Posted on October 17, 2014 by Brent Nyitray

Markets are higher as yesterday’s rally carries through. Bonds and MBS are down.

Housing Starts came in at 1.02 million, while building permits came in at 957k. Normalcy is 1.5 million, and that doesn’t even take into account population growth. We should be seeing starts coming at double what they are. Single family starts came in at 646k. Single fam has been relatively stable, while multi-fam has been extremely volatile.

Fed Head James Bullard made some dovish comments yesterday,which really turned around the market. The statement that got everyone’s attention was his suggestion that the Fed should consider maintaining QE for the time being. However, his point was not really all that dramatic – just that given the volatility in the markets, (coming primarily from Europe) and the fact that inflation expectations are falling with commodity prices, it might make sense to end QE at the December meeting, not the October one. He also stated that he believes we are a couple of jobs reports away from reaching historical norms in unemployment and the fundamentals of the economy are strong. He is not suggesting that we delay increasing interest rates, which is what people were hoping. Note that the Fed Funds futures moved pretty dramatically this week as they re-assessed their forecast for the first interest rate hike. The central tendency moved to late 2015 from mid 2015.

Wednesday’s pre-market bottom in the 10 year is feeling more and more like a capitulation. Look at the intra-day chart of the 10 year bond yield this week. It looked like a perfect storm of flight-to-safety, convexity buying, shorts throwing in the towel, and algo trading. The thing was trading like a tech stock. Again, I think of the roller coaster metaphor for the market – dizzying climbs, sickening drops, you end up in the same place where you started with less money in your pocket.

Filed under: Morning Report | 26 Comments »

Posted on October 16, 2014 by Brent Nyitray

Markets are still heavy this morning as Europe sells off. Bonds continue to rally, with the 10 year yielding 2.07%.

Is Ebola driving the correction in the stock market? FWIW, I don’t think so – I think it is European markets, which are collapsing. The Eurostoxx 50 index is down 13.5% over the past month. Note that Bullard is saying the same thing right now, and also suggesting that the Fed consider delaying the end of QE. Which begs the question – why? Rates are falling all on their own – does the Fed really need to keep purchasing bonds to drive the 10 year below 2%? Regardless, these dovish comments should be market positive, though how it affects the 10 year is an open question.

Was yesterday’s pre-market print of 1.95% on the 10-year the capitulation point? Could be, but watch credit spreads and the PIIGS. If spreads continue to widen, all bets are off.

Initial Jobless Claims fell to the lowest since 2000, with 264k people filing for first time unemployment. Continuing Claims rose 1,000.

Industrial Production rebounded in September after a dismal August, increasing by 1%. Capacity Utilization rose to 79.3%. Philly Fed fell to 20.7 from 22.5.

The NAHB Housing Market Index fell from 59 to 54. While builder sentiment dipped in October, they are still positive on the housing market. Given we are now in the seasonally slow period for the builders, I don’t know how much to read into this. Of course the big drop in rates could change that.

