Vital Statistics

| Last | Change | Percent | |

| S&P Futures | 1305.2 | -9.6 | -0.73% |

| Eurostoxx Index | 2148.5 | -44.3 | -2.02% |

| Oil (WTI) | 91.15 | -0.7 | -0.76% |

| LIBOR | 0.467 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 81.71 | 0.218 | 0.27% |

| 10 Year Govt Bond Yield | 1.74% | -0.03% | |

| RPX Composite Real Estate Index | 176.2 | 0.6 |

Markets are lower this morning on GREXIT (Greek exit) fears and a lousy earnings report from Dell. Euro sovereign yields are generally lower, with the exception of Greece which is 22 basis points higher and approaching 30%. Remember, this is the post-reorg debt that is trading here. Their debt was trading around 35% before Greece did their restructuring about 10 weeks ago. The stress in Europe is pushing down bond yields here and MBS are up as well.

While the migration to tablets is hurting Dell, they also noted corporations are delaying spending. Is it because IT spending is slowing in general, or is it that corporations have learned not to beta-test Microsoft operating systems (in this case Windows 8)?

The Congressional Budget Office weighs in on Taxmageddon. Punch line: The budget deficit will drop by $560 billion, and real GDP growth will be .5%, with a contraction of 1.3% in 1H and an expansion of 2.3% in 2H. Remember the government operates on a Sep fiscal, so they are predicting recession in the Sep 12 – Mar 13 time period. If we cancel the tax increases and spending cuts, CBO estimates that real GDP growth would be about 4.4% in real (not nominal) terms in CY13. That is an aggressive (with a capital “A”) forecast.

DealBook has an interesting article on the possible unintended consequences of breaking up the big banks.

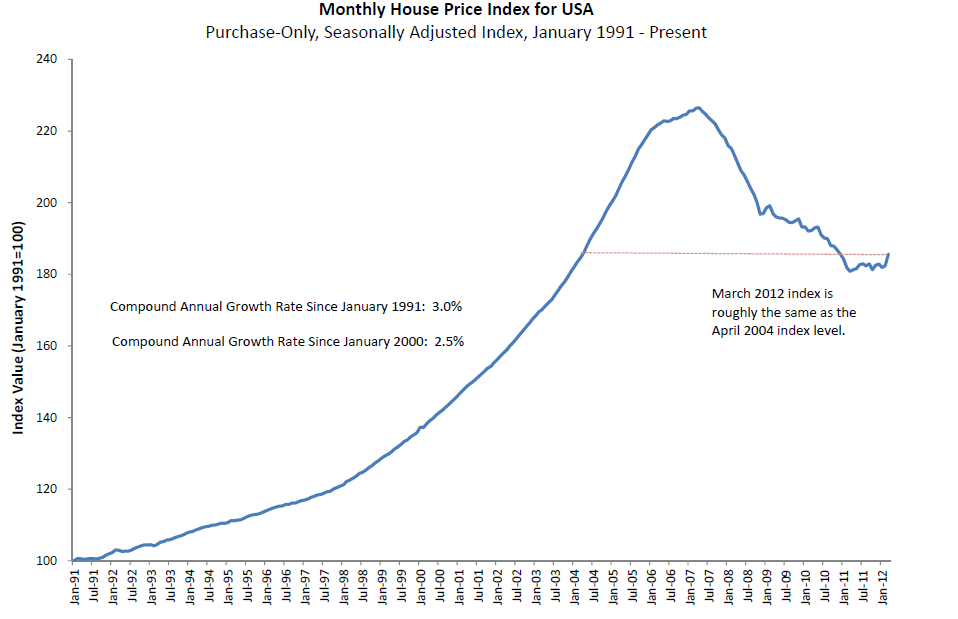

In other news, the NAR has declared the housing recovery to be underway. The MBA reported that mortgage applications increased 3.8% last week. New home sales in April were 343k, an increase of 3.3% MOM. The FHFA House Price index showed an increase of .55% QOQ and .5% YOY. This is the first increase since early 2007. Remember the FHFA index only looks at conforming loans, which is more of the “core” housing market. It has proven to be a much less volatile index than Case-Schiller or RPX.

Chart: FHFA House Price Index:

Filed under: Morning Report |

“Remember the FHFA index only looks at conforming loans”

wouldn’t that exclude large parts of the country? Finding a single-family home for 417 or less is basically impossible in the DC metro area.

LikeLike

Median house price in the Washington DC MSA was 311.6k in Q112.

Click to access metro-home-prices-q1-single-family-2012-05-09.pdf

LikeLike

Leading the nation out of recession:

http://www.statesman.com/blogs/content/shared-gen/blogs/austin/theticker/entries/2012/05/18/austins_jobless_rate_drops_to.html?cxntfid=blogs_statesman_business_blog

http://www.statesman.com/business/real-estate/its-now-a-sellers-market-in-central-texas-2368800.html?cxtype=rss_ece_frontpage

LikeLike

Thanks Brent — I just don[‘t see it. especially at the single-family level. condos and townhomes, sure. looks like WVA is included in that. that must be offsetting the higher priced NoVA area.

