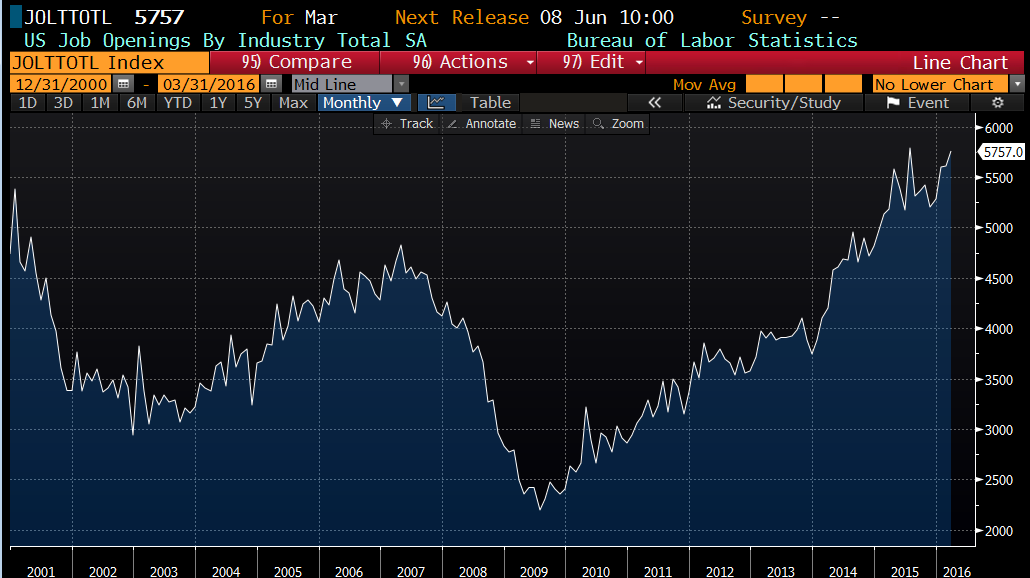

Job openings are higher than they were in 2000, according to the latest JOLTS data. Last month, job openings increased to 5.8 million, just under the high set in July last year. You can see in the chart below how job openings have looked since the index began in the year 2000.

That said, the job openings data might not be the best snapshot of the state of the labor market. The quits rate is a much better barometer of the health of the labor market. The quits rate was flat in March, and is still heading higher, but has not eclipsed the pre-recession highs.

Wholesale inventories increased by 0.1%, while sales rose 0.7%. We still have an inventory problem in the economy however, and that is one signal that is pointing towards a downturn this year. The inventory to sales ratio is at 1.36, which is pushing towards the highs experienced during the Great Recession.

Fannie Mae is launching a no-FICO product for people who don’t have credit scores. The loan will price out as if your credit score is 620. Proof of payment of your rent and some other bill will suffice. They will go to 90 LTV for purchase and no cash-out refis. The down payment is gift-able. However, for the very young borrower who has yet to establish a track record, this could be a way in.

Filed under: Economy, Morning Report | 13 Comments »

Posted on May 9, 2016 by Brent Nyitray

Markets are up small despite some bad data out of China overnight. Bonds and MBS are up small.

- Payrolls + 160k

- Unemployment rate 5%

- Average hourly earnings + 0.3% MOM / +2.5% YOY

- Labor force participation rate 62.8%

- Underemployment rate 9.7%

Overall not a great report. The Labor Force Participation rate fell back, which is bad news for the economy overall. Earnings are up, which is about the only bright spot on the report. Strategists are beginning to worry about a deceleration in the economy, or even a mild recession. Tough to see how the Fed raises rates in June.

The Labor Market Conditions Index improved to -.09 from -2.1 last month. This is a meta-index of several leading and lagging indicators.

Despite the weakness in the economy, Bill Gross and Mohammed El Arian are warning investors not to discount the Fed. Their point: wage growth is the most important part of that jobs report, and they are going up. A June hike is not the most likely outcome, however it shouldn’t be ruled out either.

The Fed wants to see a bit of inflation, but the convoy system in Asia is preventing it. Like the Japanese, China is propping up unprofitable factories, which is contributing to a glut of aluminum, steel, and other industrial goods. We saw this happen in the 1930s, which triggered trade wars and exacerbated a global deflationary vortex. We are seeing a similar thing today, with the backlash against free trade, and nationalistic candidates in Europe and the US.

The biggest internet lender, Lending Club, is down big pre-open after the CEO resigned over a loan sale. Apparently the loan sale didn’t have anything to do with pricing or credit, but it did violate the company’s internal procedures. The company is currently facing trouble funding its loans in the capital markets. The stock is down close to $5 a share after trading at $19.50 just under a year ago.

This year has not been kind to the stocks of non-bank lenders / servicers – Nationstar, Ocwen, Stonegate, Walters all down badly this year.

Filed under: Economy, Morning Report | 33 Comments »

Posted on May 6, 2016 by markinaustin

05/06/2016

Total nonfarm payroll employment increased by 160,000 in April, and the unemployment rate was unchanged at 5.0 percent. Employment increased in professional and business services, health care, and financial activities. Job losses continued in mining.

