Happy Friday the 13th.

Markets are higher this morning on optimism of a deal in Greece and encouraging economic data out of Germany. The Greek 10 year yield is down almost 100 basis points this morning and is approaching 9%. The market has a risk-on feel with stocks up and bonds / MBS down.

Import prices fell 2.8% MOM and 8% YOY. Consumer sentiment fell from 98.1 to 93.7.

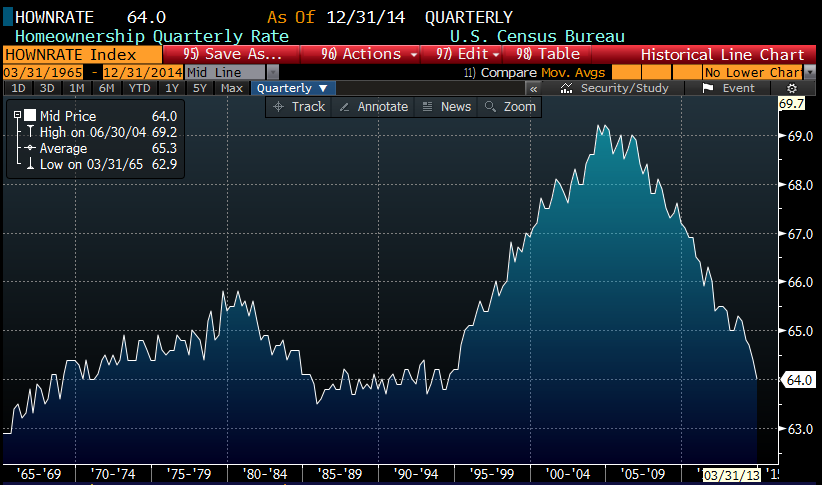

Bloomberg has a good piece on Mel Watt and the issues surrounding principal mods for Fan and Fred loans. The biggest question remains: how can you help underwater homeowners without triggering a wave of strategic defaults? 85% – 90% of people whose mortgage is underwater are current on their payments. The last thing you want to do is encourage them to stop paying in order to get a principal mod. Luckily, time has been doing the heavy lifting here, as the number of homes with negative equity has fallen from 31% in 2012 to just about 17% today. Second, many of those homes are not Fan and Fred loans in the first place, and FHFA is only looking at cutting principal on Fan and Fred loans that it owns. The FHFA Home Price Index, which tracks the prices of homes with a conforming mortgage is within 5% of the peak.

Bob Shiller warns of a bond bubble. He is probably right, although it could last some time. Interest rate cycles are long: the current cycle began in 1981 or so. Note that in the 1950s, the bond market crashed and the generation that lost their shirts in the stock market crash of 1929 ended up blowing up in levered flattening trades. Persistently low interest rates can wreak all sorts of havoc, especially with pension funds and insurance companies. They have a return bogey they must meet, and the actuarial tables couldn’t care less that interest rates are zero. Note that Dr. Cowbell is copacetic with all of this. Note that the 4 most dangerous words in investing are: This Time Is Different.

Bill Ackman sees the common stock of Fannie Mae and Freddie Mac as “the best trade in capital markets” He is betting that Congress will eventually stop taking all of Fannie’s profits and allow them to recapitalize in private markets. The thing is, this is a litigation lottery ticket. It is either worth a lot, or worth nothing. If it actually had access to its profits – it doesn’t – all p/l goes to Treasury – it would have a P/E of 1. FWIW, the Administration is bound and determined to see that Fannie Mae common shareholders do not see a dime. But administrations could change, and Congress may decide that housing reform is simply too tough and we go back to the old F&F.

How bad are things in the energy patch? We have another arctic blast hitting the Eastern part of the country and natural gas cannot get out of its own way. Kind of amazing, really.

Filed under: Morning Report | 31 Comments »