Posted on December 16, 2014 by Brent Nyitray

Stocks are lower as oil continues to fall. Bonds and MBS are rallying hard.

Euro yields are continuing to move lower. The German Bund is currently trading at 57.6 basis points. It began the year at close to 2%. Think about that for a moment. FWIW, the trader in me is starting to think about a capitulation low in rates. Which means we are ripe for a snap-back in yields. LOs, I know this is a dead period of the year, but there might be some refis to be had with the us 10 year yield falling towards 2%. I don’t know how long this gift lasts.

Another observation is that we are getting close (40 basis points or so) to the lows set before the the Fed hinted that QE was ending. If we are getting this sort of movement in rates without QE, it does beg the question of whether QE was effective in the first place.

The Russian Ruble fell to a record low as the Russian Central Bank raised interest rates to 17%. The ruble has been slammed by a combination of low oil prices and international sanctions over Ukraine. The last stop is capital controls. The swoon in oil prices has hit Russia and Venezuela particularly hard.

Housing starts fell to 1028k in November from an upward revised 1045k. Building Permits fell from 1092k to 1035k. For once it was single fam that accounted for most of the decline – multi-fam actually rose. Note that weather may have affected the numbers as winter storms arrived early this year for the upper Midwest and New England.

The FOMC meeting begins today. The decision will be released tomorrow at 2:00 pm.

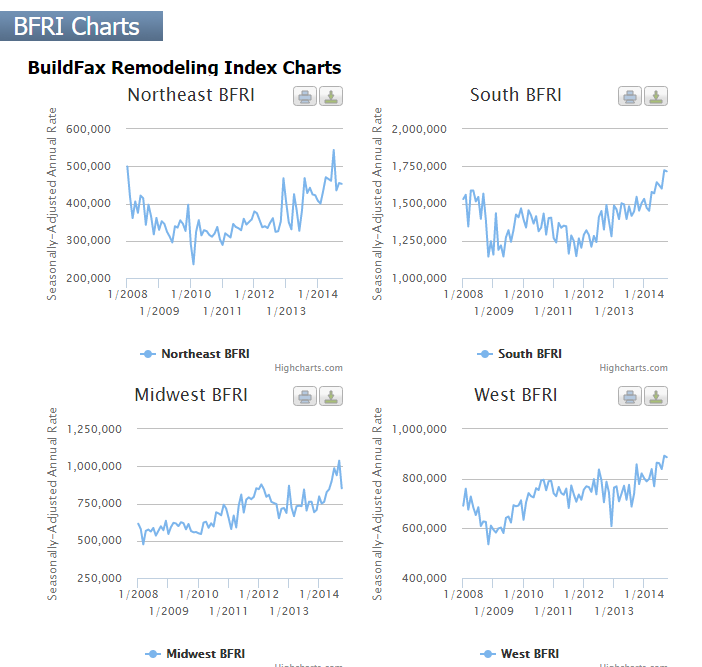

The Buildfax remodeling rate came in at just under 4 million, which is 4% below September and is 10% higher than a year ago. Activity continues to be strongest in the South and West, with the Midwest and Northeast lagging.

Filed under: Morning Report | 22 Comments »

Posted on December 15, 2014 by Brent Nyitray

Markets are higher this morning after stocks got slammed in Asia last night. Bonds and MBS are down.

The NAHB Homebuilder Sentiment Index fell to 57 in December. Sentiment is still on the strong side, although the Street was clearly spooked by Toll’s numbers last week.

Wall Street is betting that inflation will remain dead for a long time. Treasury Strips are back (which basically slices and dices a long term Treasury into a bunch of zero coupon bullet bonds). This strategy has been a winner this year, rallying almost 50%. Foreign bond investors have had a great year with the the currency and bond markets posting big gains. The thing to remember is that US investors aren’t the only ones who play the Treasury market – and foreign bond investors are often looking at their domestic bond markets and finding more value in the US. To put this in perspective – the US 10 year yields 2.12%. The German Bund (10 year) yields 64 basis points. The Japanese JGB (another 10 year) yields under 38 basis points. The Spanish 10 year yields 1.79%. There is a global relative value trade happening here.