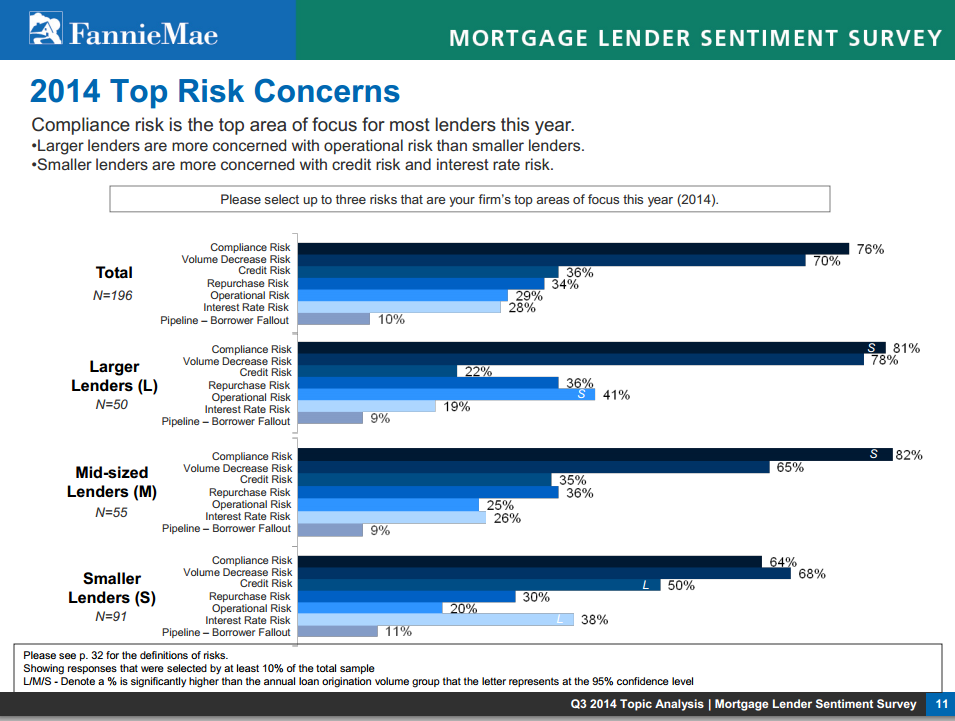

The latest Fannie Mae Lender Sentiment Survey discusses compliance costs and how much it costs. Most lenders (72%) reported that recent regulations have had a “significant” effect on their business. Mid-sized lenders reported a 50% increase in compliance spending. Note that most lenders are worried more about compliance risk than volume decrease risk.

Not housing related, but Lockheed Martin thinks we could have nuclear fusion within a decade. This is almost limitless power, without the radioactive waste that we get from nuclear fission, which is how we power our reactors today. It would also make a huge dent in CO2 emissions if it could be done on a large scale. This is a game changer on so many levels – strategic and economic.

Filed under: Morning Report | 6 Comments »

Posted on October 15, 2014 by Brent Nyitray

Markets are getting hammered this morning on global economic weakness. Bonds are flying.

Bonds are on fire this morning. The 10 year is trading below 2% level, and European bond yields are posting new lows. The German Bund now yields 73 basis points. Oil is getting smacked and the stock market futures are down hard.

Look at the chart of the 10 year yield – it is simply collapsing:

LOs should be pinging borrowers about refinancing. This rally could be a huge gift. Look at possible VA IRRLs.

Retail Sales fell .3% in September on falling energy prices. Ex autos and gas, they still fell .1%

The Producer Price Index fell .1% in September. Ex food and energy, it was flat. No inflation anywhere.

Mortgage Applications rose 5.6% last week. Purchases fell .7% while refis rose 10.6%. The 30 year fixed rate mortgage fell to 4.2%.

Not to sound Cassandra-ish, but when bond yields are collapsing like this, it is often a signal that something is very wrong in the plumbing of the financial system. Bonds simply don’t behave like this on a weak inflation number or a downgrade of Germany’s economic growth by 50 basis points.

I’ll conclude with this observation: Bond yields are at these levels without much in the way of QE any more. We could have gotten these yields without the Fed buying 3.5 trillion worth of assets?

Filed under: Morning Report | 23 Comments »

Posted on October 14, 2014 by Brent Nyitray

Stocks are higher this morning as bank earnings come in generally good. Bonds are flying on European weakness, and the 10 year hit an intraday low of 2.175 as Germany cut their 2014 – 2015 growth forecast by a pretty sizeable amount.

We had earnings from some big banks this morning. Citi and Wells beat numbers, while JP Morgan missed. On the origination side, Wells reported an $48 billion in originations, an increase of a billion from the previous quarter. Gain on sale margins increased from 1.41% to 1.82%. JP Morgan announced the bank had gained market share in mortgages, however they cut 6,000 jobs in the space and will probably cut another 1,000. For JP Morgan, originations were 21.2 billion, down 48% from a year ago, but up 26% quarter-over-quarter.

