Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1514.3 | -2.2 | -0.15% |

| Eurostoxx Index | 2616.9 | 0.2 | 0.01% |

| Oil (WTI) | 90.76 | 0.1 | 0.09% |

| LIBOR | 0.283 | -0.001 | -0.35% |

| US Dollar Index (DXY) | 82.31 | -0.004 | 0.00% |

| 10 Year Govt Bond Yield | 1.84% | 0.00% | |

| RPX Composite Real Estate Index | 194.9 | 0.2 |

Markets are slightly lower this morning after China imposed new measures to slow its housing bubble. There isn’t much in the way of economic data this week with the exception of the jobs report, which was moved to this week. Bonds and MBS are flat.

While the unemployment rate stays stubbornly in the high 7s, there are signs under the surface that things are getting better. The median duration of joblessness fell to 16 weeks in January from 25 weeks in June 2010. American aged 45-55 experienced the biggest turnaround, and this would address one of the biggest achilles heels to the economy: that many people in their prime earnings years are on the bench, which crimps spending. Nobel Laureate Dale Mortensen views this as evidence that the US labor market will not enter hysteresis, or permanently higher joblessness, which happened in Europe in the 80s.

Is slower economic growth the “new normal?” There are a few explanations why the economic recovery has been so slow. The first is simply bad luck. A series of exogenous events (the Euro crisis, crises in Washington, the Japanese tsunami) keep delivering blows to the economy just as it is getting going. The second is the view of Kevin Warsh, which holds that bad policy decisions in the aftermath of the financial crisis – overregulation and a focus on short-term stimulus measures) have left the economy weakened. The last is the view of the Keynsians, who argue that the stimulus was not enough, we need to do more, and as long as the bond market is willing to lend to us at sub 2% rates, we should borrow as much as we need to upgrade our infrastructure and hire millions of unemployed workers in the process.

FWIW, I believe that all of these explanations have a kernel of truth, but miss the big picture – that we are recovering from an asset bubble, and the de-leveraging that follows takes a long time to work through. When people borrow en masse to fund asset purchases, the debt remains even if the asset falls in value. That debt has to be dealt with, and someone has to eat the losses. While Washington would love to figure out a way to short-circuit this process, there isn’t a good way to do it. Much of the policy debate in Washington has centered over who should shoulder the costs, but you can’t make them go away. And until they are dealt with, they will act as a drag on the economy.

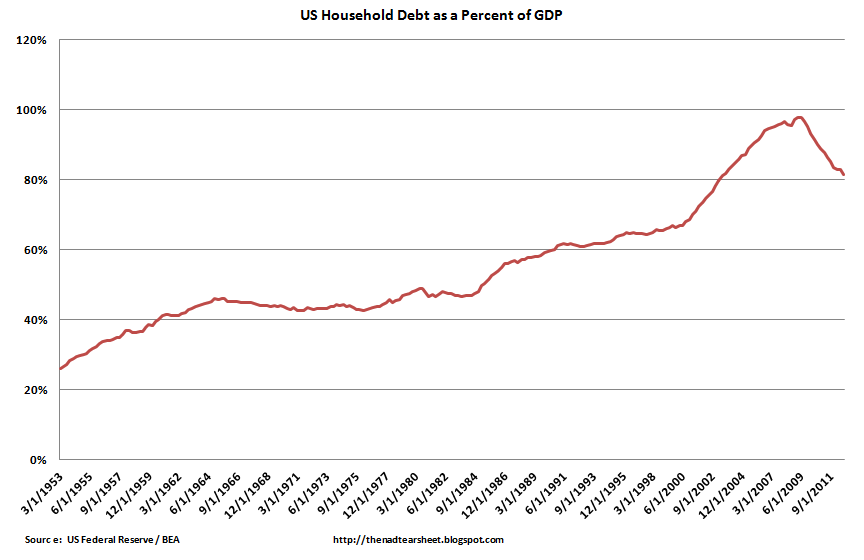

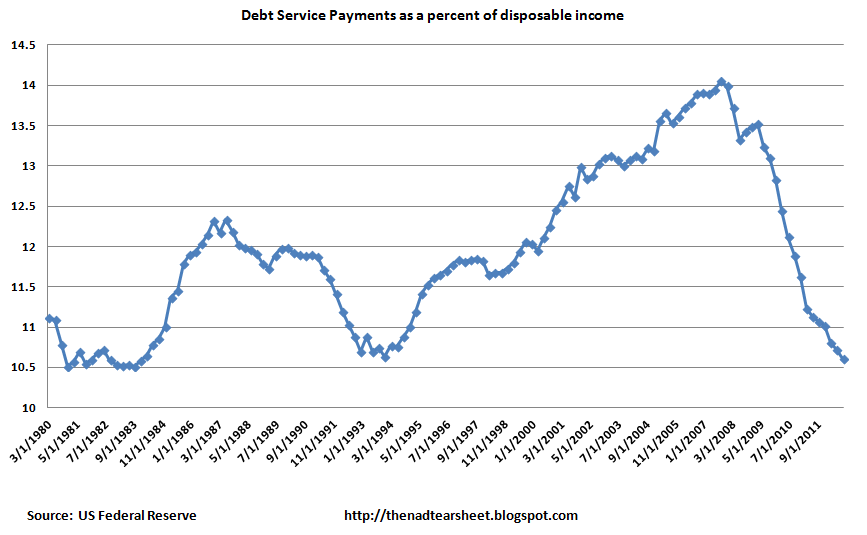

Luckily, corporate America is awash in cash. They are done deleveraging. The banks are still working their way through it, and no one really knows where they are marking some of their dodgier paper. Households are a mixed bag. Debt service (the amount of principal and interest payments) is at multi-decade lows, however the total amount of debt is not. We have some ways to go here. The recovery will be made on two fronts – debt will be slowly paid down, while real estate prices will continue to rise. And that is why the Fed is doing QE – to (officially) cut down debt service payments, and to (unofficially) help goose the real estate market.