Strategists have gotten the bond market wrong all year. This is a case where the textbook response – sell Treasuries as the economy improves – has been dead wrong, overwhelmed by events overseas. Keep this in mind when thinking about rates in the US – strong data might not be enough to push bonds lower and originators might be getting a gift here. It won’t last, and the snap-back could be vicious. Second, anyone buying a 30 year zero at 43 which yields 2.86% should have their head examined. This is bubble behavior, and is the bond market equivalent of buying Cisco Systems at 70 (or 132x earnings) in 2000. Bonds will crack at some point, but keep in mind that bond market cycles are long.

Speaking of strong economic data, Industrial Production rose 1.3% in November and capacity utilization topped 80% for the first time since March of 2008. This production number was the highest since 2010. On the other side of the coin, the December Empire Manufacturing Index fell in December.

The FOMC meets this week, and the decision will be released Wednesday at 2:00 pm EST. This one should have a press conference, along with updated economic projections and a press conference. The focus is on the timing of rate hikes, and investors will key in on language regarding the labor market.

In the budget deal last week, some regulations were relaxed for the big Wall Street banks, particularly the provision requiring derivatives to be housed in an entity without recourse to the parent FDIC – insured bank. This sparked a big rebellion on the left, but it ended up going nowhere. FDIC insured banks may now use credit default swaps as hedging instruments for their own books. To hear the left tell the story, this basically returns us back to the bad old days of 2005. To the industry, this is a common-sense relaxation of a rule that went too far in the first place. That said, banks were always allowed to use these products, but had to post more collateral than they wanted to. This is a knotty question, as many “hedges” are really speculative bets when you delve into the details. I suspect JP Morgan’s 2012 London Whale trading loss was intended to act as a hedge in the first place.

Finally, there was a bit of dishing on this place in PL yesterday…

Filed under: Morning Report | 30 Comments »

Posted on December 12, 2014 by Brent Nyitray

Markets are lower this morning as oil continues to fall. Bonds and MBS are up, with the 10 year hitting lows not seen since June of 2013.

Lower energy prices means that inflation at the wholesale level is pretty much non-existent. The producer price index fell .2% in November. Ex food and energy, it was flat.

Declining gas prices pushed the University of Michigan Consumer Confidence level to 93.8 from 88.8 last month. We appear to be back to normalcy.

The left is still up in arms over the language in the CROmnibus (continuing resolution + omnibus spending bill) that allows banks to trade derivatives in their FDIC insured entity. I haven’t seen the specific language, but I think it allows the banks to use derivatives for hedging purposes. But there is so much posturing going on here that it is hard to tell exactly what it does. The spending bill did make it through the House, and it looks like a done deal in the Senate.

Filed under: Morning Report | 22 Comments »

Posted on December 11, 2014 by Brent Nyitray

Stocks are higher this morning after initial jobless claims and retail sales surprised tot he upside. Bonds and MBS are flat.

Initial Jobless Claims fell slightly to 294k last week. We have been consistently hitting under 300k for a while, which is a very bullish sign. Companies may not be raising wages yet, but they are holding on to the people they have.

Retail Sales increased .7% in November, well above the .4% Street estimate. October was revised upward Ex autos and gas, sales rose .7%. Lower gasoline prices are providing a bit of an economic dividend.

Congress looks like they have circled around a spending bill to keep the government open for the near term. The left (led by Elizabeth Warren) is complaining about the bill. The Department of Homeland Security is funded only through February, which will give Republicans a chance to wrangle with Obama on the issue of his immigration executive order. There are also some relaxations to Dodd-Frank, and the left is apopleptic about that. The changes would allow FDIC institutions to use derivatives to hedge their own currency and f/x risk and would relax margin requirements for non-banks that use derivatives to hedge (like airlines hedging their fuel costs, for example). That said, it looks like the left will lose this battle.

