Vital Statistics:

|

Last |

Change |

Percent |

|

|

S&P Futures |

1550.7 |

2.2 |

0.14% |

|

Eurostoxx Index |

2661.8 |

22.8 |

0.86% |

|

Oil (WTI) |

93.96 |

-0.5 |

-0.52% |

|

LIBOR |

0.28 |

-0.001 |

-0.25% |

|

US Dollar Index (DXY) |

83.19 |

0.469 |

0.57% |

|

10 Year Govt Bond Yield |

1.77% |

-0.04% |

|

|

Current Coupon Ginnie Mae TBA |

104.9 |

0.1 |

|

|

Current Coupon Fannie Mae TBA |

103.7 |

0.2 |

|

|

RPX Composite Real Estate Index |

189.4 |

0.1 |

|

|

BankRate 30 Year Fixed Rate Mortgage |

3.68 |

Markets are giving back some Japan-led gains after Initial Jobless Claims spiked to 385k from 357k. This was the holiday-shortened Easter week, so there is a seasonality adjustment there. On a non-seasonally adjusted basis, they fell. Bonds and MBS are rallying, with the 10 year yield down to 1.77%.

The Bank of Japan outlined more aggressive monetary actions last night with their own version of quantitative easing. This pushed the Nikkei 225 stock market index up 2%, and caused a sizeable drop in the yen. This explains the rally in US bonds as Japanese investors flee for the “high yielding” US treasury market. Don’t laugh – the Japanese 40 year bond (the 2’s of 52) yields 1.34%. The US 10-year at 1.77%, in the context of a depreciating yen, is reviving the yen carry trade. The Yen Carry Trade is when Japanese investors borrow funds at yen rates and invest in high-yielding sovereign debt. They benefit from the pickup in yield and any favorable currency movements. With the high quality Euro sovereigns yielding even lower than the US, we are the only game in town. Punch line – this will put downward pressure on mortgage rates in the US, at least at the margin.

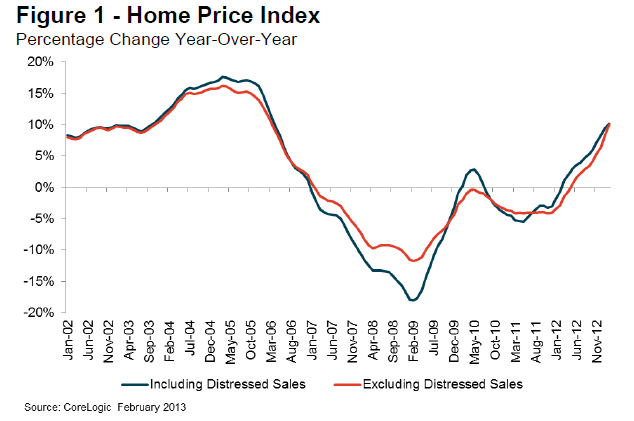

The CoreLogic Home Price Index increased 10.2% on a year-over-year basis in February, the highest increase since March of 2006. It is the 12th consecutive monthly increase. The gains were broad based, with 96% of their MSAs reporting gains. California, Arizona, and Nevada all showed gains in the high teens. They are forecasting a 2% month over month increase in March, or 12% year over year.

Chart: CoreLogic Home Price Index

Hank Paulson, George Bush’s Secretary of Treasury, says that Fannie Mae’s new profitability shouldn’t deter the government from establishing a new platform for mortgage finance. He mentioned the Washington Post article that says the Administration is pushing banks to make home loans to people with weaker credit. Nominated to take over as Treasury Secretary just as the housing bubble was peaking, he can be forgiven for being a little gun-shy on re-inflating the bubble.

San Francisco Fed President John Williams said he is hopeful that “the economy has shifted into high gear” and that the Fed could begin slowing the purchases of Treasuries and MBS this summer, with a full exit by the end of the year.

Finally, you can hear my latest interview on Capital Markets Today, where I discuss real estate pricing, politics, and the economy.

Filed under: Morning Report | 70 Comments »