LikeLike

“While the migration to tablets is hurting Dell, they also noted corporations are delaying spending. Is it because IT spending is slowing in general, or is it that corporations have learned not to beta-test Microsoft operating systems (in this case Windows 8)? ”

For us, it’s because every Microsoft upgrade after Windows XP and Office 2003 hasn’t had any business value at all in and of itself, but rather has been done solely when we are forced to do so due to hardware or software compatibility issues with PC upgrades or line of business software. I.e. it’s strictly reactionary to external events.

LikeLike

For anyone who as an interest in the Tyler Clementi suicide case, the New Yorker piece on it should be required reading. All in all an excellent example of long form (14 pages) journalism with on the record interviews and quotes.

http://www.newyorker.com/reporting/2012/02/06/120206fa_fact_parker

LikeLike

Fighting the Man, one speed trap at a time.

http://articles.orlandosentinel.com/2012-05-22/news/os-flashing-headlights-ruling-20120522_1_ryan-kintner-free-speech-headlights

LikeLike

Worth a read on the debate over Eurobonds and Greece:

“Europe Doesn’t Need More Debt

A new means of borrowing would not convince anyone that public finances were on a more sustainable trajectory.

Simon Johnson

May 22, 2012

The issue of “euro bonds” by a central European authority – for example, some form of jointly owned treasury – would not by itself bring the euro area crisis under control. The euro area as a whole already has a high level of debt outstanding – 90 percent of G.D.P., according to the International Monetary Fund. (This calculation treats the euro area as if it had a consolidated balance sheet, which it does not.)

The issuance of euro bonds would just add to government debt in Europe, and in the process would add more subsidies to troubled countries. This would not convince anyone that public finances were now on a more sustainable trajectory.

Europe could move toward creating a viable federal authority with its own sources of revenue and the ability to issue debt – just as the United States did at and after the Constitutional Convention of 1787. New federal debt could be supported by the European Central Bank, just as the Federal Reserve System in the United States works within the federal government structure. At the national level, European countries could become more like U.S. states, whose debt is not generally supported by the Fed.

Such a transition to a central fiscal authority is necessary but not sufficient to resolving the current crisis. There is still the issue of excessively high debt levels in some countries. In the U.S., this state-level debt from the war of independence was “assumed” onto the federal government. This was controversial when first proposed by Alexander Hamilton and became a huge political fight. Europe is more likely to have debt restructuring than any federal takeover of existing public debt.

Longer-term problems would still remain. It is hard for peripheral Europe to grow and to again become competitive within the single currency.

Simon Johnson is co-author of “White House Burning” and a contributor to Economix.”

http://www.nytimes.com/roomfordebate/2012/05/22/can-euro-bonds-save-the-union/europe-doesnt-need-more-debt

LikeLike

I like SJ and what he says sounds right.

This from FT – may be behind the paywall, so I lay it out here:

A fragile Europe must change fast

By Martin Wolf

I sympathise with the Germans. This is not because I agree with their prevailing view of how the crisis occurred or what to do about it. I sympathise because the German elite were the ones who understood what creating the euro implied. They realised that a currency union could not work without a political union. But the French elite wanted, instead, to end their humiliating dependence on the monetary policy set by Germany’s Bundesbank. Now, two decades later, Germany’s partners, including France, have learnt a painful lesson. Far from being liberated from German control, they are now far more firmly under it. In a big crisis, creditors rule.

Consider how much better off Europe would have been if the exchange rate mechanism had continued, instead, with wide bands. Interest rates in the crisis-hit countries would probably have been higher and asset price bubbles and current account deficits smaller. When the turnround in financial flows occurred, currency crises would indeed have erupted. The Greek drachma, the Irish punt, the Portuguese escudo, the Spanish peseta, the Italian lira and, maybe, the French franc would have devalued against the Deutschmark. Price levels of these countries would have shown a temporary jump. But the blame for any fallout would have fallen overwhelmingly at home. I feared that the euro would weaken the sense of mutual trust, in a crisis, not reinforce it. So it has proved already, even though the eurozone has barely started the adjustment.

Why, then, do creditors rule in a crisis? The answer is simple: they can borrow cheaply. As lenders have fled from weaker credits, the interest rate on German Bunds has fallen to 1.3 per cent, against 5.8 per cent in Italy and 6.2 per cent in Spain. With flat nominal gross domestic products, countries with high interest rates are at risk of falling into a debt trap. They need help in controlling their costs of borrowing that only creditors can supply. (See charts.)