Filed under: Morning Report | 13 Comments »

Posted on December 10, 2014 by Brent Nyitray

Markets are weaker this morning as oil (and oil stocks) continue to fall. WTI is trading at $62.20 after OPEC revised its 2015 forecast. Bonds and MBS are flat.

Mortgage Applications rose 7.3% last week. Purchases were up 1.3% while refis were up 13.2%. Don’t bust out the champagne quite yet, we are still basically bumping along the bottom.

Luxury builder Toll Brothers reported 4th quarter and full year results this morning. Deliveries rose 29% in dollars and 22% in units, but it looks like the torrid increase in average selling prices has passed and they are beginning to moderate. ASPs rose 6% YOY to $747k. Price appreciation for signed contracts was even less – around 3.6%. Backlog was up 3% in dollars and flat in units.

Robert Toll, CEO of Toll Brothers made a point I have been making for a long time – housing starts are still way below historical averages: “We believe the housing recovery has many years to run. Housing starts, through ups and downs from 1970-2007, have averaged about 1.6 million annually. According to Harvard University’s Joint Center for Housing Studies, ‘Despite the rebound in the last two years, home sales and starts are still nowhere near normal levels. This was the sixth consecutive year that starts failed to hit the one million mark, [which was] unprecedented before 2008 in records dating back to 1959.”

Obviously the recovery to normalcy depends on the first time homebuyer. Consistent rental inflation is pushing them to consider home ownership as an alternative. The NAHB is praising Fannie and Freddie for re-introducing the 3% downpayment loans.

Filed under: Morning Report | 88 Comments »

Posted on December 9, 2014 by Brent Nyitray

Markets are lower worldwide after a big sell-off in China. Bonds and MBS are rallying.

The Chinese government instituted new regulations for local debt last night, which sent the markets reeling. Chinese stocks have been on a tear recently (up something like 30% since Nov 1) so the news was an excuse for some major profit-taking, which sent the indices down something like 5%.

Small business optimism picked up a bit in December, as the NFIB Small Business Optimism approached the historical average before the Great Recession began. A big increase in economic optimism drove the increase. Earnings trends are heading higher, and some are planning to increase employment, which is good news for the economy.

Another good data point for the market: Job openings rose to 4.834MM in October from 4.685MM in September. This almost matches August’s number, which was the highest since early 2001. Combine that with a steady diet of sub 300k initial jobless claims prints and the leading indicators of the labor market are looking strong. Now about that wage growth…

New 3% down loans are expected to have only a marginal effect on increasing credit availability. Separately, This is all part of an attempt to get the first time homebuyer back into the market, which has been the Achilles Heel of this housing recovery. The problem is that while a 3% downpayment isn’t necessarily daunting, the credit score the banks require is – something like 755. For young adults with student loan debt, that sort of score probably just isn’t in the cards. Here are the FAQs for the 3% down loans from Freddie Mac.

Obamacare Architect Jonathon Gruber heads to Capitol Hill today to discuss the obfuscation and white lies involved in the selling of Obamacare. In an unfortunate (for him and Obama) minute of candor, he discussed how the the plan relied on the “stupidity of the American voters” to get it through, and how the “Cadillac Tax” was a brilliant piece of wordsmithing that set in motion the eventual taxability of employer-provided health care benefits. Don’t expect much out of Gruber – he will probably apologize for the language he used and spend the rest of the time lawyered up and will simply relay previously prepared talking points. Note that the Medicaid subsidy issue is going to be taken up by the Supreme Court as well, which could throw the whole thing in peril.

Filed under: Morning Report | 10 Comments »

Posted on December 8, 2014 by Brent Nyitray

Markets are lower this morning on no real news. Bonds and MBS are up.

