Stocks are lower this morning on no real news. Bonds and MBS are flat.

Mortgage Applications rose 1.4% last week. Purchases fell .4%, while refis rose 2.7%. The 30 year fixed rate mortgage finally fell six basis points after stubbornly resisting the moves in the bond market.

Later on today, we will get the FOMC minutes. While there were no changes to the economic forecasts, the markets will be looking to see if the circle of hawks is growing.

Job growth is mainly at the low end of the pay scale. But the wage growth is mainly at the high end. The US labor market is incredibly bifurcated at the moment. This is certainly what keeps Janet Yellen up at night, although the bigger question is whether the Fed can really do anything about it.

BlackRock chief investment strategist Russ Koesterich is saying that bonds have it right, stocks have it wrong with respect to the view of the economy. The higher debt levels will act as a drag on growth for the next decade or two. In other words, we are Japan, and Reinhart / Rogoff are right. This is of course heresy to Dr. Cowbell, who believes the solution to the economic morass is to borrow more (since rates are so low) and to spend it on infrastructure. Japan did exactly what Krugman wanted, and took their debt to GDP ratio to 2.2x and has had little to no economic growth for a generation. As a point of reference, our debt to GDP ratio just over 106%, however the Fed owns about a quarter of that (through QE) so it is really debt we owe ourselves.

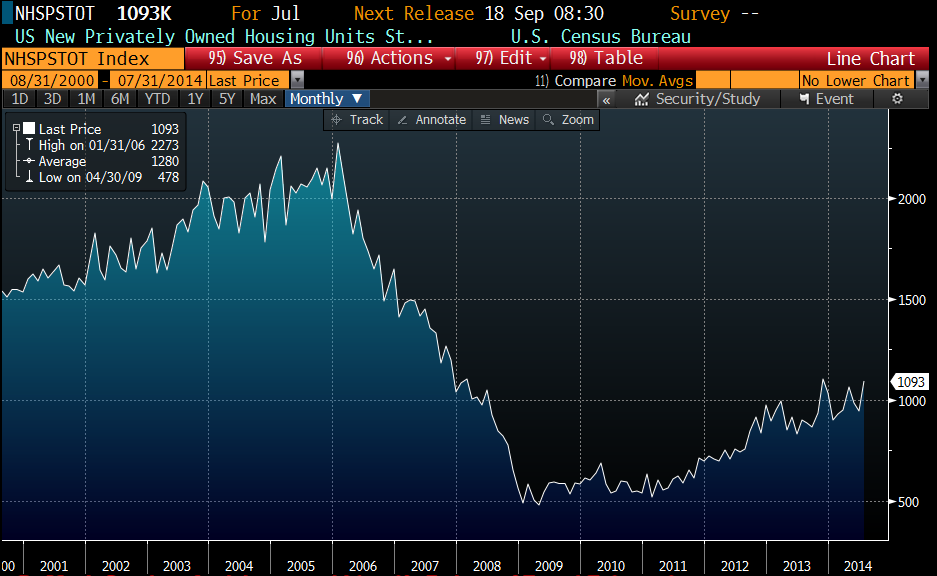

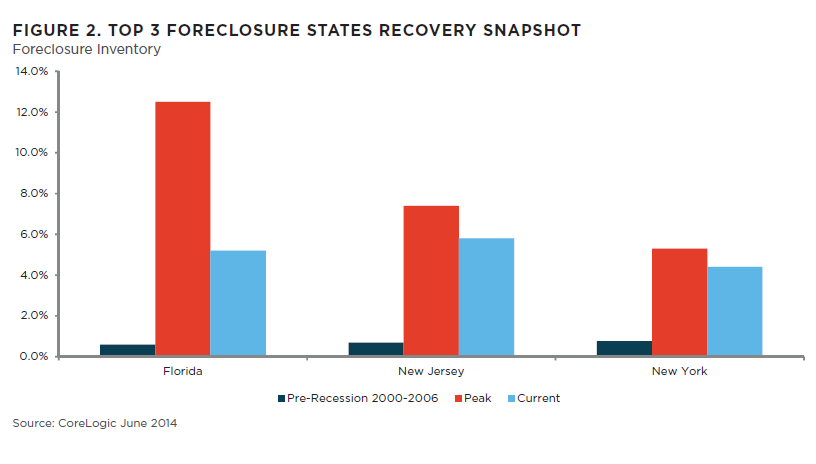

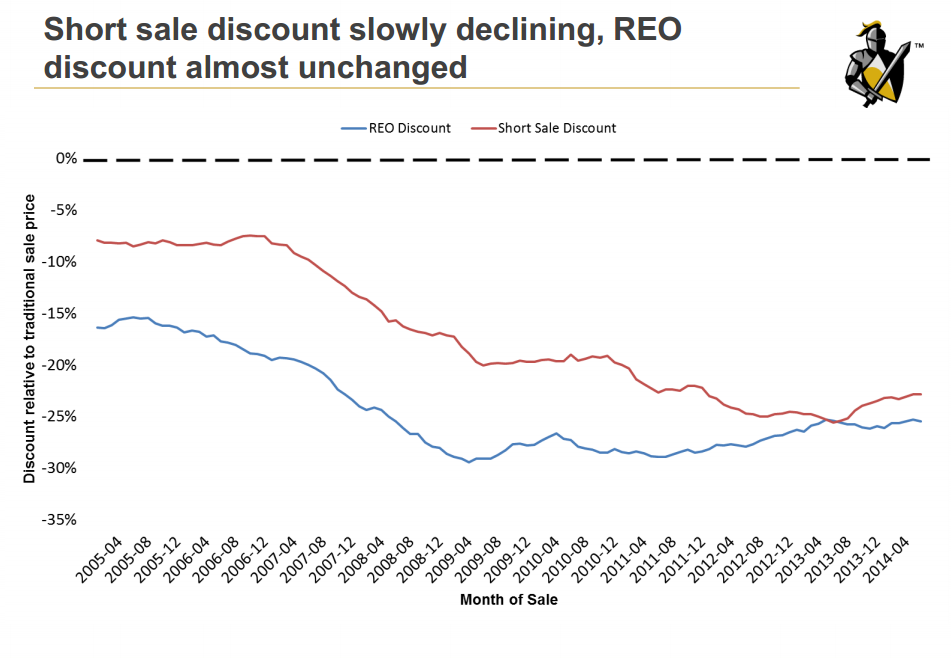

Foreclosure starts and Delinquencies ticked up in June, according to Black Knight Financial Services (formerly known as Lender Processing Services or LPS). DQs increased to 5.7% from 5.62% in May, while foreclosure starts ticked up to 88.3k vs 86.3k a month before. On a year over year basis, foreclosures starts are down 19%. Inventory continues to be concentrated in the judicial states of NY, NJ, and FL. Short sale discounts continue to narrow, while the REO discount is flat.

Filed under: Morning Report | 13 Comments »