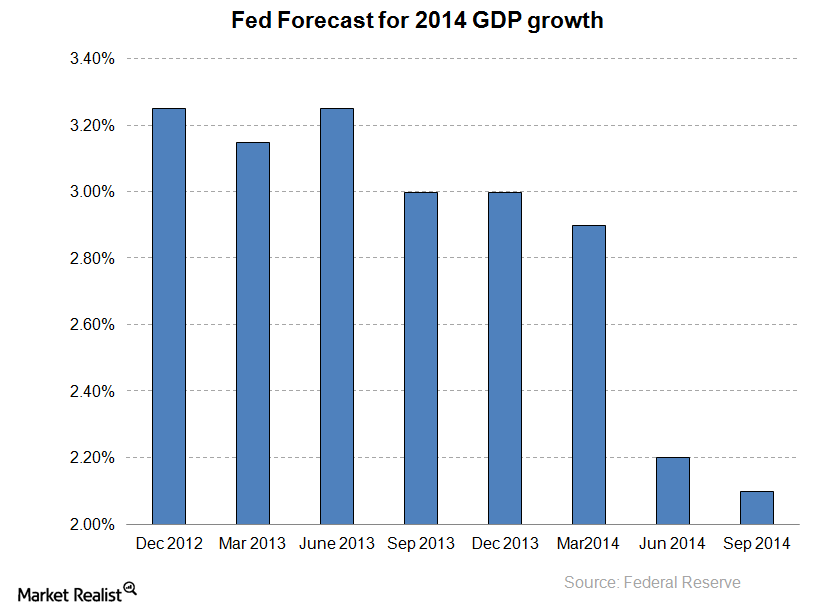

The NFIB Small Business Optimism Survey came in at 95.3, a drop from the prior month and below expectations. On the plus side, firms added .24 workers on average during the month. On the downside, only 22% of owners expect to make capital expenditures over the next 3 to 6 months. They note that the Fed has indicated it will raise rates in 2015, however the Fed’s forecasts for GDP have been over-optimistic. Take a look at the chart below. This is the Fed’s forecast for 2014 GDP growth starting at the December 2012 FOMC meeting and continuing through the September 2014 meeting. You can see how they have consistently cut their forecast.

Speaking of GDP growth, consumption is the biggest driver. It is looking like the holiday shopping season could be weak, with PriceWaterhouseCoopers predicting average holiday spending per household will fall to $684 this year from $735 in 2013. The National Retail Federation is more optimistic, predicting growth of 4.1%. Blame rising healthcare, childcare, and housing costs versus a backdrop of stagnant wages. Offsetting that of course is energy, with oil slipping below $85 a barrel. FWIW, the Back-To-School shopping season was meh, which is usually a good predictor of holiday sales.

Filed under: Morning Report | 11 Comments »

Posted on October 13, 2014 by Brent Nyitray

Markets are higher this morning on no real news. Bond and MBS markets are closed today for the Columbus Day Holiday.

No economic data this morning as bonds are closed. This week begins earnings season in earnest and we will hear from the biggest banks this week. Wells and Citi report tomorrow.

Last week, we saw a big rally in the bond markets, however TBAs didn’t really react all that much. This is strange considering the 10 year ended the previous week at 2.43% and went out Friday at 2.28%. The Fannie Mae TBA picked up about 13 ticks and the Ginnie Mae TBAs picked up 4 ticks – an extremely modest reaction, considered the huge jump in bond prices. Note the Bankrate 30 year fixed rate mortgage went up 15 basis points on Friday, which looks like a data error. Anyway, if borrowers are wondering why mortgage rates haven’t reacted all that much to the rally, the answer is that TBAs didn’t really react at all.

More anecdotal evidence that mortgage credit is easing. Includes info on TD and Shellpoint’s non QM loans.

Edward Quince – the pseudonym for the Bernank during the financial crisis. Expect more interesting tidbits out the AIG trial.

Filed under: Morning Report | 6 Comments »

Posted on October 10, 2014 by Brent Nyitray

Markets are flat on no real news. Bonds and MBS are up small.

The post FOMC minutes rally was certainly short-lived as we had another bloodbath in stocks yesterday. For the time being, it seems like US markets will be driven more by overseas events than domestic ones.

Import prices fell .5% month over month in September.

As global growth slows, the dollar rallies and commodities fall. This adds to the Fed’s predicament of missing its inflation target – in that inflation is too low. Chicago Fed Head Charles Evans says the Fed needs to reaffirm its commitment to its 2% inflation target and to stress that it will act if inflation is too low. The market may be treating the 2% inflation rate as a ceiling, and not the central tendency of a target. Evans said the FOMC could set a deadline, say two years, for returning inflation to its goal. Until you start seeing wage inflation approaching 4% or so, the Fed will probably continue to miss its inflation target to the downside.

As rates fall, can we expect to see another refinancing boom? According to Freddie Mac, probably not.

If the Republicans take the Senate this November, here are some of the issues that they plan to address: Medical devices tax, the Keystone pipeline, fast-track free trade. Another possibility – reining in the CFPB and making it subject to the appropriations process

Filed under: Morning Report | 5 Comments »

Posted on October 9, 2014 by Brent Nyitray

Stocks are lower after on overseas weakness. Bonds and MBS continue their post-FOMC minutes rally.