Filed under: Economic data, Open Thread | 20 Comments »

Posted on May 5, 2016 by Brent Nyitray

Markets are flattish this morning on no real news. Bonds and MBS are flat as well

Announced job cuts increased 5.8% in April, according to outplacement firm Challenger, Gray and Christmas. Layoffs are at a 7 year high, driven primarily by pain in the energy sector, but also in retail and computers (Intel accounted for 17k of them). Remember, these are announced job cuts – they often either don’t end up materializing or are accomplished by attrition.

We still aren’t seeing evidence of mass layoffs in the initial jobless claims numbers, which are hovering around 40 year lows. Last week, they increased to 274k.

Consumer comfort fell last week. Increasing gasoline prices aren’t helping.

Mortgage credit availability decreased in April, according to the MBA. Lynn Fisher, MBA’s Vice President of Research and Economics commented, “Mortgage credit became less available in April as a result of two opposing trends, resulting in a net decrease to the index. Investors continued to roll out Fannie Mae and Freddie Mac’s low down payment loan programs, which had a loosening effect on credit availability. However, this was more than offset by tightening among high balance and jumbo loan programs.”

Filed under: Economy, Morning Report | 32 Comments »

Posted on May 4, 2016 by Brent Nyitray

Markets are down this morning after some disappointing economic data. Bonds and MBS are flat.

We got some lousy employment / labor data this morning, starting with the ADP jobs report, which shows the economy added 156k jobs last month. The Street was looking for 195k, so this is a big miss. Friday’s jobs number is expected to come in around 200k.

Nonfarm productivity fell 1% last quarter, while unit labor costs increased 4.4%. On an annualized basis, productivity has been negative 3 out of the last 4 years. The back-to-back drop is the lowest since 1993. Firms are hiring workers, but uncertainty over the economy is holding back capital expenditures. Unit labor costs increased 4.1% last quarter. This in part might explain why profits this quarter have been weak so far.

Mortgage Applications fell 3.4% last week as purchases fell 0.1% and refis fell 5.5%.

In other economic news, the service economy continued to expand, with the ISM Non-Manufacturing index improving to 55.7. Durable Goods orders rose 0.8%, but fell 0.2% if you strip out transportation. Factory orders rose 1.1%, while capital goods orders ex defense and aircraft (a proxy for business capital expenditures) rose 0.5%. So a mixed bag overall.

Ted Cruz dropped out of the presidential race last night, paving the way for Donald Trump to be the nominee, unless the party decides to rally around John Kasich at a contested convention. If Gary Johnson were a stock, he would be a screaming buy at the moment.

We have seen an uptick in the labor force participation rate over the past few months from lows not seen since the 1970s. What is going on? While the hope is that a hot labor market will draw the long-term unemployed back into the labor force, what is really going on is that fewer people are leaving. You can see this borne out in the initial jobless claims data, which is the lowest going back to 1973. People who have jobs are keeping them. For the Fed, this creates a bit of a conundrum. They want more people to re-enter the workforce, but if business has to compete for the current labor pool by increasing wages, the Fed will have to put the brakes on the economy sooner than they would like.

Filed under: Economy, Morning Report | 19 Comments »

Posted on May 3, 2016 by Brent Nyitray

Stocks are lower this morning on global economic weakness. Bonds and MBS are up.

Sell in May and go away? Certainly that is the tone of the market so far.

Not much in the way of economic numbers this morning. The ISM New York Index rose while the IBD/TIPP Economic Optimism index ticked up as well. Vehicle sales will be trickling in all day as well.

Walter Investment Management is getting pummeled this morning on bad numbers. Tangible book value per share fell from $9.92 to $5.04 on a negative MSR valuation mark. Reverse Mortgages also hurt earnings. Nationstar and Ocwen are down in sympathy. The stock is down 27% to $5.25 a share. This was a $23 stock last summer.

Atlanta Fed President Dennis Lockhart said the markets are underestimating the possibility of a rate hike at the June meeting. Currently the Fed Funds futures market are handicapping a 10% chance of a rate hike. Kind of surprising given that GDP growth in the first quarter was a measly 0.5% and the latest forecasts for Q2 GDP are coming in around 1%. The possible exit of the UK from the Eurozone is another risk. Ultimately it will all come down to wage growth (or the lack thereof).

Construction spending rose 0.3% MOM and is up 8% YOY. Residential construction was up 7.6% YOY. Office, commercial, and health care were where the action was, increasing close to 20% overall.

Home prices increased 6.7% last year, according to Corelogic. They are forecasting a 5.3% increase this year. Restricted supply continues to drive prices higher, although affordability is falling. Lower interest rates are helping with the affordability issue,

Banks eased standards for residential mortgages in the first quarter, according to the Fed Senior Loan Officer Survey. Conforming loans, non-QM and jumbo loans eased standards.

Filed under: Economy, Morning Report | 23 Comments »

Posted on May 2, 2016 by markinaustin

http://www.economist.com/news/united-states/21697826-how-cost-benefit-analysis-might-save-americas-criminal-justice-system-when-economists-turn

It seems that prison reform, especially reduction of incarcerations, is widely agreed to be a worthy goal.

In passing, we read here that prison costs Americans $80B annually, that 1/5th of the world’s prison population is in the USA, and 70M Americans have criminal records.

Filed under: Open Thread, prisons | 20 Comments »