Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1409.8 | -2.5 | -0.18% |

| Eurostoxx Index | 2436.2 | -16.6 | -0.68% |

| Oil (WTI) | 97.49 | 0.2 | 0.24% |

| LIBOR | 0.427 | -0.004 | -0.91% |

| US Dollar Index (DXY) | 81.34 | -0.143 | -0.18% |

| 10 Year Govt Bond Yield | 1.70% | 0.00% | |

| RPX Composite Real Estate Index | 192 | 0.0 |

Initial Jobless Claims came in at 372k, a little higher than expected and pretty much in line with the latest trend of 375k / week. New Home Sales increased to 372k in July

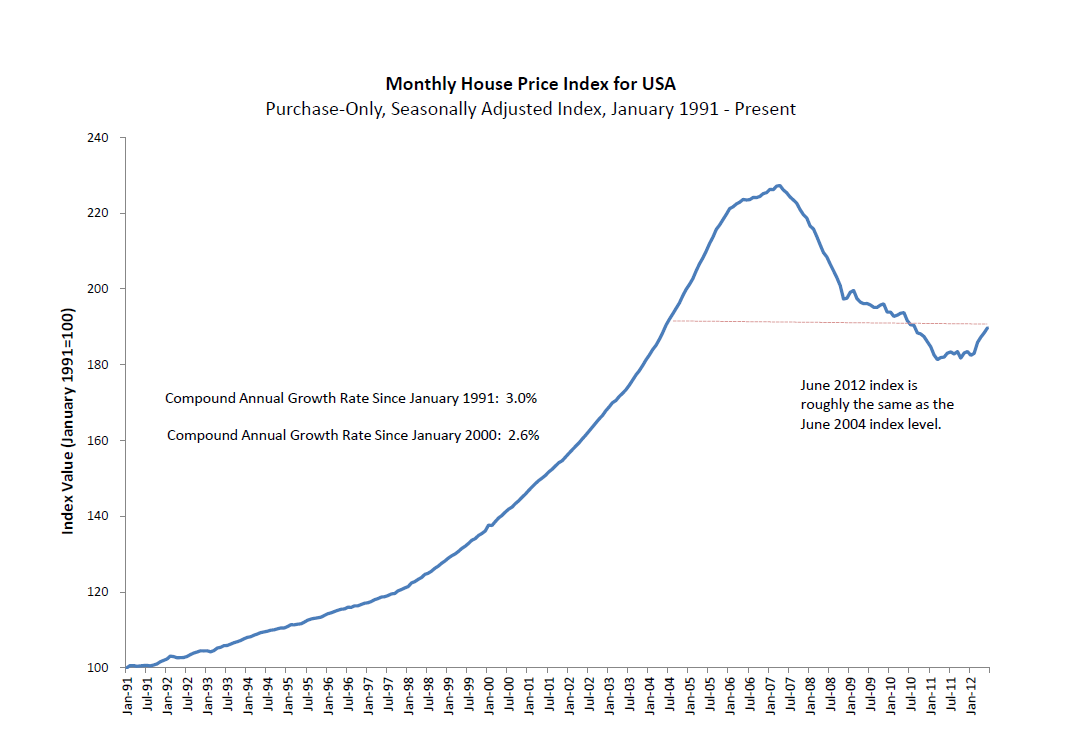

The FHFA Home Price Index increased 3% YOY and .7% MOM. This report only focuses on conforming mortgages, which makes it a more stable index than Case-Schiller or RPX.

The FOMC minutes noted that economic conditions have decelerated from earlier this year and discussed the possibility of another round of quantitative easing. This drove the 10 year yield from 1.8% to 1.7%. MBS rallied as well. My view has been that we are getting too close to the election – the Fed wants to appear non-political and definitely does not want to influence elections. However this morning, St Louis Fed President James Bullard characterized the minutes as “stale,” noting that some of the data lately indicates the economy is getting stronger again.

CBO is forecasting 2.25% economic growth for the rest of the year and unemployment above 8%. If Taxmageddon is not averted, CBO projects a recession with real GDP declining .5% from Q412 to Q413 and unemployment rising to 9%. If all the tax hikes and spending cuts are held off indefinitely, their projection is pretty much where the economy is now – 1.7% GDP growth with 8% unemployment. So the goalposts are (a) very modest recession vs (b) very modest recovery. Which means interest rates aren’t going anywhere.

Chart: FHFA House Price Index

Filed under: Morning Report | 122 Comments »