As Harold James of Princeton University, Ronald McKinnon of Stanford and many others have noted, Alexander Hamilton, the first US Treasury secretary, confronted a not dissimilar challenge with the debts incurred by the states in the American war of independence. Hamilton used the powers of the (second and centralising) constitution to assume these debts, issuing new federal debt, instead. In the long run, the modern US federal system emerged, with limits on state borrowing, a central bank (at the third time of asking) and a federal budget able to stabilise the economy.

Since dismantling the eurozone would be very costly, as I argued last week, could such a union deal with the current difficulties? The answer, in theory, is yes. The eurozone already has a central bank. The fiscal compact beloved of Angela Merkel, Germany’s chancellor, could be the equivalent of the balanced budget rule of US states. So what is missing for a life “happy ever after”? The answer seems to be a robust fiscal arrangement, to cushion the impact of crises, help members manage their debts and cut the link between weak sovereigns and banks.

Yet assumption of debts by a central treasury or replacement of national by federal fiscal mechanisms support is out of the question. The budget of the EU is 1 per cent of gross domestic product. There is no will to make it bigger.

In place of such central action, stronger solidarity among members would need to emerge. But I find it hard to believe such measures would endure. The European Stability Mechanism, designed in this crisis to help countries in difficulty, is too small, at just 5 per cent of eurozone GDP. The answer would have to be some kind of eurozone bonds, with joint and several backing. Support will be quite limited. Creditworthy members tend to dislike supporting the “irresponsible”. Voters dislike sharing with non-voters. Crucially, the federal constitution preceded Hamilton’s solution, though the big debts were a reason for ratification.

If dismantling the euro is out of the question, true federal finance is unavailable and mutual solidarity will remain limited, what is left? The answer is faster adjustment, to bring economies back to health. Indeed, that would be essential even if stronger solidarity were available. The eurozone must not turn the weaker economies of today into depressed regions, permanently supported by transfers, a policy that has blighted the south of Italy.

So how is faster adjustment to be achieved? The answer is through a buoyant eurozone economy and higher wage growth and inflation in core economies than in the enfeebled periphery. Moreover, the required growth strategy is definitely not just a matter of policies for supply. According to forecasts from the International Monetary Fund, eurozone nominal gross domestic product will rise by a mere 20 per cent between 2008 and 2017. In the latter year, it will be 16 per cent lower than if it had continued to grow at the rate of 4 per cent achieved between 1999 and 2008 (consistent with 2 per cent real growth and 2 per cent inflation). For the economies under stress, such feeble growth in the eurozone is a disaster: it means that the eurozone as a whole tends to reinforce, rather than offset, their credit contractions and fiscal stringency. They can blame the universal adoption of fiscal stringency and the policies of the European Central Bank, which let the money supply stagnate.

What has this to do with the risk of a Greek exit and the need to manage the fallout, should this occur? Nothing and everything. Nothing, because it will still be necessary to manage panics, almost certainly by unlimited ECB support, as Jacek Rostowski, Poland’s finance minister, has argued in the FT. Everything, because with large divergences in competitiveness, weak fiscal solidarity and fragile banks, a plausible prospect of adjustment into growth is vital. If countries face year after weary year of debt deflation and depression, the euro risks becoming a detested symbol of impoverishment. As a strong federal union, the US will bear the strain of such sustained disappointment. The far more fragile eurozone will not.

LikeLike

Housing across Michigan seems much better, but I wonder if the true beneficiaries are investment groups and wealthy people rather than the usual middle class house purchser. Not saying that is good or bad, just an observation. A colleague is currently renting a house, but needs a bigger home for his growing family. Every house he bids on is purchased by someone paying either cash or putting 30% or more down. And the sales are happening really fast. My sister in law is experiencing a similar phenomenon in Grand Rapids, MI. Every house she looks at is sold within a week.

LikeLike

rumor going around that SCOTUS will run on ACA tomorrow. too good not to post. but it completely unsubstantiated.

LikeLike

“novahockey, on May 23, 2012 at 1:55 pm said:

rumor going around that SCOTUS will run on ACA tomorrow. too good not to post. but it completely unsubstantiated.”

But how will that impact the price of Facebook?

LikeLike

Facebook price will go up when we’re all mandated to buy it.

LikeLike

I’m pretty sure the Facebook mandate idea originated at Heritage.

LikeLike

Mark, is this the entire editorial? If so, I found this statement kind of interesting: “So how is faster adjustment to be achieved? The answer is through a buoyant eurozone economy and higher wage growth and inflation in core economies than in the enfeebled periphery.”

That’s the challene isn’t it? Did the author have any other suggestions for what would initiate the needed growth”

LikeLike

George, my impression was that he was saying it ain’t gonna happen and Europe will not emulate America and rise above the sum of its parts.

LikeLike