The week after the jobs report is typically data-light, and this week is no exception. The highlights from a bond market perspective will probably be the JOLTS job openings on Tuesday and retail sales on Thursday. We will also hear from luxury home builder Toll Brothers on Wed morning.

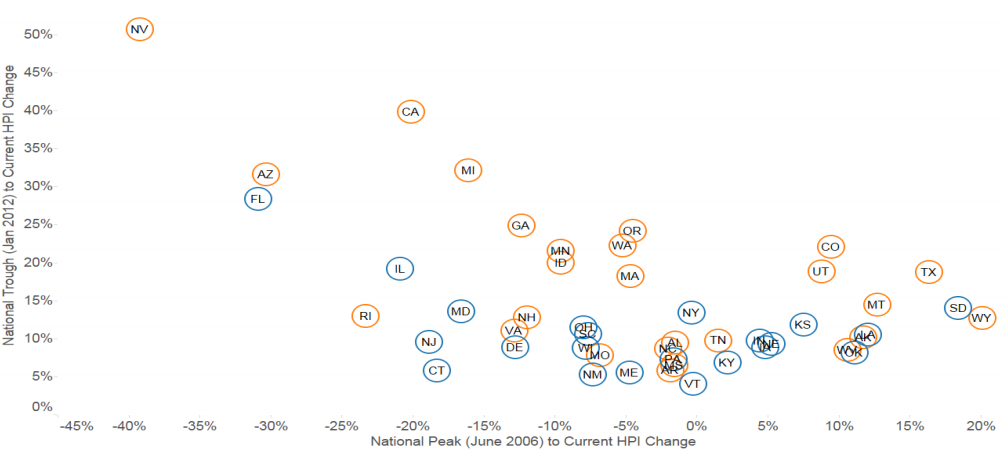

The latest Black Knight Mortgage Monitor is out. Foreclosure starts dropped by 10.5% to 81,400 and the foreclosure inventory dropped to 3.6MM homes, which is down 18% year-over-year. They have a cool chart that illustrates the difference between the judicial and non-judicial states in terms of home price appreciation, both in terms of decline and rebound. You can see how the judicial states have experienced much lower rebounds off the bottom than the non-judicial states. It would be interesting to see compare the peak to trough price declines of judicial vs. non-judicial states. I suspect we would find that having tougher foreclosure requirements did not help support house prices.

S&P lowered the ratings on Italy’s sovereign debt to BBB- from BBB, which is one level above junk status. Yet, Italian sovereigns are trading at 1.97%, 33 basis points lower than AA+ rated US Treasuries. This is all about the ECB and QE, but it shows again that all of this central bank manipulation of global sovereign bond markets has created some major dislocations. Of the 5 PIIGS, only Portugal and Greece have higher yields than the US 10-year. Strange times.

There were no changes in the federal limits on conforming loans for 2015.

San Francisco is looking at using eminent domain to steal from bondholders help people in who are in foreclosure keep their homes. The city is also trying to issue about $400 million in GO munis, and something like this cannot help.

Filed under: Morning Report | 22 Comments »

Posted on December 5, 2014 by Brent Nyitray

Markets are higher after a good jobs report. Bonds and MBS are getting slammed.

A not-too-shabby jobs report today. Payrolls increased by 321k, much better than the 230k estimate and the 208k ADP number. The two month revision was +44k. The unemployment rate held steady at 5.8% as did the labor force participation rate at 62.8%. We had a nice month-over-month increase in wages: up 0.4%, however on an annual basis, it was steady at 2.1%.

One strange anomaly: the household survey and the establishment survey differed in a big way – the household survey (which is conducted by sending questionnaires to individual houses) showed no employment growth, while the establishment survey (which is conducted by sending questionnaires to businesses) showed strong payroll growth. The market is clearly choosing to focus on the establishment data.