The 10 year traded below 2.28% earlier this morning as the market continues to digest the more dovish than expected FOMC minutes. The Fed is becoming concerned about global growth, and that could push them to keep rates low for longer. The minutes weren’t incredibly different from what the Fed has been saying all along, but combined with the weakness out of Europe and the strong dollar, was enough to push rates lower. Note the Bankrate 30 year fixed rate mortgage is flirting with a 3 handle. If this continues, we might see another refi wave, although prepayment burnout is probably the dominating factor at this point.

The thing to keep in mind is that US treasuries cannot be oblivious to what is happening in global bond markets, and global bond markets are rallying on international economic weakness. The German Bund hit an intraday low of 85.6 basis points this morning. In fact, remember the PIIGS (Portugal, Italy, Ireland, Greece, and Spain)? Only Portuguese and Spanish bonds yield more than the 10 year.

Alcoa kicked off earnings season last night with better than expected profits based on increased demand from autos and airplanes. Pepsico also reported good numbers based on its ability to push through price increases. Both of these reports should be bond bearish, not bullish, but here we are.

Initial Jobless Claims came in at 287k, the 4th consecutive week below 300k. People who have been out of work for a while may be struggling to find jobs, but those with jobs are keeping them.

Filed under: Morning Report | 8 Comments »

Posted on October 8, 2014 by Brent Nyitray

Markets are higher after yesterday’s bloodbath. Bonds and MBS are rallying.

Fears over global growth are beginning to worry the markets. One other thing to keep in the back of your mind is that third quarter earnings season is upon us as Alcoa reports after the close tonight. The rally in the dollar could end up crimping earnings for the big multinationals – something to keep in mind.

Today, we get the FOMC minutes around 2:00 pm. We could see some bond market volatility around that. LOs be aware.

Mortgage Applications rose 3.8% last week. Purchases rose 2.4% while refis rose 5%. During the week, bonds yields fell 4 basis points.

Job openings hit a 14 year high last month, according to the JOLTS survey. It looks like a lot of the growth was in health care and social assistance. Retail also reported a big increase in openings.

Home prices rose 6.4% annually in August, according to CoreLogic. Excluding distressed sales, they rose 5.9%.

Warren Buffet is perplexed by the lack of mortgage demand. Taking out a mortgage is the easiest way for a normal investor to short the bond market. Locking up money for 30 years at 4% is a no-brainer, considering that inflation has averaged about 4% over the past 60 years or so. Basically it is free money, and if we ever get another burst of 70s style inflation again, you are borrowing at a negative real rate. Warren has also been surprised by the lack of housing starts. As have many of us.

Filed under: Morning Report | 2 Comments »

Posted on October 6, 2014 by Brent Nyitray

Markets are higher on election results in Brazil, which is putting a bid under emerging markets. Bonds and MBS are down small.

This week has very little economic data to worry about (typical for the week after the jobs report). The most important event will be the FOMC minutes on Wednesday.

The banking system is loading up on Treasuries. They have all this cash that they are not putting to work. Of course all of the lawsuits and buyback demands isn’t helping things. Another interesting data point – S&P 500 companies are spending 95% of their profits on buybacks. This speaks to the lack of investment opportunities that companies see. It is the quintessential vote of economic pessimism.

A marriage of right and left – a new 15 year mortgage that uses the downpayment to buy down the rate closer to zero. A pilot program is already up and running. Interesting idea.

Last week’s decision on Fannie and Fred left investors with a bruising. The plaintiffs vow to continue the fight, however understand that Fannie and Fred common stock is a litigation lottery ticket. The only way it is worth any money is if a court overturns the legislation forming the FHFA.

Filed under: Morning Report | 18 Comments »

Posted on October 3, 2014 by Brent Nyitray

Markets are higher after a better-than-expected employment report. Bonds and MBS are down

Data dump from the jobs report:

- Nonfarm payrolls + 248k (+215k expected)

- Two month revision: + 69k (this is a good number)

- Unemployment rate 5.9% (6.1% expected)

- Labor force participation rate new low at 62.7%

- Average hourly earnings flat

- Average weekly hours increase to 34.6

The last time the labor force participation rate was this low was late 1977. This presents a dilemma for the Fed – will the labor force participation rate continue its decline? If so, then there is less slack in the labor market than we think. FWIW, I don’t see the Fed doing anything dramatic until we start seeing wage growth, and that is still nowhere to be found.

The ISM services index fell to 58.6 from 59.6 in August. This was slightly above the Street estimate of 58.5.

I know credit is tight, but what does it say when the Godfather of QE can’t refi? I guess the CFPB wants to make sure the Bernank doesn’t get a “predatory” loan.

Filed under: Morning Report | 4 Comments »