Chart: US Household debt as a percent of GDP:

Chart: Debt Service Payments as a multiple of disposable income

But ZIRP and QE isn’t “free.” Unintended consequence of ZIRP # 547,624 – a bubble in student loan paper. Sallie Mae just sold $1.1 billion of securities backed by private student loans (in other words, not backed by the Federal Government) and the riskiest tranches were 15x oversubscribed. This year alone, dealers sold $5.6 billion of student loan backed securities, with an average yield of 1.48%. And we have only issued about a billion dollars worth of jumbo securitizations since the bubble burst? I find it absolutely amazing that we can securitize unsecured loans made to students majoring in underwater basket weaving, but we can’t securitize a stated income loan. Is it Dodd-Frank and its open questions regarding “skin in the game” for issuers? If it is, I suspect the private label market will come back in a hurry once the regulators figure out what they want to do.

Filed under: Uncategorized |

About time, sheesh, lazy much?

But seriously, thanks!

What about the concept (that I read somewhere)(seriously, I did!) that countries with high debt to GDP ratio’s, in the neighborhood of +70%, generally have slower growth, in the neighborhood of 1-2%?

Anybody else remember or have read this?

LikeLike

I haven’t read that George, but it makes sense: If the local private sector is growing, then the local government should be solvent. Cause and effect. If the local private sector is contracting, then local government cannot contract fast enough to stay out of debt. This would be especially true if the property tax base crumbled.

The “beauty” of the real property tax base is its predictability. Doesn’t always work out that way, however.

Or so it would seem to me.

LikeLike

The cancer spreads. Nauseating.

http://m.washingtonexaminer.com/tim-carney-health-industry-pushes-gop-states-toward-obamacare/article/2523136#.UTTS7Pq9Kc0

Yeah us.

Doom.

LikeLike

http://www.kaiserhealthnews.org/stories/2012/august/06/third-of-medicaid-doctors-say-no-new-patients.aspx

just because you enroll someone in Medicaid, doesn’t mean they will have access to a doctor.

LikeLike

A good report. Interesting in light of the interview of the Romneys yesterday. It would seem that many voters came to similar conclusions.

Not sure how a grandstanding AG is going to help matters. We will fortunately be done with ours soon. I’ve nearly decided to support Bolling if he runs.

∂ß

LikeLike

OT: NoVA–started Game of Thrones last night, was up until 0430 reading. You were right–great book! I’m on p 272 of 807.

LikeLike

” miss the big picture – that we are recovering from an asset bubble, and the de-leveraging that follows takes a long time to work through. When people borrow en masse to fund asset purchases, the debt remains even if the asset falls in value.”

Well put. I would add that at the consumer level borrowers are more wary of debt fueled consumption, compared to the sights. That lowers the level of potential consumer.

spending

LikeLike

Sights-> aughts

LikeLike

well, the debt fueled consumption of the aughts was done largely through HELOCs. You need home equity to fuel the borrowing.

That said, how many people fund their monthly expenses on a credit card and pay it off every month to get points? I think that inflates the debt numbers a bit.

LikeLike

“expenses on a credit card and pay it off every month to get points?”

guilty. i’m addicted to airline miles. i know i won’t win, but i can’t stop.

that said, i did just score a round trip to vegas in 1st class.

Michi — glad you’re enjoying it. i’m midway through book 3. I saw at PL that LMS picked it up adn realized she read it 10 years ago.

LikeLike

Funny exchange with Juiceboxer Ygleisias.

http://storify.com/seanmdav/matthew-yglesias-does-not-understand-basic-account

LikeLike

McArdle doesn’t answer the question of why we’ve been bouncing on the bottom for 4 years, but poses some depressing ones if this is the new normal.

http://www.thedailybeast.com/articles/2013/03/04/don-t-have-enough-to-worry-about-here-s-one-more-thing-low-growth-may-be-here-to-stay.html

LikeLike

I was wrong, Obama is a capitalist at heart. He charges whatever the market will bear.

http://www.politico.com/politico44/2013/03/wh-no-set-price-for-meeting-with-obama-158389.html

LikeLike

McWing: which Drudge headline was it that you found hilarious this morning?

LikeLike

Republicans winning the sequester fight:

This is ahead of schedule. Boehner had announced previously it was going to take two weeks. This bodes well for the premise that the leadership has successfully rounded up enough votes to pass it.

LikeLike

Michi, It was a picture of an Elephant being eveloped by locust and was entitled: And Now The Locust.

LikeLike

Thanks, McWing–don’t think it was up when I clicked on your link (or some setting that I have prevents the Drudge site from loading pictures); the whole thing just looks like headlines to me. Or just a bunch of sentence fragments, if that makes more sense.

LikeLike

I linked to the mobile site.

Try:

http://www.Drudgereport.com

Should still be up, top left? He changed the headline so, to me anyway, it’s not as funny.

LikeLike