We could finally be hitting the point where the lagging employment indicators are catching up with the leading indicators. Recoveries after asset bubbles tend to be bathtub-shaped. We could finally be at the inflection point. Lower energy prices are going to be a big help as well.

Of course lower energy prices are not great for everyone – especially those companies in the energy patch. The big new distressed trade is energy debt as many over-leveraged and now cannot borrow. Shades of the mid / late 1980s.

It is an old cliche that all real estate is local. When I talk to people in San Diego, they describe a completely different housing market than the one I see up here in the Northeast. Interestingly, on the way to work today, I saw the first single family home being built since probably 2007. So maybe the Northeast is getting better at long last..

Filed under: Morning Report | 52 Comments »

Posted on December 4, 2014 by Brent Nyitray

Markets are lower as ECB President Mario Draghi addresses further action the ECB might take to boost growth. Bonds and MBS are flat.

It looks like Mario Draghi is kicking the QE can down the road a little more, and will address further stimulus measures in the first quarter. The Euro is rallying.

Initial Jobless Claims came in at 297k during the holiday shortened week. Announced job cuts fell 21% in November, according to outplacement firm Challenger, Gray and Christmas.

The ISM Non-Manufacturing Index rose to 59.9% in November as business activity and new orders surged. The employment index decreased however.

Completed Foreclosures fell to 41,000 in October, according to CoreLogic. This is a 26.4% decline from a year ago, and a 34% drop from September. The 12 month sum of foreclosures is at its lowest point since October 2000. Approximately 605,000 homes are in some stage of foreclosure compared to 875,000 a year ago. This represents about 1.6% of all homes with a mortgage. Unsurprisingly, the judicial states contain the highest inventory, with New Jersey at 5.5%, and New York and Florida at 4.1%.

The latest Beige Book shows that conditions improved overall during the months of October and November. The only disappointing news was that wage inflation remains “subdued.” Separately, Obama met with the Business Roundtable yesterday to push for wage increases. The Administration is also pushing for businesses to consider hiring the long-term unemployed. This is pretty much going to be an “either / or” type of situation.

Filed under: Morning Report | 10 Comments »

Posted on December 3, 2014 by Brent Nyitray

Markets are flattish on no real news. Bonds and MBS are flat as well.

Mortgage Applications fell 7.3% last week, which isn’t a surprise given the holidays. Purchases rose 2.5% while refis fell 13.4%.

ADP is forecasting the payroll number will come in at 208k this Friday. The Street is forecasting 230k.

Speaking of bond bullish, Amazon.com just did a $6 billion (!) bond issue, which contained a $1.5 billion tranche of 30 year bonds yielding 4.95%. The funds will be used for general corporate purposes. If you look at their balance sheet, they already have $7 billion in cash vs. $3 billion in debt outstanding, so it isn’t like they need the money. 30 years at under 5%. 7 years ago, the 30 year yielded more than that.

The latest kerfuffle in Washington doesn’t involve immigration – it involves a bunch of expiring tax breaks. Many of them are for individuals – tax breaks for teachers, tuition, mortgage debt forgiveness, mortgage PMI, and mortgage forgiveness. There are a number of business breaks in there as well. The Senate came up with a two year extension, but Obama promised to veto it because it doesn’t address the earned income tax credit and child tax credits that expire in 2017. He wants them to be made permanent. It looks like a 1 year extension bill is in the works. If this doesn’t get resolved, it could make for an interesting start to the tax year.

From the polar vortex making November the coldest in decades to El Nino ushering in a mild December, natural gas investors have been taken for a ride over the past six weeks or so. Fun fact – on the NYSE, they have Bloomberg or CNBC on the big TV monitors. In the commodity pits, they have on the Weather Channel. This is why. Look at the volatility of nat gas over the past month. roughly $3.50 to $4.50 and back to $3.80. Pretty amazing.

Filed under: Morning Report | 24 Comments »